Young graduate in cap and gown standing at a crossroads holding a diploma and a loan envelope, choosing between multiple repayment path

How to Choose Student Loan Repayment Plans?

You've borrowed money for college. The diploma's in hand, and now reality hits: figuring out how to actually repay those loans. Make the wrong choice here, and you could waste $15,000 or more in extra interest charges. Choose strategically? You'll maintain a manageable budget and potentially unlock debt cancellation opportunities.

The numbers tell the story—roughly 43 million people across the United States are currently managing federal student loans. Here's what most don't realize at first: you're choosing from eight distinct repayment structures. Some keep your monthly bill constant throughout a fixed timeline. Others adjust what you pay based on your earnings and family size. Borrowed from banks instead of the federal government? You're working with an entirely separate framework.

This resource breaks down every available repayment path in 2026, reveals actual payment amounts you can expect, and guides you toward the approach that aligns with your financial reality.

What Are Student Loan Repayment Plans?

Your repayment plan determines three critical elements: your monthly bill amount, the timeline until you're debt-free, and whether you might qualify for balance forgiveness later. The Department of Education establishes these frameworks for federal borrowing. Private lenders? They create their own terms.

Federal options divide into two categories. The first group operates on predetermined schedules—your payment stems from your total debt and follows a set calendar. You'll see consistent expectations about what you owe and when you'll finish paying. The second category ties payments to your current earnings and family composition, then reassesses annually.

Your selection ripples beyond just what you pay each month. It shapes your total interest accumulation, influences your financial stress levels, and controls access to forgiveness initiatives. Consider the traditional decade-long plan—you'll minimize interest charges but face stiffer monthly obligations. Opt for an extended income-based track instead, and early payments might barely register, though interest can snowball if your career takes off. This becomes especially crucial for anyone pursuing Public Service Loan Forgiveness, which requires enrollment in particular income-driven structures for 120 consecutive payments.

Federal Student Loan Repayment Options

After graduation, your loans automatically enter the Standard Repayment Plan until you actively select an alternative. These three structured approaches work effectively for borrowers with reliable income who value knowing their exact debt-free date.

Standard Repayment Plan

The foundation approach divides your balance into 120 identical payments spanning a decade. Here's a concrete scenario: carrying $30,000 at 5.5% interest means approximately $326 monthly, with roughly $9,100 in interest charges by completion. Every alternative gets benchmarked against this baseline.

Eligibility extends broadly—anyone holding federal Direct Loans qualifies, along with those managing older FFEL Program loans or Perkins Loans. Parents carrying PLUS loans can use this track too. The advantage is clarity—debt disappears quickly while interest stays contained. The challenge? That monthly obligation can strain fresh graduates earning entry-level wages.

Author: Marcus Bennett;

Source: sonicmusic.net

Graduated Repayment Plan

This structure eases you in gently, then escalates over time. Initial payments might start around $183 for a $30,000 loan, climbing every 24 months until you're paying roughly $530 toward the end. The framework anticipates career progression, betting your income will rise to accommodate larger bills.

Federal loan types across the board work here, Parent PLUS included. There's a price: interest charges increase by several thousand compared to standard repayment because those modest early payments barely touch accumulating interest. This strategy succeeds when you're, say, completing a residency before earning attending physician compensation. It falters when salary growth stalls or life throws financial curveballs.

Extended Repayment Plan

Spread your obligations across a quarter-century—that's the extended framework. Qualification requires carrying federal debt of $30,000 or higher across Direct or FFEL loans. Monthly bills shrink considerably (that same $30,000 balance might demand just $175 monthly on the fixed option), but lifetime interest balloons to approximately $22,500.

This path helps when debt volume overwhelms your budget and you legitimately need monthly breathing room. The downside? You're committing to 15 additional years of interest charges versus standard repayment. Another consideration—extended plans don't count toward Public Service Loan Forgiveness, which matters for government and nonprofit employees.

Income-Driven Repayment Plans Explained

Income-driven frameworks recalculate your obligation annually by examining your tax documents, household composition, and federal poverty thresholds. After two to two-and-a-half decades of consistent payments (timeline varies by plan), any remaining balance gets eliminated—though tax implications on forgiven amounts depend on your specific plan and current regulations. These structures target individuals whose debt dwarfs their yearly earnings or who've chosen service-oriented careers with modest compensation.

