Student Loans Resource & Financial Education

Author: James Smith;

Source: sonicmusic.net

Welcome to our Student Loans resource center — a place dedicated to helping students, graduates, and families better understand the world of education financing. Here we discuss federal and private student loans, repayment strategies, interest rates, forgiveness programs, and practical ways to manage education debt with greater confidence.

You’ll find clear explanations of how student loans work, step-by-step guidance on applying for loans, comparisons of repayment plans, and helpful tools such as loan calculators and financial planning tips. We also explore topics like loan forgiveness programs, deferment and forbearance options, refinancing, and ways to reduce long-term borrowing costs.

Read more

Top Stories

Read more

Read more

Read more

Read more

Trending

Read more

Read more

Latest articles

Most read

Read more

Read more

In depth

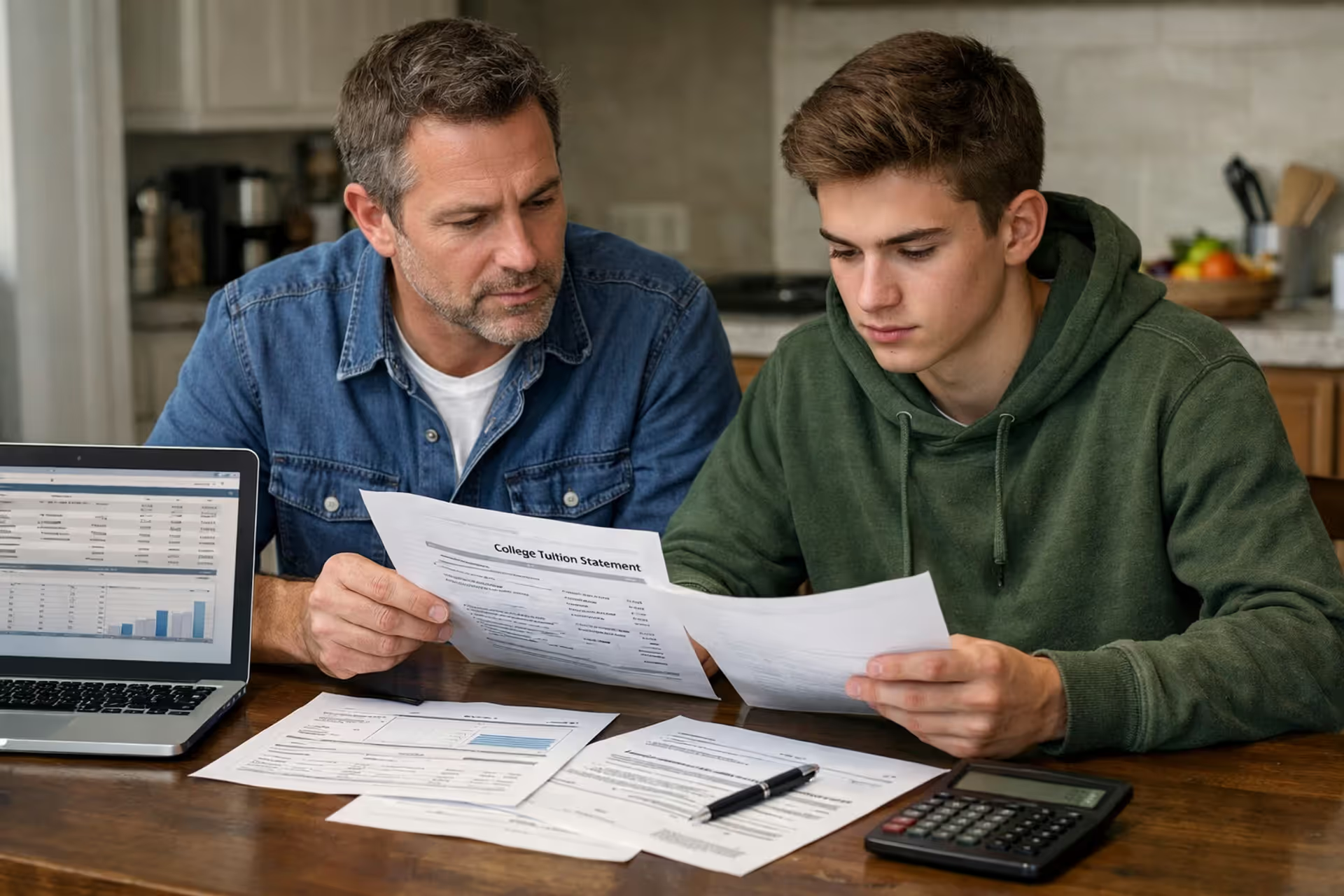

College costs climb higher each year, and federal aid packages rarely cover everything. Your child maxes out their federal student loan eligibility at $5,500 to $7,500 annually depending on their year in school. Scholarships help, but most families still face a substantial gap between what they've saved and what the bursar's office demands each semester.

That's where parent student loans enter the picture. You're taking on debt in your name—not your kid's—to fund their undergraduate degree. It's a generous choice that carries serious long-term consequences for your financial security.

Before you click "submit" on any loan application, you need a clear picture of how these loans function, what they'll actually cost you, and whether borrowing makes sense given your retirement timeline and current debt load.

What Are Parent Student Loans?

Here's the essential distinction: when parents borrow for college, the debt sits entirely on the parent's credit report and remains the parent's legal obligation. Your daughter might promise to pay you back after she lands that engineering job, but the loan servicer doesn't care about pinky swears. They're coming after you if payments stop.

The federal government offers Direct PLUS Loans specifically designed for parents of undergrads. You'll also see these called Parent PLUS Loans—same thing, different name. Banks and online lenders have jumped into this market too, creating private loan products that let parents borrow based on their creditworthin...

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.