Graduation cap placed on stack of dollar bills next to calculator and loan amortization document on office desk

How Student Loan Interest Works?

Student loan interest represents the cost of borrowing money for your education. While most borrowers understand they'll pay back more than they borrowed, the mechanics of how that interest accumulates—and when—often remain unclear until the first payment arrives. Understanding these details can save you thousands of dollars over the life of your loans.

What Is Student Loan Interest

Student loan interest is the fee lenders charge for providing you with educational funding. When you borrow $10,000, you don't just repay that $10,000—you also pay a percentage of the outstanding balance as compensation to the lender.

Most student loans use simple daily interest, which means your lender calculates interest based on your current principal balance each day. The formula is straightforward: (outstanding principal × interest rate) ÷ 365 = daily interest charge. If you have a $20,000 loan at 5% interest, you'll accrue approximately $2.74 in interest each day ($20,000 × 0.05 ÷ 365).

This differs from compound interest, where interest charges get added to your principal and then generate their own interest. Student loans don't technically compound continuously, but they do experience capitalization—specific moments when unpaid interest gets added to your principal balance. Once capitalized, that former interest becomes part of your principal and generates its own interest charges going forward.

When you make a payment, your lender typically applies it to accrued interest first, then to the principal. This sequencing matters because only payments that reduce your principal will lower your future interest charges. A $300 monthly payment might include $150 in interest and $150 toward principal in the early years of repayment.

