Parent and college student reviewing tuition bills and loan documents at home

Parent Student Loans Guide

College costs climb higher each year, and federal aid packages rarely cover everything. Your child maxes out their federal student loan eligibility at $5,500 to $7,500 annually depending on their year in school. Scholarships help, but most families still face a substantial gap between what they've saved and what the bursar's office demands each semester.

That's where parent student loans enter the picture. You're taking on debt in your name—not your kid's—to fund their undergraduate degree. It's a generous choice that carries serious long-term consequences for your financial security.

Before you click "submit" on any loan application, you need a clear picture of how these loans function, what they'll actually cost you, and whether borrowing makes sense given your retirement timeline and current debt load.

What Are Parent Student Loans?

Here's the essential distinction: when parents borrow for college, the debt sits entirely on the parent's credit report and remains the parent's legal obligation. Your daughter might promise to pay you back after she lands that engineering job, but the loan servicer doesn't care about pinky swears. They're coming after you if payments stop.

The federal government offers Direct PLUS Loans specifically designed for parents of undergrads. You'll also see these called Parent PLUS Loans—same thing, different name. Banks and online lenders have jumped into this market too, creating private loan products that let parents borrow based on their creditworthiness.

Who can actually apply? Biological and adoptive parents qualify automatically. Stepparents can borrow if they're currently married to the student's biological or adoptive parent and if their financial information appeared on the FAFSA form. Grandparents raising their grandchildren? Generally out of luck for federal PLUS loans, though some private lenders might work with you.

