Student reviewing federal student loan options on a laptop

Department of Education Student Loans Guide

Content

Content

Figuring out how to finance your college education inevitably leads you to the U.S. Department of Education's lending programs—and there are solid reasons why millions of borrowers start here. These aren't standard commercial loans from traditional banks. You're accessing financing that includes protections most lenders would never consider: payment structures that flex downward when your income drops, authorized pauses during financial emergencies, and legitimate paths toward having your remaining debt canceled entirely.

The problem? Most people don't grasp what they've agreed to until they're several years into repayment, frequently overpaying or overlooking programs that could have transformed their financial trajectory.

Let's change that today.

What Are Department of Education Student Loans?

Today's federal student lending operates through a single program—the William D. Ford Federal Direct Loan system, which places the U.S. government directly in the position of your lender rather than using banks as intermediaries. Here's what this structure means for you: companies such as MOHELA or Nelnet act as your loan servicer, managing billing and collecting your payments. But they're contractors, not the actual entity that owns what you owe.

The distinction between federal and private financing runs deep. Commercial lenders evaluate your credit history and make approval decisions accordingly. They establish rates that fluctuate based on your financial profile. Fall behind on payments? You're dealing with collections departments motivated primarily by recovering maximum dollars.

The federal system operates under different principles entirely. Your interest rate gets determined by Congressional legislation—identical rates for everyone borrowing during that academic year, with zero consideration of your credit profile. Your earning power determines what you pay monthly under most available plans. And debt cancellation programs? They're written into law, though successfully navigating them requires substantial effort.

Credit checks don't factor into most undergraduate federal borrowing whatsoever. You won't need someone to cosign, which becomes enormously significant when your parents either cannot or will not participate financially. PLUS loans designated for graduate students and parents do involve credit screening, but evaluators look specifically for severe negative factors—recent bankruptcy filings, current defaults, major payment delinquencies within the past several years. Simply having mediocre credit won't eliminate your eligibility.

Accessing these funds requires either U.S. citizenship or qualified immigration documentation. You'll need enrollment status of at least half-time in a degree-granting or certificate program at an institution participating in federal student aid. Maintaining satisfactory academic progress also becomes mandatory, which schools typically define as completing sufficient credits each semester while keeping your GPA above minimum thresholds.

Every federal loan starts with the FAFSA—your Free Application for Federal Student Aid. This isn't a one-time submission. You'll complete this annually for each year you're seeking funding. Skip submitting during any year? No federal loan eligibility exists for that academic period, regardless of prior qualification.

Author: Evan Thornton;

Source: sonicmusic.net

Types of Department of Education Loan Programs

Federal lending divides into four primary categories, each structured for particular circumstances and carrying specific terms you should understand completely before accepting any funding.

Direct Subsidized Loans offer the strongest financial terms available anywhere. Eligibility extends only to undergraduate students whose FAFSA demonstrates financial need. The transformative feature: throughout your enrollment period (maintaining at least half-time status), the six-month grace window after you stop attending, and during any approved deferment periods, the federal government absorbs all accumulating interest. That's money you'll never repay. Consider a student requiring five years to complete their bachelor's degree—that interest subsidy can preserve thousands of dollars compared to unsubsidized alternatives where interest compounds from day one.

Direct Unsubsidized Loans become available to all qualifying students—undergraduate, graduate, professional degree programs, no exceptions. Financial need plays no role in eligibility. The obvious compromise: interest begins accumulating immediately upon disbursement to your school. Most students ignore that mounting interest throughout their enrollment years, and when they graduate, it capitalizes—meaning your principal balance permanently increases and you're subsequently charged interest on what was previously just interest. A $30,000 unsubsidized loan balance can balloon past $35,000 by graduation day even without making a single payment.