Author: Marcus Bennett;

Source: sonicmusic.net

Income-Based Repayment (IBR)

IBR restricts your payment to either 10% or 15% of "discretionary income," determined by when you first borrowed. Your initial loan disbursement occurred July 1, 2014 or later? You'll face the 10% threshold. Earlier borrowers see 15%. Discretionary income calculates as your adjusted gross income with 150% of poverty guidelines for your household subtracted out.

Here's a practical walkthrough: you're single, pulling in $45,000 annually, and meet criteria for the 10% tier. Monthly payments land near $264. Continue paying for 20 years (or 25 if you borrowed earlier), and your servicer wipes remaining balances. Direct Loan and FFEL borrowers can access IBR. Parent PLUS doesn't qualify.

A helpful feature during your initial 36 months—when your calculated payment falls short of accruing interest, the government covers unpaid interest on subsidized loans. Beyond year three, that unpaid interest adds to your principal. Annual income verification is mandatory. Skip that deadline? Your payment jumps to whatever the decade-long standard schedule would demand, which can devastate your budget.

Pay As You Earn (PAYE)

PAYE similarly caps obligations at 10% of discretionary income using identical 150% poverty calculations. The distinction? Stricter eligibility: your first federal loan must date to October 1, 2007 or later, and you needed another disbursement October 1, 2011 or after. Parent PLUS loans remain excluded.

Forgiveness arrives after 20 years. Built-in protection exists—your payment can't surpass what standard 10-year repayment would cost, even with significant income growth. This ceiling shields high earners but might extend repayment if you pivot careers midstream.

The interest subsidy parallels IBR: government coverage of unpaid interest on subsidized loans for 36 months before capitalization begins. PAYE suits borrowers carrying moderate debt who anticipate income increases but need safety nets during early lean years.

Saving on a Valuable Education (SAVE)

SAVE supplanted REPAYE in 2023 and delivers the most favorable terms available among income-driven options in 2026. Payments cap at 5% of discretionary income for undergraduate debt and 10% for graduate obligations (or a proportional blend with both). The discretionary income formula applies 225% of poverty thresholds, shielding more of your earnings.

Return to that single $45,000 earner—under SAVE, undergraduate debt monthly payments might only hit $132. That's half of IBR's requirement. Forgiveness triggers at 20 years for undergraduate borrowers and 25 for graduate degree holders. Original borrowing under $12,000? You could see forgiveness after merely 10 years of payments.

SAVE's interest subsidy is powerful: when monthly payments don't cover accumulating interest, the government cancels 100% of that unpaid interest rather than letting it compound into your balance. This prevents ballooning debt and makes SAVE attractive when your debt-to-income numbers look troubling. All Direct Loan holders qualify, and Parent PLUS borrowers gain access after consolidating into a Direct Consolidation Loan.

Income-Contingent Repayment (ICR)

ICR represents the earliest income-driven framework and typically delivers less favorable terms for most borrowers. Your payment becomes whichever amount is smaller: 20% of discretionary income or what you'd owe on a fixed 12-year schedule adjusted for income. Discretionary income here applies 100% of poverty thresholds, protecting less of your paycheck than SAVE or PAYE.

Forgiveness materializes after 25 years. ICR's primary relevance today? It stands as the sole income-driven avenue for Parent PLUS borrowers who consolidate into Direct Consolidation Loans. Monthly obligations typically exceed other IDR plans, and no interest subsidy exists. Most borrowers bypass ICR unless they're parents seeking income-based relief or consolidating legacy FFEL loans.

Private Student Loan Payment Plans

Private lenders function outside federal systems and establish their own conditions. Most private loans follow predetermined repayment calendars—commonly 5, 7, 10, or 15 years—with monthly payments engineered to eliminate your balance by the endpoint. Interest rates correlate with your credit profile and market forces, and variable-rate products can adjust quarterly or annually.

Unlike federal alternatives, private lenders rarely provide income-driven repayment or debt cancellation. Some might authorize temporary forbearance or permit interest-only payments during hardship, but that's discretionary and often limited to 12 months cumulatively. Borrowers wrestling with private loan obligations typically explore refinancing—essentially replacing your original loan with a new product featuring different rates or timelines.

Refinancing can reduce monthly bills by lengthening the term or securing lower rates, but tradeoffs exist. Refinance federal loans into private products? You surrender income-driven plans, forgiveness programs, and federal safeguards like deferment during economic turbulence. Only refinance when you're confident about income consistency and you're uninterested in Public Service Loan Forgiveness or other federal advantages.

Private lenders frequently include co-signer release after 24 to 48 consecutive on-time payments, which improves your debt-to-income ratio for future credit needs. Many reduce your interest rate by 0.25 to 0.50 percentage points for autopay enrollment—a simple method to trim total interest.