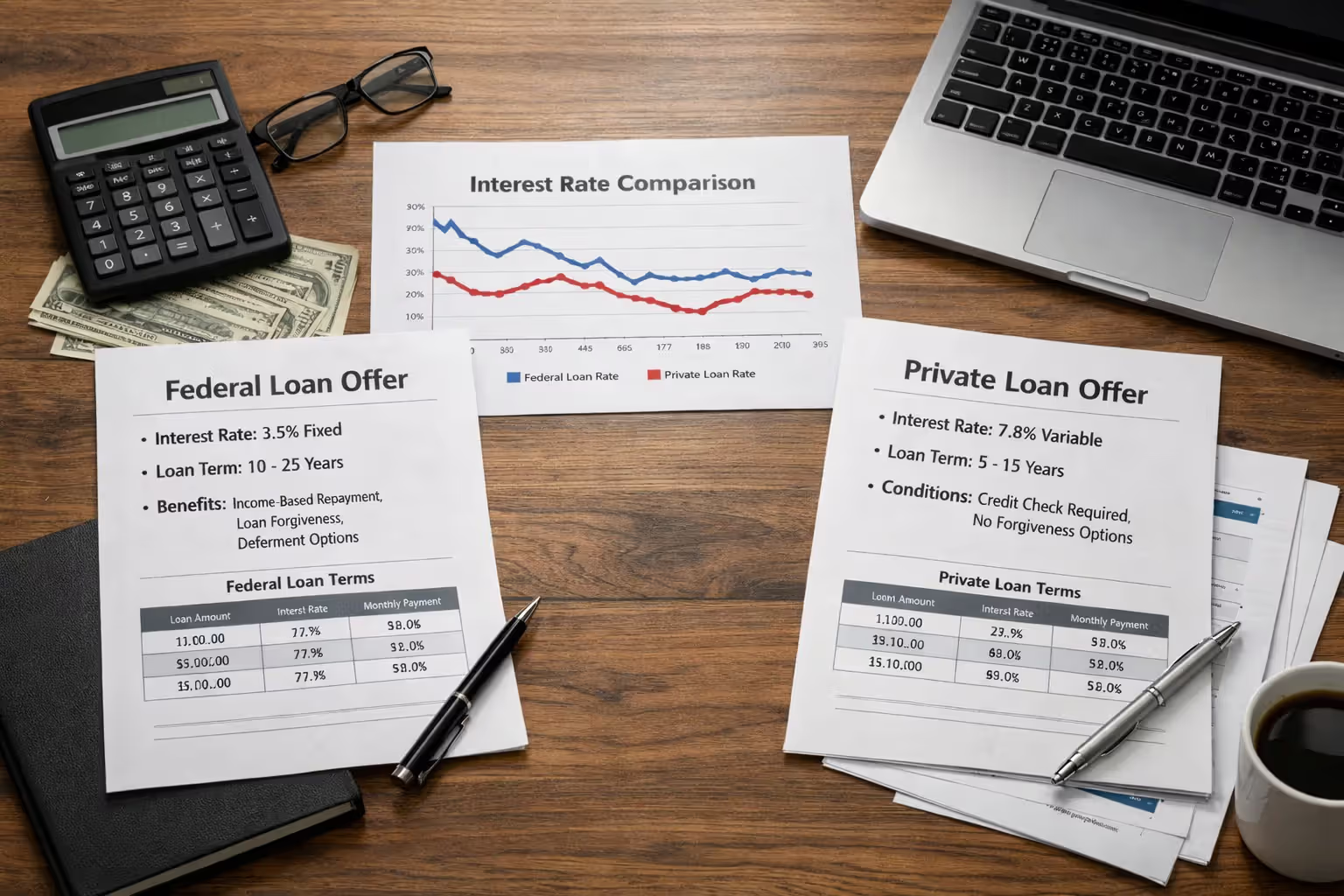

Federal versus private represents the fundamental choice you'll make. Federal loans come with fixed interest rates that don't depend on your credit score, plus certain safety nets if your finances tank. Private loans might offer lower rates if your credit score tops 760, but you're giving up federal protections in exchange for those savings.

How Do Student Loans Work for Parents?

The timeline starts after your student completes the FAFSA and the college sends their aid offer. You look at the numbers: tuition runs $28,000, room and board adds $14,000, the school estimates another $3,000 for books and expenses. Total: $45,000. Your student qualified for a $6,000 Pell Grant, $3,500 in subsidized federal loans, and $2,000 in unsubsidized loans. You've saved $8,000. That leaves a $25,500 gap.

Author: Evan Thornton;

Source: sonicmusic.net

For federal Parent PLUS Loans, you head to studentaid.gov and log in with your FSA ID—the same credential you used for the FAFSA. The application takes maybe 20 minutes. You'll authorize a credit check, but the government doesn't calculate a traditional credit score. Instead, they scan your credit report for recent disasters: bankruptcy filings in the past five years, loan defaults, foreclosures, accounts sitting in collections, tax liens, or charge-offs exceeding $2,085.

Clean history? You're approved within minutes. The government lets you borrow up to the school's published cost of attendance minus any other financial aid your student already accepted. In this example, you could borrow the full $25,500 gap—or more if the school's official budget exceeds their basic tuition and fees.

Private lenders run conventional credit checks. They want to see your FICO score (most want 680 minimum, though some accept 650), verify your employment and income, and calculate your debt-to-income ratio. They're typically looking for DTI below 40%, though some go up to 50% for borrowers with exceptional credit. You'll submit pay stubs, W-2s, and possibly tax returns.

Once approved by either route, the school's financial aid office certifies your loan amount. They're confirming you're not borrowing more than allowed. Money flows directly to the college bursar, who applies it to your student's account. Tuition and fees get paid first. Anything left over gets refunded to your student for living expenses, usually via direct deposit or a check.

Here's what catches families off guard: the loan lives on your credit report exclusively. Your son isn't building credit. Late payments wreck your score and trigger collection calls to your phone. If you default, the government can garnish your wages, intercept your tax refunds, and even offset your Social Security benefits once you retire. Private lenders can sue you. The loan doesn't magically transfer to your child after graduation unless you go through a formal refinancing process where they qualify independently.

Federal Parent PLUS Loans vs. Private Parent Student Loans

These two categories operate under completely different rules.