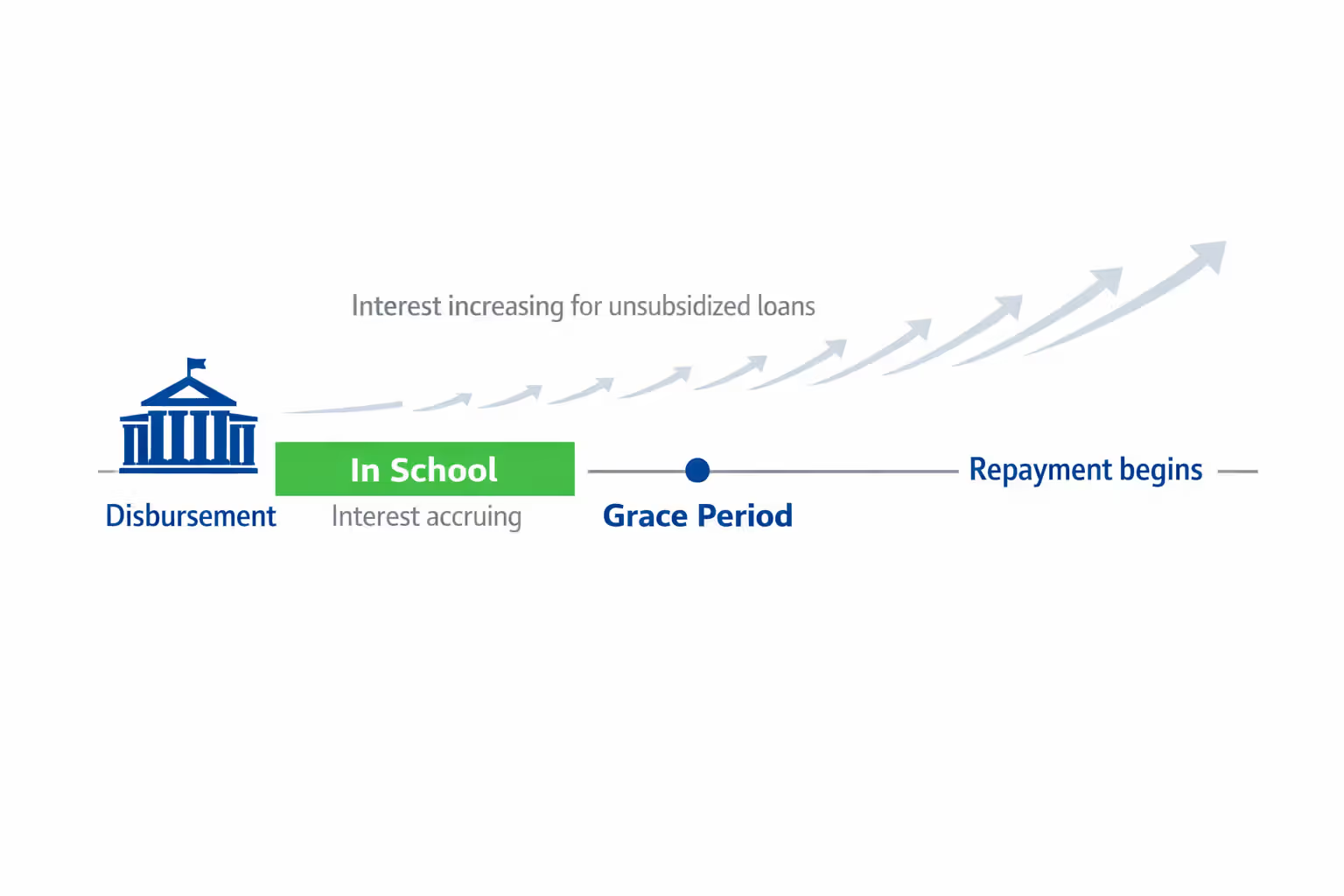

When Does Interest Start Accruing on Student Loans

The timing of when interest begins depends entirely on your loan type. Federal subsidized loans offer a unique benefit: the Department of Education pays your interest while you're enrolled at least half-time, during your grace period, and during certain deferment periods. This means a subsidized loan borrowed in your freshman year won't accumulate any interest until six months after you graduate or drop below half-time enrollment.

Federal unsubsidized loans, Graduate PLUS loans, and Parent PLUS loans start accruing interest the moment your school receives the loan disbursement. If your university gets your loan funds on September 1 of your freshman year, interest begins that same day—even though you won't enter repayment for years.

Author: Danielle Pierce;

Source: sonicmusic.net

Private student loans almost always begin accruing interest immediately upon disbursement. Some private lenders offer in-school deferment options, but interest continues accumulating in the background. A few private lenders provide interest-only payment plans during school, allowing you to pay the monthly interest charges without touching the principal.

In-School Interest Accrual

For unsubsidized federal loans and most private loans, four years of undergraduate education means four years of interest accumulation before you make your first standard payment. On a $5,000 unsubsidized loan at 6.5% interest, you'll accumulate approximately $1,300 in interest during a four-year degree if you make no payments.

Some borrowers choose to make interest-only payments while in school. Paying $27 monthly on that $5,000 loan would prevent capitalization and save you from paying interest on interest later. Even irregular payments—$100 here, $50 there—reduce the amount that will capitalize.

During Deferment and Forbearance

Deferment and forbearance both pause your required payments, but they treat interest differently. During deferment on subsidized federal loans, the government covers your interest for certain qualifying reasons (unemployment, economic hardship, or returning to school). Unsubsidized federal loans and private loans continue accruing interest during all deferment periods.

Forbearance always allows interest to accrue on all loan types. A 12-month forbearance on $40,000 in loans at 7% interest adds $2,800 to your balance. When forbearance ends, that $2,800 typically capitalizes, increasing your principal to $42,800 and raising your monthly payment.

Why Student Loans Charge Interest

Lenders charge interest because they're providing capital today that you'll repay over a decade or more. That money has a cost: the lender could invest it elsewhere, and there's always risk you might not repay. Interest compensates for both the opportunity cost and the default risk.

