Student using loan calculator on computer with financial documents and charts visible on screen

How to Use a Student Loan Calculator?

Planning for college expenses or managing existing debt requires clear numbers. A student loan calculator transforms abstract borrowing decisions into concrete monthly payments, total interest costs, and repayment timelines. Whether you're a high school senior estimating college costs or a graduate navigating repayment options, these tools help you avoid financial surprises.

Understanding how to use these calculators effectively can mean the difference between manageable monthly payments and years of financial strain. This guide walks through every calculator type, input field, and decision point so you can make informed borrowing and repayment choices.

What Is a Student Loan Calculator and Why Use One

A student loan calculator is a digital tool that projects the financial outcomes of borrowing or repaying educational debt. You input basic loan details—principal amount, interest rate, and term length—and the calculator outputs monthly payments, total interest paid, and sometimes alternative repayment scenarios.

The primary benefit is visibility. Most borrowers sign promissory notes without grasping what $50,000 in loans actually costs over ten years. A calculator shows that a 6.5% interest rate on that amount means $567 monthly payments and $18,040 in interest. That clarity helps students borrow only what they need and graduates choose repayment strategies that fit their budgets.

These tools also enable comparison shopping. When you're choosing between a federal Direct Unsubsidized Loan at 5.5% and a private loan at 7.2%, running both through a student loan calculator explained the real cost difference—often thousands of dollars over the life of the loan. Parents evaluating PLUS loans versus home equity lines can see which option creates less long-term financial burden.

Students who estimate their total debt and monthly payments before freshman year are 40% more likely to graduate with manageable debt-to-income ratios. The five minutes spent with a calculator can prevent decades of financial stress

— Jennifer Harmon

Types of Student Loan Calculators

Not all student loans calculators serve the same purpose. Your goal—whether estimating borrowing needs, planning repayment, or exploring refinancing—determines which calculator type provides useful information.

Payment Calculators

Payment calculators answer one core question: "What will I owe each month?" You enter your total loan balance, interest rate, and repayment term (typically 10, 15, 20, or 25 years). The calculator applies standard amortization formulas to show monthly payment amounts under various repayment plans.

These work best when you already have loans and need to budget for repayment. A recent graduate with $35,000 in federal loans at 5.8% interest can see that standard 10-year repayment requires $388 monthly, while extended 25-year repayment drops payments to $218 but increases total interest from $11,560 to $30,400.

Payment calculators often include options for income-driven repayment plans, which cap payments at 10-20% of discretionary income. These require additional inputs like family size and annual income but show how payments adjust as your salary changes.

Author: Evan Thornton;

Source: sonicmusic.net

Borrowing and Cost Calculators

A student loan borrowing calculator helps prospective students estimate how much to borrow for college. You input expected costs—tuition, room, board, books—minus grants, scholarships, and family contributions. The calculator shows the borrowing gap and projects what those loans will cost after graduation.

These tools prevent over-borrowing. A student planning to borrow $80,000 for a degree that typically leads to $45,000 starting salaries can see that monthly payments would consume 25% of gross income—well above the recommended 10-15% threshold.

Cost calculators go further by incorporating opportunity costs and total repayment amounts. Borrowing $30,000 at 6% over ten years costs $39,960 total—that extra $9,960 represents money unavailable for retirement savings, home down payments, or other financial goals during your twenties and thirties.

Refinance and Consolidation Calculators

These specialized tools help borrowers with existing loans evaluate whether refinancing or consolidating makes financial sense. You input current loan balances, interest rates, and remaining terms, then compare them against new loan offers.

A refinance calculator might show that consolidating three private loans (totaling $45,000 at rates of 7.5%, 8.2%, and 6.9%) into a single loan at 5.8% saves $127 monthly and $15,240 over the life of the loans. However, it also reveals trade-offs: refinancing federal loans into private loans eliminates income-driven repayment options and forgiveness programs.

Consolidation calculators for federal loans show different outcomes. Federal Direct Consolidation doesn't lower your interest rate—it creates a weighted average of existing rates, rounded up to the nearest one-eighth percent. The benefit is simplified payments and access to certain repayment plans, not interest savings.

How to Calculate Student Loan Payments Step-by-Step

Walking through the calculation process with a student loan calculator guide reveals exactly how inputs affect outputs. Here's the standard workflow:

Step 1: Enter the principal amount. This is your total borrowed amount across all loans you're calculating. If you have multiple loans with different rates, calculate them separately or use a multi-loan calculator. For example, enter $28,000 if that's your expected total borrowing for a four-year degree.