Direct PLUS Loans serve two completely different borrower categories. Parents can access these to cover educational expenses for their dependent undergraduate children. Graduate and professional students can borrow for their own advanced education. These loans require credit evaluation—the government verifies you haven't experienced catastrophic recent credit events. Interest rates on PLUS loans consistently run higher than subsidized or unsubsidized options, typically by 2.5 to 3 percentage points. Across a decade or two of repayment, that rate differential compounds into substantial additional cost.

Direct Consolidation Loans allow merging multiple federal loans into one single loan. This doesn't reduce your interest rate—instead, you receive a weighted average of your current rates, rounded upward to the nearest one-eighth of a percentage point. Why would anyone consolidate then? It unlocks certain repayment structures and forgiveness programs exclusively available to Direct Loan borrowers. If you're carrying older FFEL program loans from before 2010, consolidating converts them into Direct Loans, creating eligibility for Public Service Loan Forgiveness.

| Loan Category | Current Interest Rate | Eligibility Requirements | Maximum Annual Borrowing | Interest Subsidy Available? |

| Direct Subsidized | 5.50% | Undergraduate students demonstrating financial need | $3,500 to $5,500 based on your year in the program | Yes—throughout enrollment, six-month grace period, and approved deferments |

| Direct Unsubsidized | 5.50% for undergraduate students; 7.05% for graduate/professional students | Any student meeting basic eligibility | $5,500 to $20,500 after deducting any subsidized loan amounts | No—interest begins accruing immediately at disbursement |

| Direct PLUS | 8.05% | Parents of dependent undergraduates; students in graduate/professional programs | Full cost of attendance minus all other financial assistance | No—interest begins accruing immediately at disbursement |

| Direct Consolidation | Weighted average of consolidated loans, rounded up to nearest 1/8 percent | Anyone holding multiple federal student loans | Not applicable—combines existing debt | No—interest continues accruing on the consolidated balance |

These rates apply specifically to loans disbursed between July 1, 2025, and June 30, 2026. Each July 1st, Congress resets these percentages based on May's 10-year Treasury note auction results, plus statutory add-on percentages. If your borrowing occurred in earlier years, your rates will differ—but once set, they remain fixed for that loan's entire lifespan.

How to Apply for Federal Education Student Loans

FAFSA applications open October 1st for the academic year beginning the following fall semester. This early availability carries significance: many state agencies and institutional financial aid offices distribute funds on a first-come, first-served basis. Delay your submission until spring? You risk missing out on grants and subsidized loan allocations, even when your financial circumstances technically qualify you.

Most colleges establish priority deadlines falling in February or March. Submit before that cutoff and reviewers consider your application while their full aid budget remains available. Miss the priority deadline and you're competing for whatever funding hasn't been committed yet.

You'll need Social Security numbers for yourself and, if you're a dependent student, your parents as well. Federal tax information from two years prior becomes necessary (meaning 2023 tax data for applications covering the 2025-26 academic year). Documentation of untaxed income—child support receipts, veteran's benefits, housing allowances. Current account statements reflecting balances in checking accounts, savings, and any investment holdings.

The IRS Data Retrieval Tool imports tax information automatically, accelerating processing and eliminating transcription errors that might trigger your application for verification—a tedious bureaucratic process demanding additional documentation submission to your school's financial aid office.

After submission, the Education Department calculates your Student Aid Index (this replaced the Expected Family Contribution terminology). Your SAI doesn't represent what you'll actually spend out-of-pocket—schools use this figure in their formulas determining need-based aid qualification.

Your college receives your SAI and constructs your financial aid offer: grants requiring no repayment, work-study earning opportunities, and available loan options. This information arrives via an award letter, usually 2-4 weeks after the institution admits you.

Here's what catches students off-guard: accepting every offered loan isn't mandatory. Numerous borrowers take the maximum available simply because the system offers it, then graduate carrying double the debt their situation actually required. Accept only amounts necessary after accounting for grants, scholarships, work-study, and whatever your family contributes.

