Student reviewing student loan account on laptop at home

Student Loan Servicers Guide

Content

Content

Understanding who manages your student loans can save you from missed payments, lost paperwork, and thousands of dollars in avoidable fees. Your loan servicer acts as the middleman between you and the entity that funded your education, yet many borrowers don't realize their servicer exists until something goes wrong.

What Is a Student Loan Servicer?

A student loan servicer is a company that handles the day-to-day administration of your student loans. Think of them as the customer service department for your debt. While the U.S. Department of Education or a private bank owns your federal or private loans, the servicer manages billing, processes payments, and answers questions about your account.

This distinction matters because many borrowers confuse their servicer with their lender. The lender provided the money you borrowed. The servicer collects it back. For federal loans, the Department of Education assigns your servicer—you don't get to pick. Private loan servicers are typically chosen by the bank or credit union that issued your loan.

Servicers earn money through contracts paid by loan holders, not through interest on your debt. Federal servicers receive a monthly fee per borrower account they manage, which creates a business model focused on volume rather than personalized service. This explains why customer service quality varies widely across student loan servicing companies.

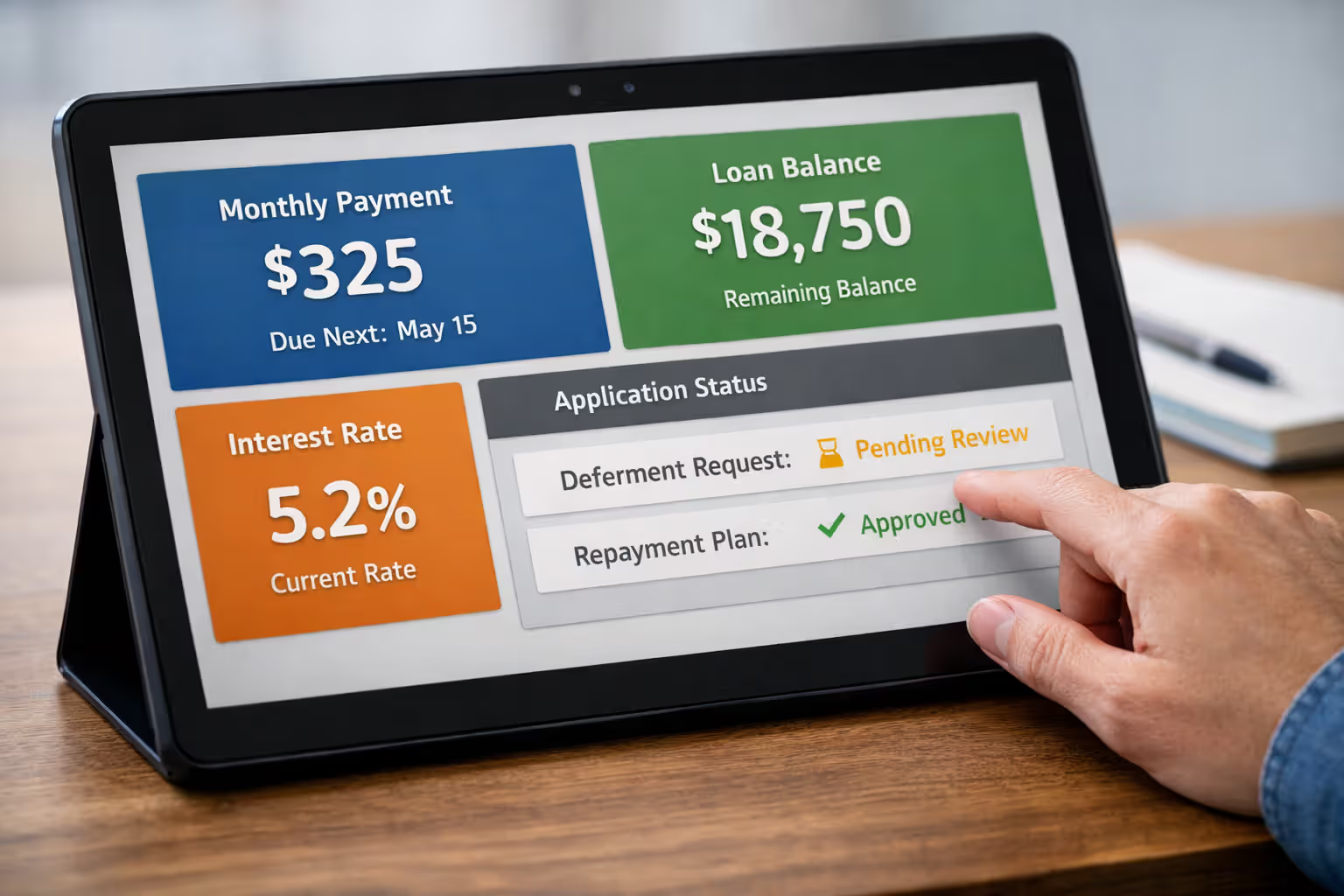

Your servicer's responsibilities include calculating your monthly payment, applying funds to principal and interest, tracking your loan balance, and managing requests for deferment or forbearance. If you qualify for an income-driven repayment plan or Public Service Loan Forgiveness, your servicer processes those applications and tracks your progress.

Author: Olivia Harrington;

Source: sonicmusic.net

How to Find Your Student Loan Servicer

Locating who services your federal loans takes about two minutes. Visit StudentAid.gov and log in using your FSA ID. Once inside your dashboard, scroll to the "My Aid" section. Every federal loan you've taken out appears here, along with the servicer's name, contact information, and current balance. If you've never created an FSA ID, you'll need to set one up—the process requires identity verification and takes one to three days.

For private student loans, check your email inbox for monthly billing statements. The sender is your servicer. If you've changed email addresses or deleted old messages, pull your credit report from AnnualCreditReport.com. Each loan listing includes the creditor's name, which is usually your servicer. Look in your files for the original loan agreement or promissory note; the servicer's contact information should appear on recent correspondence.

Some borrowers have loans with multiple servicers, especially if they attended school across several years or took out both federal and private loans. Federal loans from different years might be assigned to different servicers based on when the Department of Education's contracts changed. Private loans from different lenders will almost certainly have separate servicers.