Federal Direct PLUS Loans

Every parent borrower pays the same rate for federal PLUS loans taken during the same academic year. For 2025-2026, that rate sits at 8.05%, locked in for the life of that specific loan. Borrow again next year? You'll get whatever rate Congress sets for 2026-2027.

The government also clips you for a 4.228% origination fee right off the top. Request $20,000 and you'll actually receive $19,154.40, but your loan balance starts at the full $20,000. That fee gets worse the more you borrow—on $50,000, you're paying $2,114 in fees before interest even enters the picture.

That lenient credit check makes PLUS loans accessible to families who'd never qualify for private financing. Spotty payment history from three years ago? Not a deal-breaker unless it resulted in a default or charge-off. Recent late payments on credit cards? The system doesn't weight those heavily unless accounts went to collections.

Get denied? You can add an endorser—basically a cosigner—who agrees to repay if you don't. Or you can document extenuating circumstances that explain why your credit shows negative marks. Maybe you were unemployed for eight months and fell behind on car payments, but now you're back at work with steady income.

No maximum lifetime borrowing limit exists beyond the annual cost of attendance. Parents of twins at expensive private colleges have borrowed $200,000 or more through PLUS loans. The government will keep lending as long as you keep qualifying and the school certifies the amounts.

Repayment normally kicks in 60 days after the loan fully disburses, though you can request deferment while your student remains enrolled at least half-time. Interest accrues during deferment—it's not paused, just the payment requirement.

Standard repayment stretches over 10 years with fixed monthly payments. Graduated plans start lower and bump up every two years. Extended repayment becomes available once you owe more than $30,000 across all federal loans, letting you stretch payments over 25 years.

Income-driven repayment doesn't directly apply to Parent PLUS Loans, which frustrates many borrowers. The workaround: consolidate your PLUS loans into a Direct Consolidation Loan, which then qualifies for Income-Contingent Repayment. Your monthly payment becomes 20% of discretionary income or what you'd pay under a 12-year fixed plan, whichever is less. After 25 years of payments, remaining debt gets forgiven—but you'll owe income tax on the forgiven amount.

If you die or become totally and permanently disabled, the loan discharges without your estate or heirs owing anything. That sounds grim, but it's a meaningful protection that private loans don't always match.

Private Parent Student Loans

Walk into this market with strong credit and you might find rates starting around 5.50% variable or 6.25% fixed as of early 2026. Show up with a 680 credit score and you're looking at 9% or higher. Below 650? Many lenders simply won't approve you at any rate.

Author: Evan Thornton;

Source: sonicmusic.net

Most private lenders skip origination fees entirely. Borrow $20,000 and you receive the full $20,000. That immediately gives private loans an advantage for well-qualified borrowers, even before comparing interest rates.

You'll face stricter underwriting. Lenders verify your employment—they might call your HR department. They calculate your debt-to-income ratio by adding up your mortgage, car payment, credit card minimums, and the new student loan payment, then dividing by your gross monthly income. Over 43% DTI? You'll likely get denied unless you have substantial assets.

Loan limits vary by lender. Most cap you at the cost of attendance minus other aid, similar to federal loans. Some impose aggregate limits—$150,000 total across all years, for instance. A handful of lenders serving families at expensive schools go up to $250,000 total.

Repayment terms range from five to 20 years. Shorter terms mean higher monthly payments but dramatically less total interest. A $30,000 loan at 7% over five years costs $594 monthly and $5,640 in total interest. Stretch it to 15 years and payments drop to $270, but interest balloons to $18,600.

Some lenders let you defer payments while your student attends school. Others require interest-only payments immediately. A few demand full principal-and-interest payments from day one. Read the terms carefully.