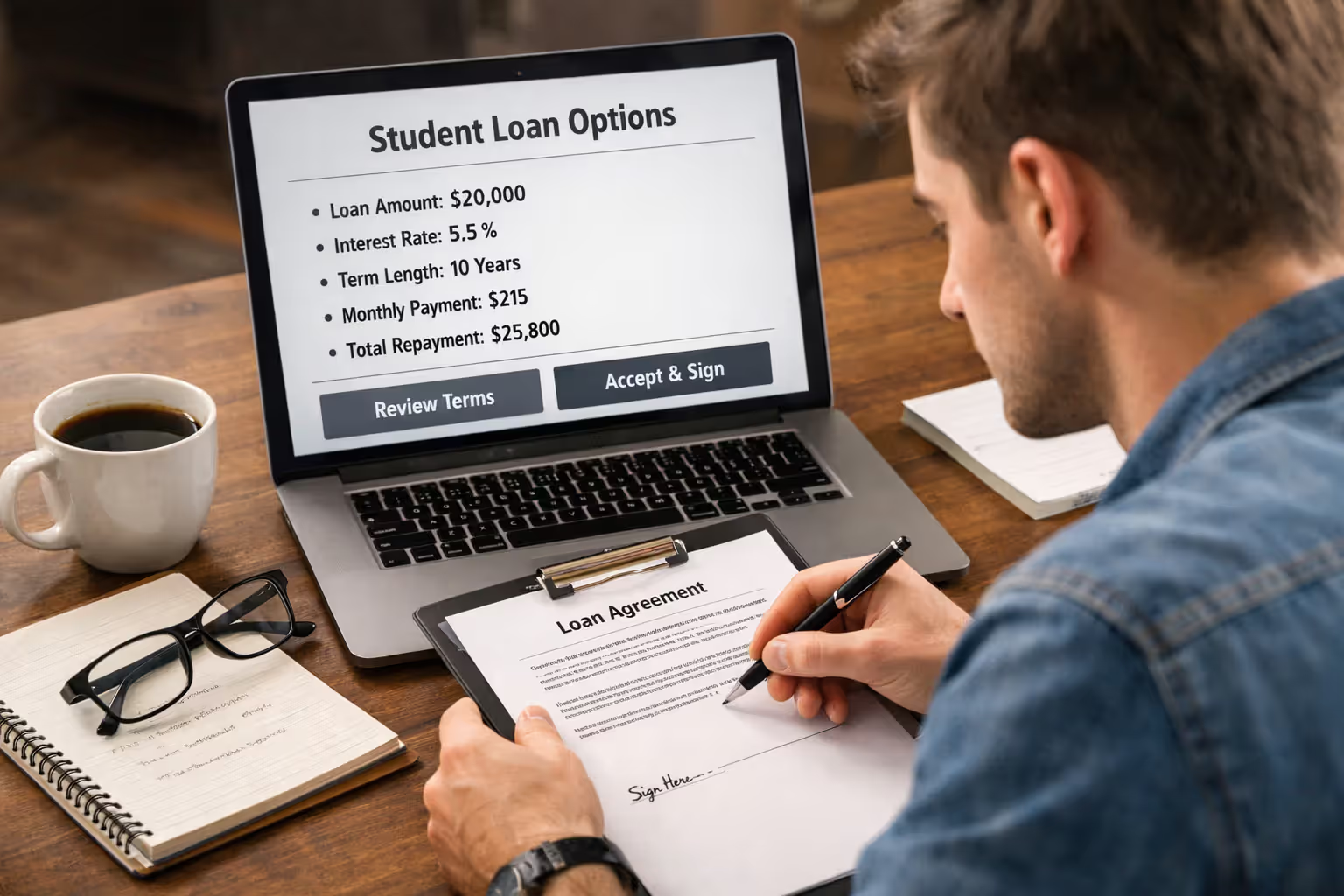

First-time borrowers complete entrance counseling online—an interactive educational session explaining your repayment obligations. You'll also execute a Master Promissory Note, the legally binding contract obligating you to repay borrowed amounts with interest. Both requirements consume roughly 30 minutes combined. A single MPN covers multiple borrowing years within a 10-year period, so you'll typically complete this process just once.