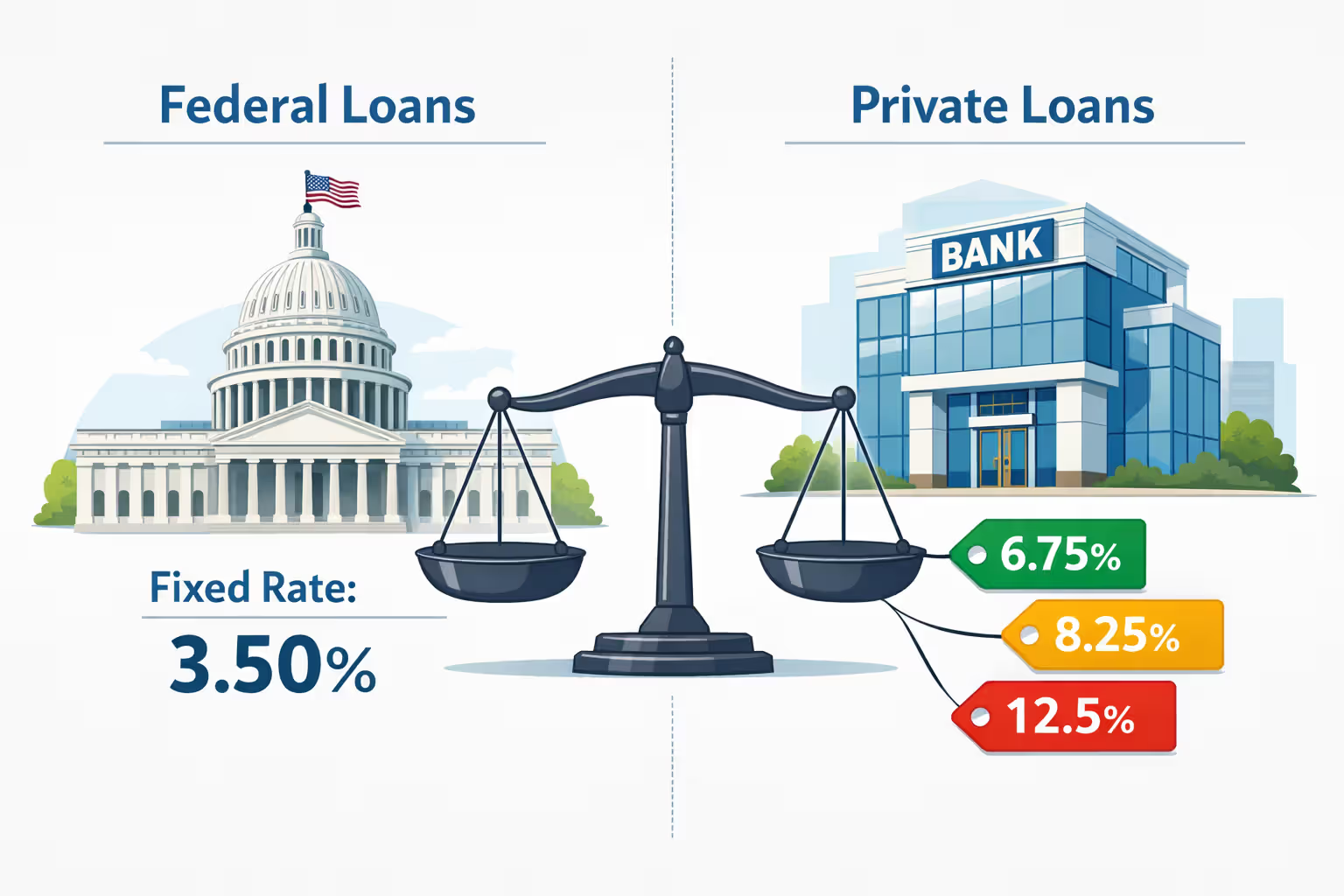

Federal student loans carry interest rates set by Congress, designed to cover the government's administrative costs and borrowing expenses while keeping rates affordable. The federal government borrows money through Treasury bonds and lends it to students at slightly higher rates. Federal loan interest rates don't vary based on your credit because the government's mission includes broad access to education funding.

Private student loans operate like other consumer credit products. Banks and credit unions charge interest rates that reflect their cost of capital plus a profit margin. They also price in your individual default risk. A borrower with excellent credit and a high-income cosigner poses less risk than someone with limited credit history and no cosigner, so they receive a lower rate.

Your credit score, income, debt-to-income ratio, and employment history all factor into private loan pricing. Two students borrowing the same amount for the same school might receive rate offers that differ by three or four percentage points based solely on their credit profiles.