Federal protections like income-driven repayment and Public Service Loan Forgiveness don't exist in the private loan world. Some lenders offer forbearance if you lose your job, but it's discretionary—not guaranteed. Death and disability discharge policies vary wildly. Some lenders match federal generosity. Others provide no discharge at all, leaving your estate or cosigner on the hook.

| Feature | Federal PLUS Loan | Private Loan |

| Rate (2025-2026) | 8.05% fixed regardless of credit | 5.50%–12%+ depending on credit profile; variable or fixed available |

| Credit evaluation | Checks only for serious negative events in past five years | Full credit review requiring minimum score, usually 650–680 |

| Maximum you can borrow | School's certified cost of attendance minus aid already awarded | Typically matches cost minus aid, but some lenders cap aggregate borrowing |

| Payment flexibility | Standard, graduated, extended available; consolidation unlocks income-contingent plan | Fixed term of 5–20 years with limited modification options |

| Upfront fees | 4.228% origination fee deducted from disbursement | Usually zero |

| Cosigner availability | Endorser allowed after denial | Many lenders permit cosigners, potentially reducing rates |

| Forgiveness and discharge | Public Service Loan Forgiveness after consolidation; automatic death/disability discharge | Generally unavailable; discharge terms differ by lender |

Parent Student Loan Rates and Costs

The federal PLUS rate of 8.05% applies universally for loans disbursed during the 2025-2026 school year. Congress adjusts this rate annually based on the 10-year Treasury note plus a fixed margin, so next year's loans might cost 7.8% or 8.3%—you won't know until late spring 2026.

That 4.228% fee substantially increases your true cost. Take a $40,000 loan and you're paying $1,691.20 in fees immediately. Over a standard 10-year repayment, you'll make monthly payments of $486 and pay $18,240 in interest. Total cost: $59,931.20 to borrow $40,000.

Private market rates fluctuate with broader economic conditions and your individual credit profile. Variable rates typically track SOFR (Secured Overnight Financing Rate) plus the lender's margin, which might run 4% to 8%. SOFR currently hovers around 4.5%, so a variable loan with a 3% margin would start at 7.5% but could rise if the Federal Reserve hikes rates.

Fixed-rate private loans provide payment certainty. That same $40,000 at 6.5% fixed over 10 years costs $454 monthly with total interest of $14,480—saving you $3,760 compared to the federal PLUS loan. Factor in zero origination fees and the private loan saves you $5,451 over 10 years.

But raw cost isn't everything. What if you lose your job in year three? Federal loans offer unemployment deferment and income-driven options after consolidation. Private lenders might grant temporary forbearance, but they're not required to help. What if you become disabled at age 58? Federal loans discharge automatically. Many private lenders offer no such protection.

Run the numbers, but also evaluate your risk tolerance and financial stability. A 45-year-old tenured professor with excellent health and strong retirement savings might prioritize the rate savings. A 52-year-old self-employed consultant with health issues might value federal protections despite the higher cost.

Repayment Options and Strategies

Federal PLUS loans technically enter repayment 60 days after your student's school receives the final disbursement for the academic year. In practice, most parents immediately request deferment while their student remains enrolled at least half-time, plus an additional six months after graduation or dropping below half-time.

Deferring payments provides breathing room but costs you. Interest compounds monthly, and when deferment ends, unpaid interest capitalizes—gets added to your principal balance. Defer payments on a $60,000 PLUS loan at 8.05% for four years and you'll accumulate roughly $21,200 in interest. When repayment starts, you owe $81,200, and your monthly payment under standard 10-year repayment jumps to $986 instead of $729.

Standard repayment fixes your payment over 10 years, minimizing total interest but maximizing monthly payments. Graduated repayment starts lower—maybe 50% of the standard payment—and increases every two years. You'll pay substantially more total interest, but it helps if you're juggling other debts.

Extended repayment drops your monthly payment dramatically by stretching the term to 25 years, but you need to owe at least $30,000 across all federal student loans. A $60,000 balance that costs $729 monthly over 10 years drops to $429 monthly over 25 years—but total interest balloons from $27,480 to $68,700.