Author: Evan Thornton;

Source: sonicmusic.net

Repayment Plans and Options

Eight distinct repayment structures exist, each calculating your monthly obligation differently and extending across varying timeframes. Your selection profoundly impacts both your total repayment amount and how many years this debt follows you.

Standard Repayment divides your balance into equal monthly amounts across 10 years. This approach costs the least in total interest but demands the highest monthly payment. Someone owing $30,000 at 6% interest pays approximately $333 each month, with roughly $9,967 going toward interest across the decade. From a pure financial perspective, this represents the optimal choice if your budget can handle it.

Graduated Repayment launches with reduced payments that increase every two years, often doubling by your final payment years. You still eliminate the debt within 10 years, but you'll surrender considerably more to interest than standard repayment—sometimes several thousand dollars more. This structure bets on your earnings climbing steadily. If that income growth doesn't materialize, those scheduled payment increases become financially brutal.

Extended Repayment stretches payments across 25 years using either fixed or graduated structures. Qualification requires owing over $30,000 in Direct Loans. Monthly obligations drop dramatically—that $30,000 loan decreases from $333 monthly down to perhaps $180. But you'll ultimately pay more than double the interest across the loan's lifespan, easily exceeding $20,000 in interest charges alone.

Income-Driven Repayment structures calculate payments using your discretionary income and household size rather than your loan balance. Four distinct versions currently exist: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Saving on a Valuable Education (SAVE), and Income-Contingent Repayment (ICR).

SAVE, which achieved full implementation in 2024, delivers the most favorable terms for the majority of borrowers. Undergraduate debt gets capped at 5% of discretionary income, while graduate debt caps at 10%. Discretionary income represents everything you earn exceeding 225% of federal poverty guidelines—shielding more of your paycheck than earlier IDR versions protected.

The significant advantage emerges at year 20 (or year 10 for borrowers whose original balance was under $12,000): any remaining balance gets completely forgiven. If you're employed in qualifying public service positions, you might access forgiveness after just 10 years through PSLF.

| Plan Name | Monthly Payment Calculation Method | Repayment Duration | Forgiveness Eligibility | Best Suited For |

| Standard | Fixed payment amount calculated to eliminate debt in 10 years | 10 years | No forgiveness available | Borrowers who can manage higher payments and prioritize minimizing total interest costs |

| Graduated | Lower initial payments that increase every 24 months | 10 years | No forgiveness available | People confident their earnings will increase substantially and predictably |

| Extended | Fixed or graduated payments stretched over 25 years | 25 years | No forgiveness available | Large debt balances where annual IDR recertification hassle outweighs benefits |

| SAVE | 5% of discretionary income for undergraduate debt; 10% for graduate debt | 20-25 years | Yes, remaining balance forgiven after required payment period | Lower-income earners, public service professions, anyone strategically pursuing forgiveness |

| PAYE | 10% of discretionary income, never exceeding standard 10-year payment | 20 years | Yes, remaining balance forgiven after required payment period | Borrowers whose first loan disbursed before October 2007 and who received disbursements after October 2011 |

| IBR | 10-15% of discretionary income depending on when borrowing began | 20-25 years | Yes, remaining balance forgiven after required payment period | Borrowers who don't qualify for PAYE but want income-based payment calculations |

You're allowed to switch plans whenever circumstances change by contacting your servicer. But understand this consequence: transitioning from an IDR plan into standard or graduated repayment triggers capitalization of accumulated unpaid interest, permanently inflating your principal balance. Calculate the numbers thoroughly before making this move.

Department of Education Loan Help and Forgiveness Programs

Multiple programs discharge or forgive federal student debt under specific circumstances. Most borrowers remain unaware these options exist until financial desperation hits—and by that point, they've frequently missed opportunities to position themselves for eligibility.