Author: Danielle Pierce;

Source: sonicmusic.net

How Student Loan Interest Rates Are Determined

Federal student loan interest rates follow a formula established by Congress. Each spring, the government looks at the 10-year Treasury note auction in May and adds a fixed margin that varies by loan type. For the 2025-2026 academic year, Direct Subsidized and Unsubsidized Loans for undergraduates used the 10-year Treasury rate plus 2.05 percentage points. Graduate unsubsidized loans added 3.60 percentage points, and PLUS loans added 4.60 percentage points.

After your federal loan is disbursed, the interest rate never changes throughout repayment—regardless of market conditions or future legislation. A loan you receive in fall 2025 maintains that same percentage until your final payment, even if new borrowers two years later receive significantly different rates. Federal rates are capped by law: undergraduate loans can't exceed 8.25%, graduate loans max out at 9.5%, and PLUS loans cap at 10.5%.

Private lenders evaluate multiple factors when setting your rate. Credit scores carry the most weight—scores above 750 typically qualify for the best rates, while scores below 650 may not qualify at all without a creditworthy cosigner. Your loan term matters too: shorter repayment periods (5-7 years) usually come with lower rates than 15 or 20-year terms because the lender's money is at risk for less time.

Variable-rate private loans adjust based on financial benchmarks like SOFR (Secured Overnight Financing Rate) or Prime Rate, with the lender adding their margin on top. If you receive a rate structured as "SOFR plus 3.5%," your rate recalculates monthly or quarterly as the benchmark moves up or down. Fixed-rate loans maintain the same percentage from origination through final payment, providing predictable payments but typically starting 0.5-1.0 percentage points higher than their variable counterparts.

| Loan Category | 2025-2026 Rate | Fixed vs Variable |

| Direct Subsidized (Undergrad) | 6.53% | Fixed |

| Direct Unsubsidized (Undergrad) | 6.53% | Fixed |

| Direct Unsubsidized (Grad Student) | 8.08% | Fixed |

| Direct PLUS (Grad/Parent) | 9.08% | Fixed |

| Private (Excellent Credit Score) | 4.50% - 8.75% | Both Options Available |

| Private (Good Credit Score) | 7.25% - 12.50% | Both Options Available |

How Much Interest You'll Pay Over Time

Your total interest expense hinges on multiple factors: how much you borrowed initially, your loan's interest rate, your chosen repayment timeline, and whether you pay extra beyond required amounts. Federal loans typically use a 10-year standard repayment schedule, though income-driven alternatives can stretch repayment across 20 or 25 years, substantially multiplying your interest costs.

Consider a borrower with $30,000 in loans at 6.5% interest on a 10-year standard plan. Monthly payments of $340 will result in $10,796 in total interest—meaning the borrower pays $40,796 to retire a $30,000 debt. Extend that same loan to 20 years, and total interest jumps to $23,367, even though the monthly payment drops to $224.

The math gets more painful at higher balances. Someone with $100,000 in graduate school loans at 7.5% interest will pay $49,430 in interest over 10 years (monthly payment: $1,194). Switch to a 25-year repayment plan, and total interest balloons to $127,880 with a monthly payment of $759.

| Amount Borrowed | Annual Rate | Repayment Period | Monthly Payment Amount | Interest Over Loan Life |

| $30,000 | 6.5% | 10 years | $340 | $10,796 |

| $30,000 | 6.5% | 20 years | $224 | $23,367 |

| $50,000 | 7.0% | 10 years | $580 | $19,598 |

| $50,000 | 7.0% | 20 years | $388 | $43,146 |

| $100,000 | 7.5% | 10 years | $1,194 | $49,430 |

| $100,000 | 7.5% | 25 years | $759 | $127,880 |

Several factors push total interest costs higher. Capitalization events—when unpaid interest gets added to your principal—increase your balance and generate interest on interest. Periods of deferment or forbearance allow interest to accumulate without any payments reducing your balance. Income-driven repayment plans that set payments below the monthly interest charge create negative amortization, where your balance grows despite making payments.