Step 2: Input the interest rate. Federal loan rates for 2026 are fixed at origination and vary by loan type. Direct Subsidized and Unsubsidized Loans for undergraduates currently sit around 5.5%, while PLUS loans approach 8.05%. Private loans range from 3.5% to 14% depending on creditworthiness. Enter the exact rate from your loan documents or offers.

Step 3: Select the repayment term. Standard federal repayment is 10 years (120 months). Extended plans stretch to 25 years. Private loans often offer 5, 7, 10, or 15-year terms. Shorter terms mean higher monthly payments but less total interest.

Step 4: Choose your repayment plan type. Standard repayment means fixed payments throughout the term. Graduated repayment starts lower and increases every two years. Income-driven plans (IBR, PAYE, REPAYE) require income and family size data.

Step 5: Review the output. The calculator displays monthly payment amounts, total interest paid, and total repayment cost. Advanced calculators show amortization schedules—month-by-month breakdowns of how much goes toward principal versus interest.

For that $28,000 loan at 5.5% over 10 years, you'd see a $305 monthly payment, $8,600 in total interest, and a $36,600 total repayment amount. If you switched to 20-year repayment, monthly payments drop to $193, but total interest jumps to $18,320—more than double.

Author: Evan Thornton;

Source: sonicmusic.net

Key Factors That Affect Your Student Loan Estimate

Several variables dramatically change what a student loan estimate calculator shows. Understanding these factors helps you manipulate inputs to see best-case and worst-case scenarios.