Public Service Loan Forgiveness (PSLF) eliminates your remaining balance after completing 120 qualifying payments while employed full-time with qualifying employers. This includes organizations at every government level—federal agencies, state departments, local municipalities, or tribal governments all qualify. Registered 501(c)(3) nonprofit organizations qualify automatically. Private nonprofits delivering certain public services potentially qualify as well.

Each qualifying payment must occur while you're enrolled in an income-driven plan or the 10-year standard plan. You must maintain full-time employment status (defined as 30+ hours weekly at most organizations) with a qualifying employer during each payment period.

PSLF's initial implementation proved catastrophic—rejection rates exceeded 90% for early applicants. Servicer mistakes, borrowers holding wrong loan types, confusion about qualifying employment all contributed. Recent reforms and the temporary PSLF waiver (which expired in October 2022) helped over 400,000 borrowers achieve forgiveness. The critical lesson: file Employment Certification Forms annually to document your progress and identify problems years before you reach the 120-payment threshold.

Teacher Loan Forgiveness provides up to $17,500 after completing five consecutive years teaching full-time in schools serving low-income communities. Math, science, and special education teachers at the secondary level qualify for the complete $17,500. Other full-time teachers qualify for up to $5,000. The limitation: those five years cannot simultaneously count toward PSLF. You must select one program or the other for any given employment period.

Total and Permanent Disability Discharge cancels your federal student loans when medical conditions prevent you from working. The Department accepts documentation from three sources: Social Security Administration disability determinations, Department of Veterans Affairs disability ratings, or physician certification of total and permanent disability. Following discharge approval, you enter a three-year monitoring period. If you earn above poverty guideline thresholds during monitoring, you may be required to resume repayment.

Author: Evan Thornton;

Source: sonicmusic.net

Borrower Defense to Repayment discharges loans when your school engaged in misleading practices or violated state laws in ways directly relating to your loans or educational services received. Think institutions like Corinthian Colleges, ITT Technical Institute, and similar predatory schools. Applications demand detailed evidence of specific institutional misconduct and explicit connections between that misconduct and the financial harm you experienced.

Deferment and forbearance temporarily suspend your payment obligations. During deferment periods, subsidized loans don't accrue interest (though unsubsidized loans do). Forbearance accumulates interest on all loan types. Qualifying circumstances for deferment include economic hardship, unemployment, cancer treatment, and active military deployment. Forbearance approval comes easier but costs you more long-term as interest compounds throughout the forbearance period.

The biggest mistake borrowers make is not exploring income-driven repayment plans early. These plans prevent default, preserve credit, and create a pathway to forgiveness that many borrowers don't realize exists until they're already in financial crisis