Author: Danielle Pierce;

Source: sonicmusic.net

How to Reduce Student Loan Interest Costs

The most effective strategy is making payments while you're still in school. Even $25 or $50 monthly toward an unsubsidized loan prevents that interest from capitalizing when you enter repayment. A student who pays $50 monthly on a $5,000 loan during four years of school will save approximately $400 in capitalized interest.

Once in repayment, paying more than your minimum payment accelerates principal reduction. An extra $100 monthly on a $30,000 loan at 6.5% saves $3,089 in interest and cuts 2.5 years off your repayment term. Always specify that extra payments should apply to principal, not advance your due date.

Refinancing can lower your interest rate if you have strong credit and stable income. Private lenders offer refinancing rates as low as 4.5% for well-qualified borrowers in 2026. Refinancing $50,000 from 7% to 5% saves approximately $5,600 in interest over 10 years. The trade-off: refinancing federal loans into private loans eliminates federal protections like income-driven repayment, forbearance options, and potential forgiveness programs.

Nearly every lender provides a quarter-point rate discount (0.25%) when you set up automatic monthly withdrawals from your bank account. On a $40,000 loan, that small reduction saves about $1,000 over 10 years. Some employers provide student loan repayment assistance as a benefit—contributions up to $5,250 annually are tax-free through 2025, and this provision has been extended through 2026.

Income-driven repayment plans can reduce your monthly payment but usually increase total interest paid. These plans make sense when you need cash flow relief or you're pursuing Public Service Loan Forgiveness, which forgives remaining balances after 120 qualifying payments. Outside of forgiveness scenarios, the extended repayment period means more interest accumulation.

Most borrowers underestimate how much interest capitalization will cost them over 20 years of repayment. I've seen clients whose $60,000 in original loans grew to $75,000 before they made their first payment due to capitalized interest from school and a grace period. Every dollar you can pay toward interest before it capitalizes saves you three or four dollars over the life of the loan

— Rebecca Chen

Common Student Loan Interest Mistakes to Avoid

Many borrowers don't realize that unpaid interest capitalizes at specific trigger points: when your grace period ends, when you leave an income-driven repayment plan, when a deferment or forbearance period ends, or when you no longer qualify for a subsidized loan interest benefit. Each capitalization event permanently increases your principal and your monthly payment.

Making only minimum payments might feel manageable, but it maximizes your interest costs. A borrower who consistently pays an extra $75 monthly saves thousands in interest and shortens their repayment term significantly. The psychological relief of being debt-free years earlier often outweighs the modest monthly budget adjustment.

Author: Danielle Pierce;

Source: sonicmusic.net

Forbearance seems like an easy solution during financial difficulty, but it's expensive. Interest continues accruing on all loans, and that interest capitalizes when forbearance ends. Whenever possible, explore income-driven repayment plans instead—your payment might drop to $0 based on income, but you'll maintain progress toward forgiveness programs and avoid the interest capitalization that comes with forbearance.

Many borrowers with private loans accept the first offer they receive without shopping around. Interest rates can vary by two or three percentage points between lenders for the same borrower. Applying with three or four lenders takes a few hours but can save $10,000 or more over your repayment term. Rate shopping within a 30-day window typically counts as a single credit inquiry, minimizing the impact on your credit score.

FAQ

Student loan interest transforms a $40,000 education debt into a $60,000 repayment obligation if you're not strategic. The mechanics are straightforward—interest accrues daily on your principal balance—but the timing of when it starts, when it capitalizes, and how your repayment choices affect total costs require attention.

Focus on three priorities: prevent interest capitalization by making payments during school and deferment periods when possible, pay more than the minimum to accelerate principal reduction, and refinance if you can secure a meaningfully lower rate without sacrificing federal protections you need. Small decisions—a $50 monthly payment during college, an extra $75 toward principal each month, enrolling in autopay—compound into thousands of dollars saved over a decade of repayment.

The borrowers who pay the least interest are those who understand when interest starts accruing on their specific loan types, recognize capitalization triggers, and treat their loans as a priority expense rather than a minimum payment obligation. Your loan servicer won't remind you to make extra payments or warn you when interest is about to capitalize. That responsibility falls to you, and the financial benefit of getting it right is substantial.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.