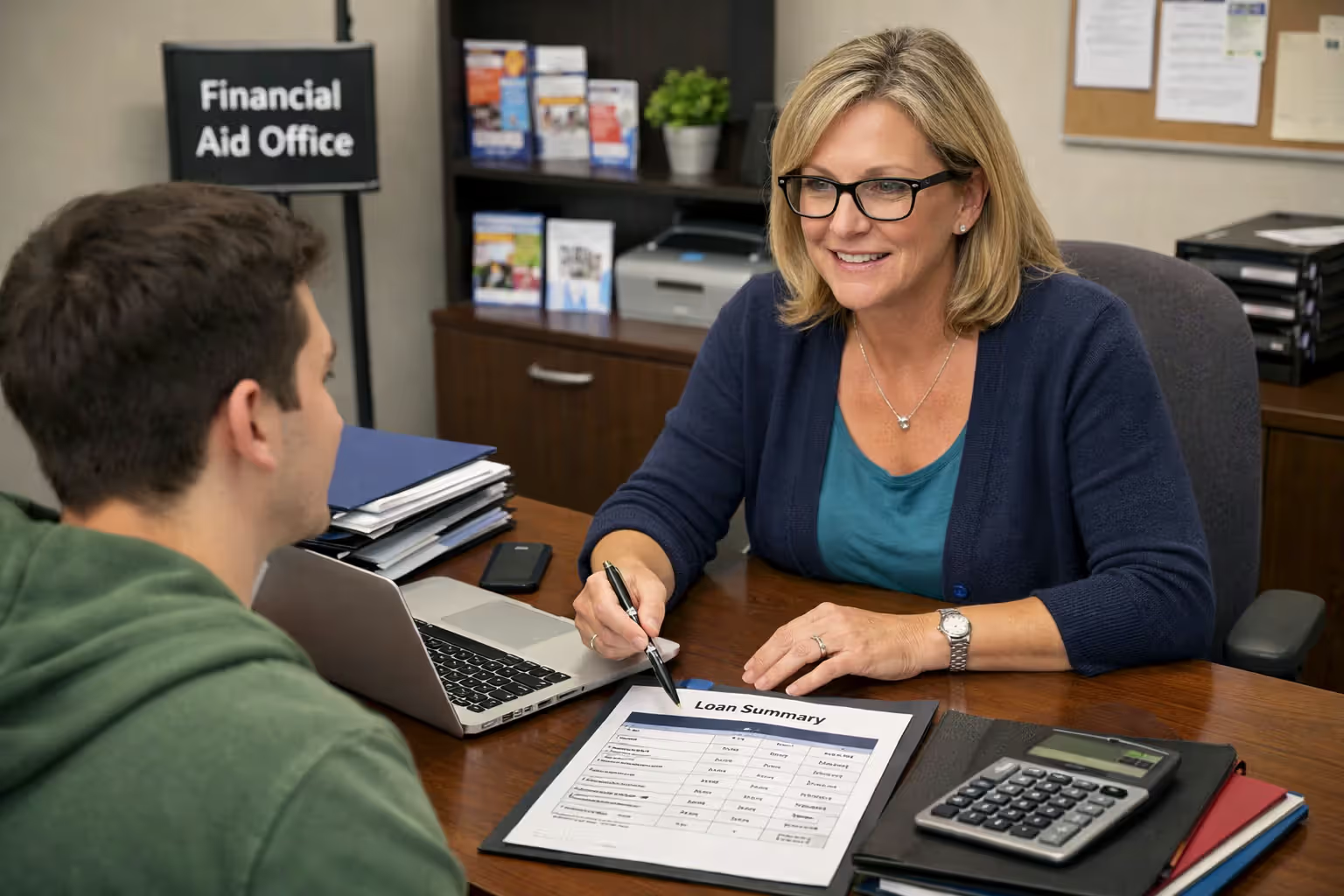

If you're still stuck, contact your school's financial aid office. They maintain records of the loans you took out while enrolled and can point you toward the right servicer. This works even if you graduated years ago.

Author: Olivia Harrington;

Source: sonicmusic.net

Major Student Loan Servicing Companies

The student loan servicing landscape changed dramatically between 2021 and 2024, when several major companies exited federal loan servicing. As of 2026, the industry has stabilized around a smaller group of servicers handling federal loans, while private loan servicing remains fragmented across dozens of companies.

Federal Loan Servicers

The Department of Education currently contracts with five primary servicers for federal student loans. MOHELA (Missouri Higher Education Loan Authority) manages the largest portfolio, including most borrowers pursuing Public Service Loan Forgiveness. Aidvantage, operated by Maximus, took over accounts from Navient when that company left federal servicing. EdFinancial Services continues servicing loans under its long-standing contract. Nelnet remains a major player, particularly for borrowers who consolidated loans in recent years. OSLA Servicing handles a smaller portfolio focused on specific loan types.

Each servicer offers online account management, mobile apps, and phone support, though quality and wait times vary. MOHELA faced significant criticism during 2023 and 2024 for processing delays related to PSLF applications, leading to improved staffing and systems by 2025. Aidvantage struggled with account transfers but has since streamlined its platform.

| Servicer Name | Contact Number | Website | Loan Types Serviced | Key Online Features |

| MOHELA | 1-888-866-4352 | mohela.com | Direct Loans, FFEL, PSLF tracking | Payment estimator, PSLF form upload, auto-pay setup |