Author: Marcus Bennett;

Source: sonicmusic.net

Comparing Student Loan Repayment Plans

This breakdown presents core characteristics of federal repayment alternatives so you can evaluate monthly affordability against lifetime expenses and forgiveness qualification.

| Repayment Structure | Monthly Payment Calculation | Duration | Debt Cancellation | Ideal Borrower Profile |

| Standard | Fixed identical amount throughout | 10 years | None | Borrowers with consistent income seeking minimal interest costs |

| Graduated | Begins modest, rises biennially | 10 years | None | Early-career individuals anticipating salary increases |

| Extended | Reduced fixed or graduated amounts | 25 years | None | Large-balance borrowers requiring monthly budget flexibility |

| IBR | 10% or 15% of discretionary income annually | 20 or 25 years | Available after full term | Borrowers whose debt surpasses yearly earnings |

| PAYE | 10% of discretionary income, capped at standard amount | 20 years | Available after 20 years | Borrowers with initial loans after October 2007 |

| SAVE | 5% (undergraduate) or 10% (graduate) of discretionary income | 10–25 years | Available after 10–25 years | Borrowers with challenging debt-to-income ratios or smaller balances |

| ICR | Lower of 20% discretionary income or modified 12-year fixed | 25 years | Available after 25 years | Parent PLUS borrowers post-consolidation |

Concentrate on three elements during comparison: immediate cash availability, cumulative interest paid, and forgiveness qualification. Someone carrying $50,000 in loans while earning $40,000 faces $555 monthly under standard but merely $207 under SAVE. Across 10 years, standard generates roughly $16,600 in interest charges. SAVE could produce higher cumulative interest if income surges dramatically, but monthly flexibility might enable emergency savings or retirement contributions.

Forgiveness presents complications. Yes, it can eliminate tens of thousands in debt, but you're pledging decades of payments and annual documentation. If you anticipate rapid income acceleration or plan workforce exits, you might actually pay more under income-driven frameworks than aggressively tackling standard repayment.