— Mark Kantrowitz

Managing Your Student Loans Through the Education Department

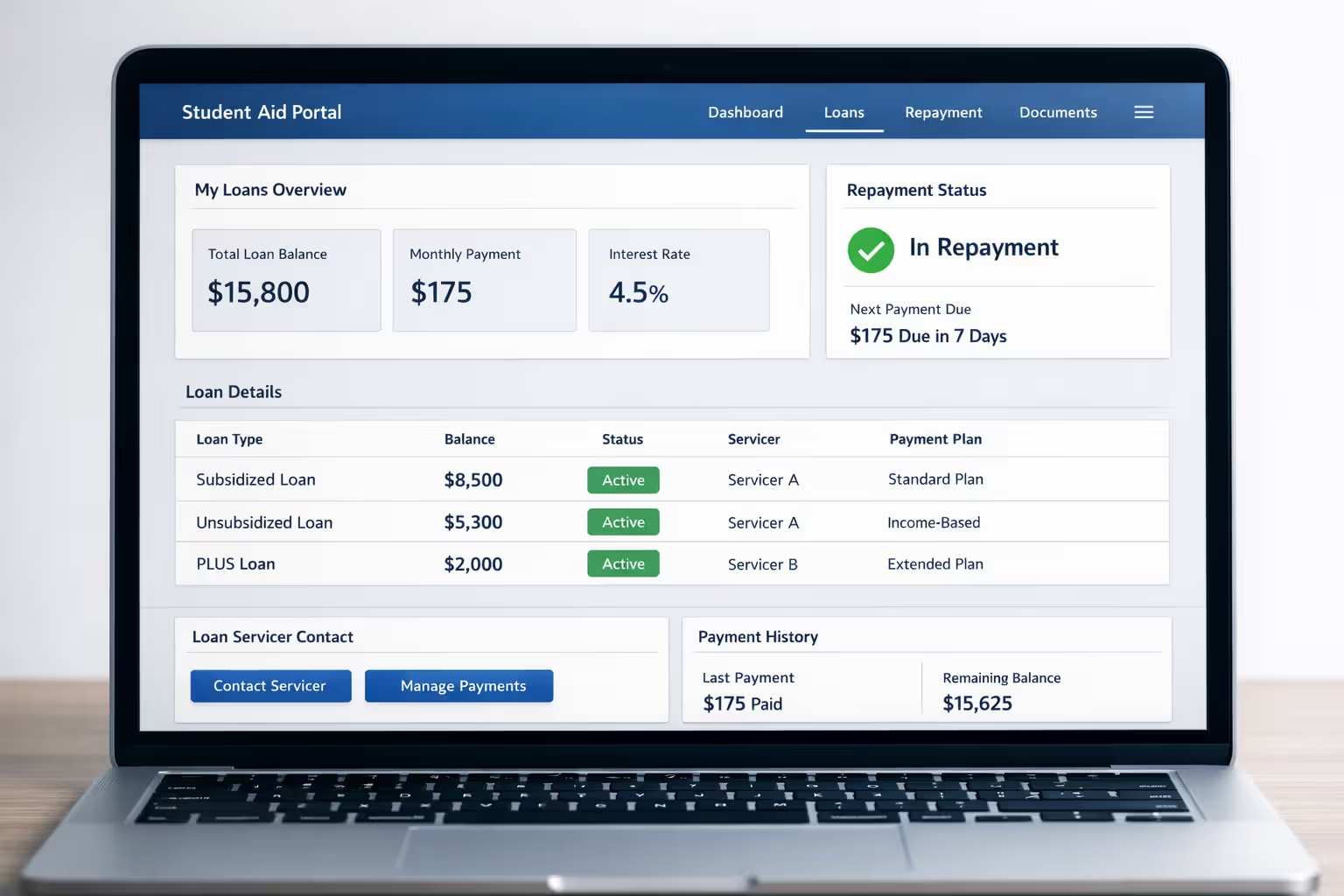

The Education Department assigns a loan servicer to your account—borrowers don't select their servicer. Current servicing companies include MOHELA, Aidvantage, EdFinancial, Nelnet, and several others. These contractors handle your monthly billing, process incoming payments, and manage day-to-day account operations on the government's behalf.

StudentAid.gov functions as your centralized dashboard for everything related to federal financial aid. Logging in reveals all your federal loans, displays your servicer's contact details, shows current interest rates, lists disbursement dates, and tracks repayment status. This should be your primary resource for any questions, and you should review it quarterly to identify errors before they compound.

When your address changes, phone number updates, or you establish a new email account, update this information immediately through both StudentAid.gov and directly with your loan servicer. Borrowers who miss critical communications frequently discover they've been switched from income-driven plans back to standard repayment because they missed annual recertification deadlines. That can spike your monthly obligation from $150 to $600 instantly.

Author: Evan Thornton;

Source: sonicmusic.net

Preventing default deserves your absolute priority attention. Federal loans enter default status after 270 consecutive days without payment—approximately nine months. Default devastates your credit score, authorizes wage garnishment without requiring court proceedings, intercepts federal and state tax refunds, and eliminates eligibility for future federal aid. The government retains authority to sue you for the balance, and bankruptcy discharge remains nearly impossible for student loans.