| Aidvantage | 1-800-722-1300 | aidvantage.com | Direct Loans, FFEL | Mobile app, repayment plan comparison tool |

| EdFinancial | 1-855-337-6884 | edfinancial.com | Direct Loans, FFEL | Paperless billing, deferment requests, cosigner release |

| Nelnet | 1-888-486-4722 | nelnet.com | Direct Loans, FFEL | Loan simulator, text/email alerts, budget calculator |

| OSLA Servicing | 1-866-264-9762 | myosla.org | Direct Loans, consolidation loans | Payment history downloads, tax form access |

Private Loan Servicers

Private student loan servicing is less centralized. Navient still services private loans despite exiting federal servicing. SoFi, Earnest, and CommonBond service loans they originated themselves. Discover and Sallie Mae handle their own loan portfolios. Citizens Bank, PNC, and Wells Fargo service private education loans through in-house departments or third-party contractors like Firstmark Services and PHEAA.

The servicer for your private loan depends entirely on who issued it. Refinancing your private loans means getting a new servicer along with your new interest rate and terms.

What Your Loan Servicer Does for You

Your servicer sends monthly billing statements at least 21 days before your payment due date. These statements break down how much you owe, where your payment goes (principal versus interest), and your remaining balance. Servicers process payments received online, by mail, by phone, or through automatic debit. They apply payments according to federal regulations or your loan agreement, typically covering interest first, then principal.

When you need to change repayment plans—switching from a standard 10-year plan to an income-driven option, for example—your servicer handles the paperwork. They calculate what you'll pay under different scenarios and recertify your income annually for income-driven plans. If you experience financial hardship, your servicer processes forbearance and deferment requests, temporarily pausing or reducing payments.