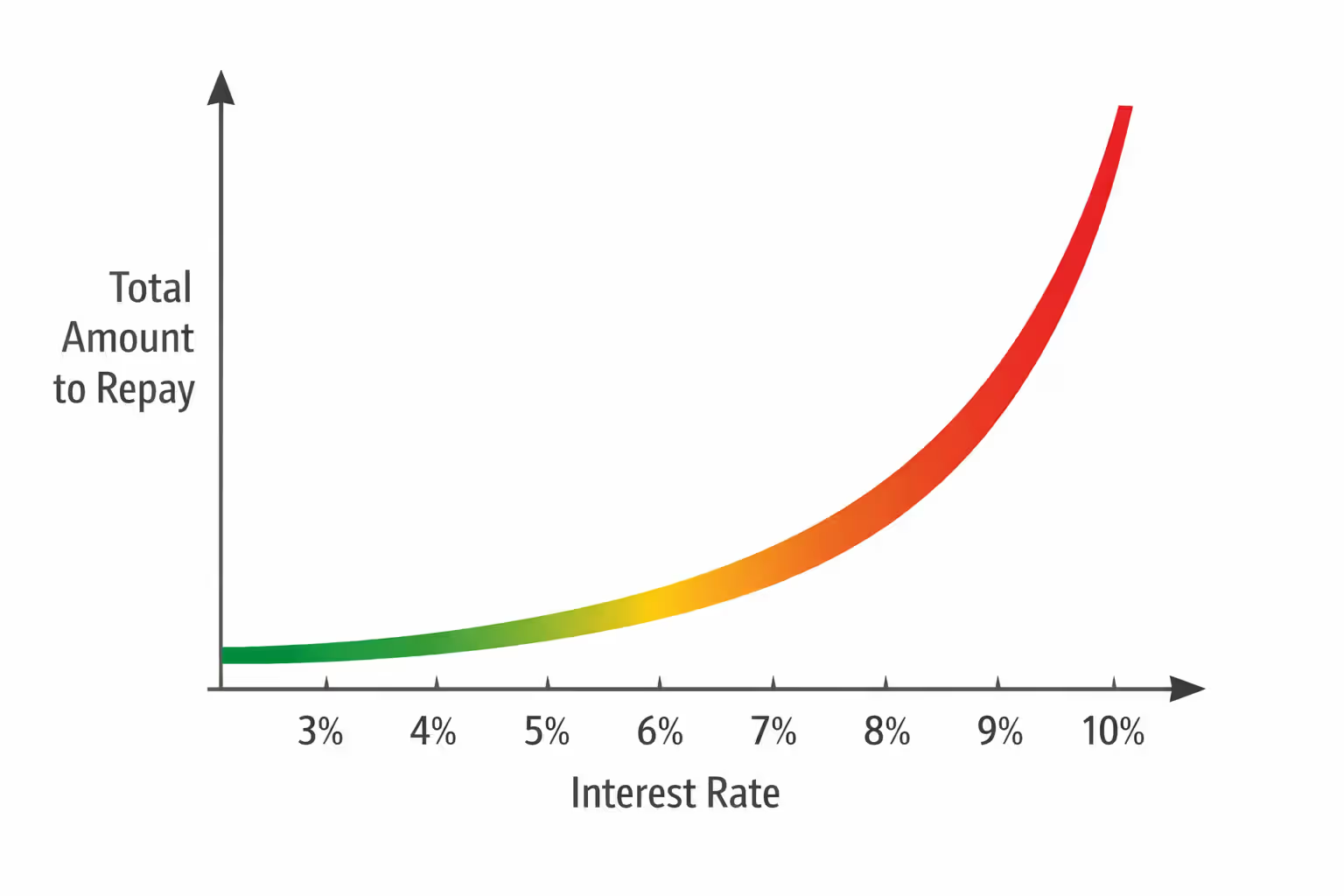

Interest rates have the most significant impact. A single percentage point changes outcomes substantially. On a $40,000 loan over 10 years, the difference between 5% and 6% interest is $30 monthly and $3,600 over the life of the loan. Federal rates reset annually each July based on Treasury yields, so borrowing year matters. Private rates depend on credit scores—excellent credit might qualify for 4.5% while fair credit faces 10% or higher.

Loan term length creates a trade-off between affordability and total cost. Doubling your repayment term from 10 to 20 years roughly cuts monthly payments in half but often doubles total interest paid. Borrowers fixated on low monthly payments sometimes choose extended terms without realizing they'll pay $20,000 extra over the loan's life.

Repayment plan type matters primarily for federal loans. Standard repayment costs the least over time. Income-driven plans offer lower initial payments but extend repayment to 20-25 years, dramatically increasing total interest. However, remaining balances are forgiven after that period (though forgiven amounts may be taxable income).

Federal versus private loans operate under different rules. Federal loans offer fixed rates, income-driven repayment, deferment during economic hardship, and potential forgiveness. Private loans typically offer no such protections but sometimes feature lower rates for well-qualified borrowers. A calculate student loan payments tool should specify which loan type you're modeling.

Interest capitalization occurs when unpaid interest gets added to your principal balance. This happens after deferment, forbearance, or at the end of grace periods. If you defer $30,000 in loans for three years at 6% interest, roughly $5,400 in interest capitalizes, creating a new principal balance of $35,400. Future interest accrues on that higher amount, compounding your costs. Many basic calculators don't account for this, leading to underestimated payments.

Fees add to borrowing costs but rarely appear in simple calculators. Federal Direct Loans charge 1.057% origination fees (deducted from disbursement), while private loans may charge 0-5%. A $10,000 loan with a 1% fee means you receive $9,900 but owe $10,000 plus interest.

Author: Evan Thornton;

Source: sonicmusic.net

Common Mistakes When Using a Student Loan Calculator

Even with a comprehensive student loan calculator guide, users make predictable errors that lead to inaccurate estimates.

Ignoring loan fees is the most common oversight. You might calculate payments on a $20,000 loan, but after a 1% origination fee, you actually receive $19,800 while owing interest on $20,000. The difference seems small but compounds over 10 years.

Using the wrong interest rate happens when borrowers confuse federal and private rates or input outdated information. Federal rates change annually, so using last year's 4.99% when this year's rate is 5.5% underestimates payments by roughly $15 monthly on a $30,000 loan.

Not accounting for multiple loans with different rates leads to oversimplification. If you have $15,000 at 4.5% and $15,000 at 7%, calculating $30,000 at 5.75% (the average) produces slightly different results than calculating each loan separately. The weighted average approach works for rough estimates but not precise budgeting.

Misunderstanding income-driven repayment is widespread. These plans calculate payments as a percentage of discretionary income (income above 150-225% of poverty guidelines), not gross income. A borrower earning $50,000 might expect 10% ($5,000 annually, or $417 monthly) under an income-driven plan, but after the poverty guideline adjustment, actual payments might be $275. Using the wrong formula skews planning.

Assuming static income when using payment calculators creates unrealistic long-term projections. Your $40,000 starting salary will likely grow to $60,000+ within five years. Calculators showing unaffordable payments based on entry-level income might look manageable once you account for typical career progression in your field.

Forgetting about tax implications of certain strategies can backfire. Parent PLUS loans offer interest tax deductions up to $2,500 if income limits are met, effectively reducing the interest rate. Similarly, forgiven loan balances under income-driven plans may be taxable as income—$50,000 forgiven after 20 years could create a $10,000+ tax bill.