How to Select the Right Repayment Plan

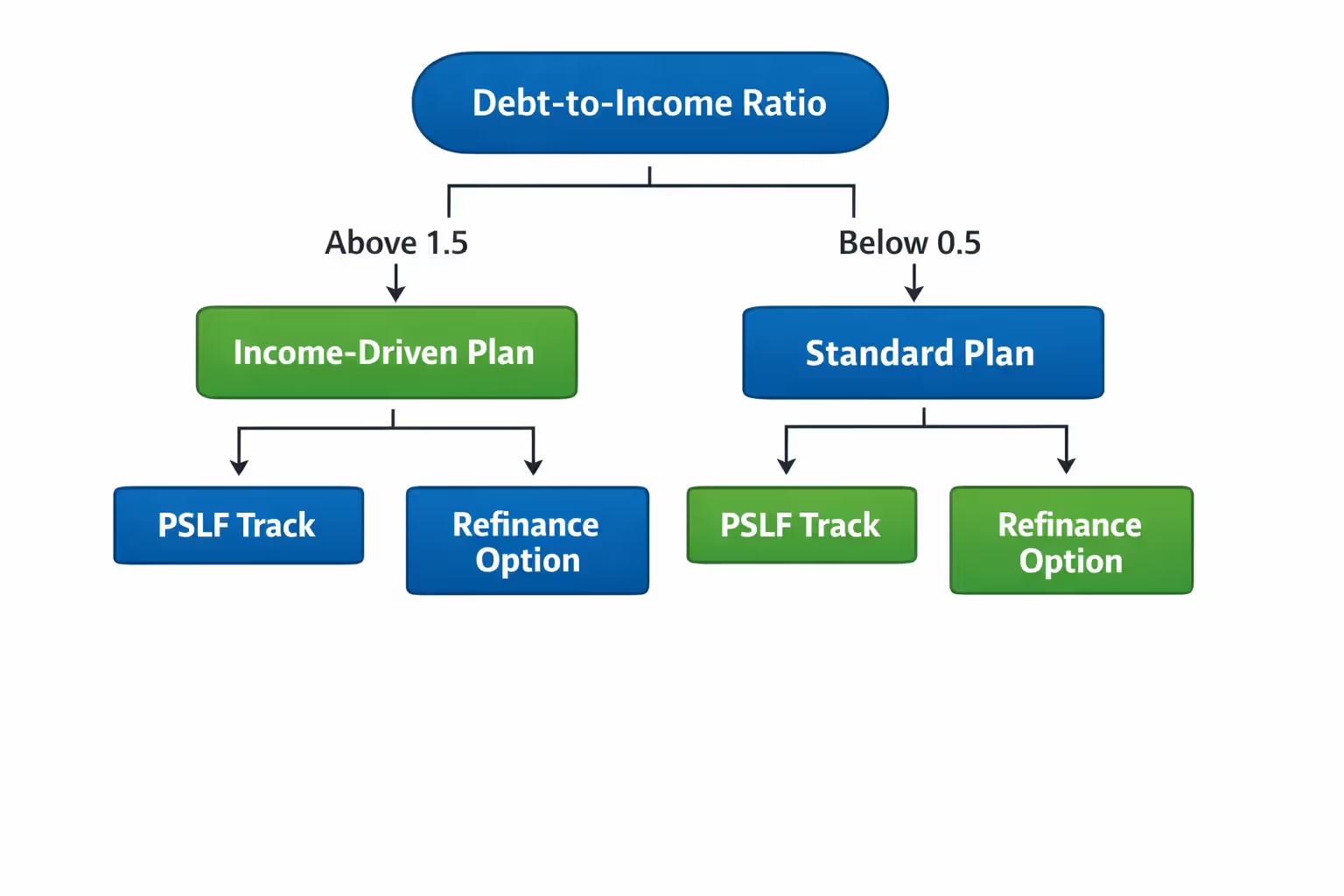

Begin by calculating your debt-to-income ratio: divide total federal student loan balance by current annual gross income. Above 1.5? An income-driven framework probably makes financial sense. Below 0.5? Standard repayment saves maximum money unless you're pursuing Public Service Loan Forgiveness.

Next, project where your earnings trend. Medical residents, new attorneys, and junior software engineers often benefit from graduated or income-driven structures during constrained years, then refinance or transition to aggressive repayment once compensation jumps. Teachers, social workers, and nonprofit employees should prioritize income-driven frameworks qualifying for PSLF, even when monthly payments exceed minimums, because forgiveness after 10 years of public service can dwarf any interest savings from abbreviated plans.

Author: Marcus Bennett;

Source: sonicmusic.net

Account for household evolution. Married and filing jointly? Your spouse's income inflates discretionary income calculations under most IDR plans. Filing separately might reduce your payment but increase tax burden. Model both scenarios before committing. Planning for children? Household size reduces discretionary income, shrinking monthly obligations under income-driven frameworks.

Common pitfalls to avoid: don't miss recertification deadlines (triggers payment surges); don't treat forbearance as cost-free (interest compounds onto balance); and don't refinance federal debt if you might need income-driven plans or forgiveness later. Many borrowers also underestimate tax consequences of canceled balances. Current regulations may treat forgiveness from income-driven plans (excluding PSLF) as taxable income, creating lump-sum tax obligations the year debt gets eliminated. SAVE's 10-year forgiveness for modest balances represents a notable exception.

Leverage the Federal Student Aid Loan Simulator at studentaid.gov/loan-simulator to test scenarios. Input your balance, interest rate, income, and household size, then compare monthly payments and lifetime expenses across all frameworks. The tool also projects PSLF eligibility and forgiveness quantities.

Selecting a repayment framework isn't a permanent choice that locks you in forever.Your earnings shift. Your family circumstances change. Your professional ambitions evolve. Reassess your approach annually, particularly after significant life transitions like marriage, career changes, or raises. What functions effectively at 25 might prove terrible at 35, and federal plan adaptability lets you adjust without penalties

— Michael Lux

Frequently Asked Questions About Student Loan Repayment

Identifying the optimal repayment framework means balancing current affordability against lifetime expenses while synchronizing your choice with career objectives and life circumstances. Federal borrowers possess remarkable flexibility—eight distinct alternatives, unlimited switching capability, and forgiveness programs that can erase six-figure debt for public servants or borrowers completing decades of payments. Private borrowers face narrower choices but can leverage refinancing to capture reduced rates or abbreviated terms when income and credit improve.

Calculate thoroughly, revisit decisions annually, and adjust freely as your financial landscape transforms. The framework fitting your current circumstances may prove inadequate six months forward, and federal protections ensure you're never trapped in a structure that no longer serves your needs. Whether you're a recent graduate initiating first payments or a mid-career professional reconsidering strategy, the proper repayment framework can liberate cash for competing priorities, shield you during constrained periods, and establish sustainable paths toward complete debt elimination.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.