Servicers maintain your account history, including every payment you've made and any periods of deferment or forbearance. This record matters enormously for loan forgiveness programs. Public Service Loan Forgiveness requires 120 qualifying monthly payments, and your servicer tracks this count. Mistakes in tracking have cost borrowers years of progress toward forgiveness.

Your servicer also handles less common situations: processing disability discharge applications, calculating refunds for overpayments, updating your contact information, and managing cosigner releases on private loans. They're your first point of contact for questions about your loan terms, interest rates, or outstanding balance.

Common Problems With Student Loan Servicers

Payment misapplication ranks among the most frequent complaints. Borrowers make extra payments intending to reduce principal, but servicers apply the money to future interest or advance the due date instead of lowering the balance. Federal regulations allow borrowers to specify how extra payments should be applied, but servicers sometimes ignore these instructions. Always indicate "apply to principal" when making additional payments and verify the allocation on your next statement.

Communication failures frustrate borrowers who can't reach representatives or receive conflicting information. Wait times stretched to 90 minutes during peak periods in 2023, though most servicers now average 15 to 30 minutes. Representatives sometimes provide incorrect guidance about repayment options or forgiveness eligibility, leading borrowers to make poor decisions. Document every conversation: note the date, time, representative's name, and advice given.

Incorrect payment counts for Public Service Loan Forgiveness have triggered lawsuits and federal investigations. Servicers undercounted qualifying payments due to administrative errors, costing borrowers months or years toward forgiveness. The Department of Education conducted a one-time recount in 2022-2023, correcting many errors, but ongoing tracking remains imperfect. Request an updated payment count at least annually and dispute discrepancies immediately.

Account access issues spike during servicer transfers. Borrowers lose access to online accounts, can't make payments, or see incorrect balances during transitions. Automatic payments sometimes fail when accounts move, triggering late fees and credit damage. During any transfer, monitor your accounts closely and keep confirmation of every payment you make.

To file a complaint about your federal loan servicer, submit a report through the Federal Student Aid Feedback System at StudentAid.gov. The Consumer Financial Protection Bureau accepts complaints at consumerfinance.gov and tracks patterns across servicers. For private loans, complaints go to the CFPB and your state attorney general's office. Complaints trigger investigations and sometimes result in account corrections or compensation.

Author: Olivia Harrington;

Source: sonicmusic.net

When Your Loan Servicer Changes

Servicer transfers happen when the Department of Education awards new contracts, when servicers exit the business, or when loans are sold or consolidated. You should receive notice at least 15 days before the transfer, though sometimes notifications arrive late or get lost in spam folders. Federal law requires both your old and new servicer to notify you.

During a transfer, your loan terms don't change. Your interest rate, repayment plan, and forgiveness progress remain the same. What changes is where you send payments and who answers your questions. Your old servicer stops accepting payments on a specific date, and your new servicer takes over the next day. Any payment you made to your old servicer before the cutoff counts; payments sent after the cutoff should go to your new servicer.

Protect yourself during transitions by downloading all account documents before the transfer. Save payment history, tax forms, correspondence about repayment plans, and any forgiveness tracking documents. Create an account with your new servicer as soon as you receive transfer notification. Set up automatic payments with the new servicer to avoid missed payments during the transition.

Verify that your new servicer has accurate information. Check that your repayment plan, income certification, and forgiveness payment count transferred correctly. Errors during transfers are common—borrowers enrolled in income-driven repayment have been switched to standard plans, and PSLF counts have been reset to zero. Dispute any errors within 30 days of discovering them.

The single biggest mistake borrowers make is assuming their servicer will protect their interests.Servicers are administrative companies, not advocates. Keep your own records, verify every statement, and don't rely on verbal promises. If it's not in writing, it didn't happen

— Marcus Chen

Frequently Asked Questions About Student Loan Servicers

Your student loan servicer controls access to repayment options, tracks progress toward forgiveness, and determines whether your account stays in good standing. Knowing who services your loans, maintaining your own records, and verifying your servicer's work protects you from costly errors. Check your account quarterly, respond promptly to servicer communications, and don't hesitate to escalate problems through official complaint channels. The servicer works for your loan holder, not for you—but understanding how they operate gives you the tools to manage your debt effectively and avoid the pitfalls that trap unprepared borrowers.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.