Income-Contingent Repayment through consolidation helps parents with limited income relative to loan balance. Earn $45,000 annually with $70,000 in PLUS debt? Your payment under ICR might run $200–300 monthly instead of $850. After 25 years of payments, remaining debt forgives—but the IRS treats forgiven amounts as taxable income. Forgive $40,000 and you might owe $10,000 in federal income tax that year.

Private loans rarely offer income-driven options. Your payment is your payment. Miss payments and you default, trashing your credit and potentially triggering lawsuits.

Refinancing both federal and private parent loans can slash rates if market conditions improve or your credit strengthens. Going from 8.05% to 5.5% on $50,000 saves you roughly $6,800 over 10 years. But refinancing federal loans into private loans permanently eliminates federal protections. You can't un-refinance if you later regret it.

The IRS lets you deduct up to $2,500 in student loan interest annually if your modified adjusted gross income falls below $90,000 (single filers) or $180,000 (married filing jointly) as of 2026. The deduction phases out gradually above those thresholds and disappears completely at $105,000 and $210,000 respectively. You can't claim it if you're married filing separately or if someone else claims your child as a dependent.

If your child wants to take over payments, they can—informally. They send money to you, you pay the servicer. Or they make payments directly to the loan servicer on your behalf. But the loan remains in your name. If they stop paying, you're still legally responsible. The only way to truly transfer responsibility is refinancing into a new loan in your child's name, which requires them to qualify based on their own credit and income. A 22-year-old making $42,000 a year will struggle to refinance $60,000 in debt.

Should You Take Out a Parent Student Loan?

Borrowing for college ranks among the most generous financial moves a parent can make. It's also among the riskiest.

Author: Evan Thornton;

Source: sonicmusic.net

The upside: your child can attend their dream school or a program with strong career outcomes without crushing student debt limiting their post-graduation choices. They can focus on academics instead of working 30 hours weekly at the campus bookstore. You might have more borrowing capacity than they do, making parent loans necessary to cover costs.

The downside: you're potentially derailing your own retirement. You can borrow for college; you can't borrow for retirement. Default rates on Parent PLUS loans have climbed in recent years, particularly among parents over 50 who borrowed large amounts. The government doesn't hesitate to garnish Social Security benefits from retirees who default on PLUS loans.

Consider your current financial position honestly. Are you behind on retirement savings? Most 50-year-olds should have roughly 6 times their salary saved for retirement. Have 2 times your salary saved instead? Taking on $40,000 in student debt at 8.05% will further delay your retirement, possibly by years.

Already carrying credit card debt at 22% or a home equity line at 9%? Adding an 8% student loan compounds your debt service burden. Run a debt avalanche calculation to see whether those other debts should get eliminated first.

Alternatives worth exploring: Your student can borrow additional unsubsidized Direct Loans—up to $12,500 annually by junior and senior year. They can also pursue private student loans in their own name, possibly with you as a cosigner. Cosigning still puts you on the hook, but the loan reports on their credit too, helping them build credit history. Many private student loans release cosigners after 24 consecutive on-time payments.

Choosing a less expensive school often makes more financial sense than massive parent borrowing. A regional public university might cost $18,000 annually versus $55,000 at a private college. If both offer solid programs in your student's intended field, the cheaper option prevents you from borrowing $148,000 over four years.

Starting at community college for two years, then transferring, cuts total costs dramatically. Working for a year or two before college to build savings represents another valid path. Taking five years to complete a degree while working part-time beats graduating in four years under a mountain of debt.

Parent loans make sense when the numbers are reasonable relative to your income and retirement timeline. Borrowing $25,000 total over four years when you're 42 years old, earning $95,000 annually, with $350,000 saved for retirement? Manageable. Borrowing $120,000 when you're 54, earning $58,000, with $80,000 saved for retirement? That's a recipe for financial disaster.