Overlooking prepayment benefits means missing opportunities to reduce costs. Most calculators show standard repayment schedules, but paying an extra $100 monthly on a $30,000 loan at 6% shortens the term from 10 years to 7.5 years and saves $2,800 in interest. Few borrowers run these scenarios without specifically looking for a prepayment calculator.

Author: Evan Thornton;

Source: sonicmusic.net

How to Choose the Right Student Loan Calculator for Your Needs

Matching calculator type to your specific situation ensures you get actionable information rather than generic estimates.

If you're planning for college costs, use a student loan borrowing calculator that incorporates total cost of attendance, expected family contribution, and likely aid packages. These tools help you understand the borrowing gap before you commit to a school. Compare the four-year borrowing total across multiple schools—a prestigious private university might require $80,000 in loans while a state school needs $30,000. The calculator shows that the $50,000 difference translates to $550 more in monthly payments for a decade.

If you're about to enter repayment, a payment calculator with multiple repayment plan options is essential. Input your exact loan balances and rates, then model standard, graduated, extended, and income-driven plans. See which fits your starting salary and how payments change as income grows. This is the time to decide whether to prioritize low monthly payments or minimal total interest.

If you're considering refinancing, use a refinance calculator that shows side-by-side comparisons. Input your current loans and the refinance offer, then examine monthly payment differences, total interest savings, and term length changes. Pay attention to what you lose—federal loan protections, income-driven options, potential forgiveness—and whether the interest savings justify those trade-offs.

If you're evaluating loan offers, a student loan cost calculator that shows total repayment amounts across different scenarios helps. A private loan at 5.5% might look better than a federal loan at 6.5%, but when you factor in federal protections and the option to switch to income-driven repayment if you face financial hardship, the higher-rate federal loan might be the safer choice.

If you're managing multiple loans, seek calculators that handle multiple inputs with different rates and terms. These show your total monthly obligation across all loans and help you decide whether consolidation simplifies payments enough to justify any interest rate changes.

If you're self-employed or have variable income, use calculators that model income-driven plans with fluctuating income inputs. Your payments under PAYE or IBR will change as your income changes, so seeing how payments adjust between $40,000 and $70,000 income years helps you budget for variability.

Comparison of Student Loan Calculator Types

| Calculator Type | Best For | Key Inputs | What It Shows |

| Payment Calculator | Graduates entering repayment | Loan balance, interest rate, term, repayment plan | Monthly payment amount, total interest, payoff date |

| Borrowing Calculator | Prospective students estimating needs | College costs, financial aid, family contribution | Required borrowing amount, projected monthly payments |

| Cost Calculator | Comparing total loan costs | Principal, rate, term, fees | Total repayment amount, lifetime interest cost |

| Refinance Calculator | Borrowers with existing loans considering refinancing | Current loans, new loan offers, credit score | Interest savings, new monthly payment, trade-offs |

| Consolidation Calculator | Multiple loan holders | Individual loan balances and rates | Combined payment, weighted average rate |

| Income-Driven Calculator | Borrowers needing lower payments | Income, family size, loan balance, discretionary income threshold | Monthly payment under various IDR plans, forgiveness timeline |

Frequently Asked Questions About Student Loan Calculators

Student loan calculators transform abstract debt into concrete numbers you can evaluate and plan around. The difference between borrowing blindly and borrowing strategically often comes down to spending 15 minutes with the right calculator before making decisions.

Use these tools at every stage of your education financing journey. Before applying to colleges, estimate total borrowing needs and post-graduation payments to ensure your degree investment makes financial sense. When comparing loan offers, calculate the real cost difference between options—sometimes a slightly higher interest rate on a federal loan is worth it for the repayment flexibility. As you enter repayment, model different plans to find the balance between affordable monthly payments and reasonable total costs.

Remember that calculators provide estimates based on the data you input. Garbage in, garbage out. Take time to gather accurate numbers: your exact loan amounts, current interest rates, and realistic income projections. Run multiple scenarios—best case, worst case, and most likely—to understand your range of possible outcomes.

The most valuable insight from any student loan calculator isn't a single number. It's the understanding of how different variables interact to create your financial future. Small changes in borrowing amounts, interest rates, or repayment terms create large differences in what you'll ultimately pay. That knowledge empowers you to make borrowing decisions you won't regret a decade later.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.