Struggling with payments? Contact your servicer before missing any due date. Switch into income-driven repayment (your payment might calculate to zero if income is sufficiently low). Request deferment or forbearance if circumstances qualify you. Ignoring past-due notices guarantees worse outcomes and eliminates options.

Loan rehabilitation lets you repair a defaulted loan by completing nine "reasonable and affordable" monthly payments within a 10-month window. The default notation gets removed from your credit reports (though prior late payment marks remain visible). You regain eligibility for deferment, forbearance, and federal student aid. The significant limitation: rehabilitation works only once per loan.

Consolidation also cures default status immediately and creates instant eligibility for income-driven plans. But the default notation remains on your credit reports for seven years. Choose consolidation when you need immediate relief and cannot wait 10 months for rehabilitation to complete.

Common Mistakes Borrowers Make with Federal Student Loans

Missing FAFSA deadlines directly costs you money. States and colleges distribute aid budgets until funds are exhausted. Submit late and you'll likely receive reduced awards or nothing, even when your financial circumstances qualify you for need-based aid. Create a recurring October 1st reminder and complete your FAFSA within the first 30 days whenever possible.

Ignoring interest capitalization generates unpleasant surprises down the road. When unpaid interest gets added to your principal balance, you start paying interest on that interest—compound interest working aggressively against you. Capitalization occurs when you complete or leave school, exit deferment or forbearance periods, miss your IDR plan annual recertification deadline, or consolidate loans. Paying even modest amounts toward interest before it capitalizes saves substantial money over your loan's lifespan.

Treating servicer communications like junk mail causes missed opportunities and compliance problems. These aren't credit card marketing offers—they're annual loan statements, recertification reminders, and policy updates directly affecting your repayment. Open every servicer communication immediately and respond before stated deadlines pass. Register for electronic delivery so messages reach you even when physical addresses change.

Defaulting to the wrong repayment structure costs thousands unnecessarily. Many borrowers automatically land in standard repayment without evaluating income-driven alternatives. Others select extended repayment when IDR would cost less over time and offer forgiveness eligibility. The Loan Simulator tool at StudentAid.gov lets you compare plans using your actual loan data—use it before making decisions.

Borrowers pursuing PSLF sometimes mistakenly make payments under graduated or extended repayment plans, which don't count toward the 120 qualifying payments. Others make extra principal payments thinking it accelerates forgiveness, but PSLF specifically requires exactly 120 payments—paying extra just costs you money without providing any benefit.

Frequently Asked Questions About Department of Education Student Loans

Department of education student loans deliver protections and flexibility that private commercial loans simply cannot match—but only when you actually understand and actively use those features. The difference between manageable repayment and years of financial crisis typically comes down to three factors: selecting the right repayment plan for your specific situation, maintaining consistent communication with your servicer, and knowing which forgiveness programs you might potentially qualify for.

Begin with StudentAid.gov today. Review your complete loan portfolio. Confirm your current servicer assignment and active repayment plan. Run the Loan Simulator to determine whether a different plan would save money or better align with your career trajectory. Working in public service roles or for nonprofit organizations? Submit an Employment Certification Form immediately to begin tracking PSLF progress, even if you're years away from reaching 120 qualifying payments.

Establish autopay to capture the 0.25% interest rate reduction most servicers provide—and to eliminate missed payments that damage credit scores. Create annual calendar reminders to recertify income-driven plans before deadlines pass. Schedule a yearly comprehensive review of your repayment strategy as your income and life circumstances evolve.

These loans represent substantial financial commitments, but they're simultaneously investments in enhanced earning potential and expanded career opportunities. Managing them strategically instead of just making minimum payments and hoping everything works out can preserve tens of thousands of dollars and help you achieve financial freedom years earlier than you might expect.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.