Parents often underestimate the impact of student loan debt on their retirement timeline.I've seen clients delay retirement by five or more years because they prioritized their child's education over their own financial security. The kindest thing you can do for your child is maintain your own financial independence

— Jennifer Martinez

How to Apply for Parent Student Loans

For federal Parent PLUS Loans, navigate to studentaid.gov and sign in using your FSA ID—the same username and password you created when completing the FAFSA. Can't remember it? Use the password recovery tool before starting your application.

You'll find the PLUS loan application under the "Apply for Loans" section. The form asks for basic information: your name, Social Security number, date of birth, and your student's details. You'll authorize the Department of Education to pull your credit report. This generates a soft inquiry initially, converting to a hard inquiry only if you proceed after approval.

Most applicants receive a decision within 60 seconds. Approved? You'll immediately complete the Master Promissory Note, a legally binding agreement to repay the loan. One MPN remains valid for up to 10 years, so you won't need to sign a new one each year unless your student transfers schools.

Denied? Don't panic. You have two main options. First, you can add an endorser—someone with clean credit history willing to be equally responsible for the debt. Your spouse, a parent, or a sibling might serve as endorser. Second, you can appeal by documenting extenuating circumstances: medical debt from a serious illness, identity theft, or errors on your credit report. The appeal process takes 2-3 weeks.

If you remain denied even after appeal, your student becomes eligible to borrow additional unsubsidized Direct Loans—$4,000 extra for freshmen and sophomores, $5,000 extra for juniors and seniors. Not ideal, but it helps close the gap.

Private parent student loans require shopping around. Hit up at least three lenders for rate quotes. Most let you check rates through a soft credit inquiry that won't hurt your credit score. You'll enter your income, employment information, and loan amount desired. Within seconds, you'll see whether you prequalify and at what estimated rate.

Once you've selected a lender, you'll complete a full application providing:

- Driver's license or state ID

- Social Security number

- Recent pay stubs (usually last two months)

- W-2s from the most recent tax year

- Possibly your most recent tax return

- Information about your student's school and program

The lender pulls your full credit report (hard inquiry) and verifies your employment—they might call your employer's HR department directly. Most lenders deliver final decisions within 3-5 business days.

After approval, you'll review and electronically sign the loan agreement. Read it thoroughly. What's the interest rate? Fixed or variable? What's the repayment term? Are there prepayment penalties? What happens if you die or become disabled?

The lender then certifies the loan with your student's school, confirming the amount doesn't exceed cost of attendance minus other aid. Certification typically takes 7-10 business days. Once certified, funds disburse directly to the school, usually split across fall and spring semesters.

Timing matters enormously. Start the application process at least 45 days before tuition is due. Many schools impose late payment fees or registration holds if bills aren't paid by their deadline, typically 2-3 weeks before classes start. Coordinate with the financial aid office to understand their processing timeline and avoid surprises.

Author: Evan Thornton;

Source: sonicmusic.net

Frequently Asked Questions

Parent student loans create a pathway for students to attend colleges they couldn't otherwise afford, but that path runs straight through your financial future. The monthly payments you commit to today will compete with your retirement contributions, mortgage, and emergency savings for years or decades.

Before borrowing a single dollar, calculate the true monthly payment and stress-test it against your budget. Can you genuinely afford $450 monthly for 10 years? What if you lose your job? What if your spouse becomes ill and can't work? What if your own parents need financial help?

Explore every alternative first. Push your student to apply for more scholarships—even $1,000 awards add up. Investigate whether they can work 10-15 hours weekly during school. Consider whether a gap year working full-time to save money makes sense. Question whether an expensive private college offers genuinely better career outcomes than your state flagship university.

If you do borrow, borrow conservatively. Just because you qualify to borrow $35,000 doesn't mean you should. Borrow the minimum necessary, understand your repayment options completely, and keep communication open with your student about who's actually making the payments.

Your child's success matters enormously, but your financial security matters too. The greatest gift you can give your child isn't a degree from an expensive college—it's the knowledge that you won't become financially dependent on them in retirement because you over-borrowed for their education. Make choices that work for your entire family's long-term financial health.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.