Laptop showing financial charts on a wooden desk with dollar bills, graduation cap, notebook and pen — student loan payoff calculator concept

Student Loan Payoff Calculator Guide

Managing student debt can feel overwhelming when you're staring at a five- or six-figure balance. A student loan payoff calculator offers clarity by showing exactly when your loans will be paid off and how much interest you'll pay over time. These tools transform abstract numbers into concrete timelines, helping you make informed decisions about extra payments and repayment strategies.

Understanding how these calculators work—and how to use them correctly—can save you thousands of dollars in interest and shave years off your repayment timeline.

What Is a Student Loan Payoff Calculator

A student loan payoff calculator is a digital tool that estimates how long it will take to eliminate your student debt based on your current loan details and payment strategy. Unlike generic debt calculators, these tools account for the specific characteristics of student loans, including varying interest rates, grace periods, and repayment plan structures.

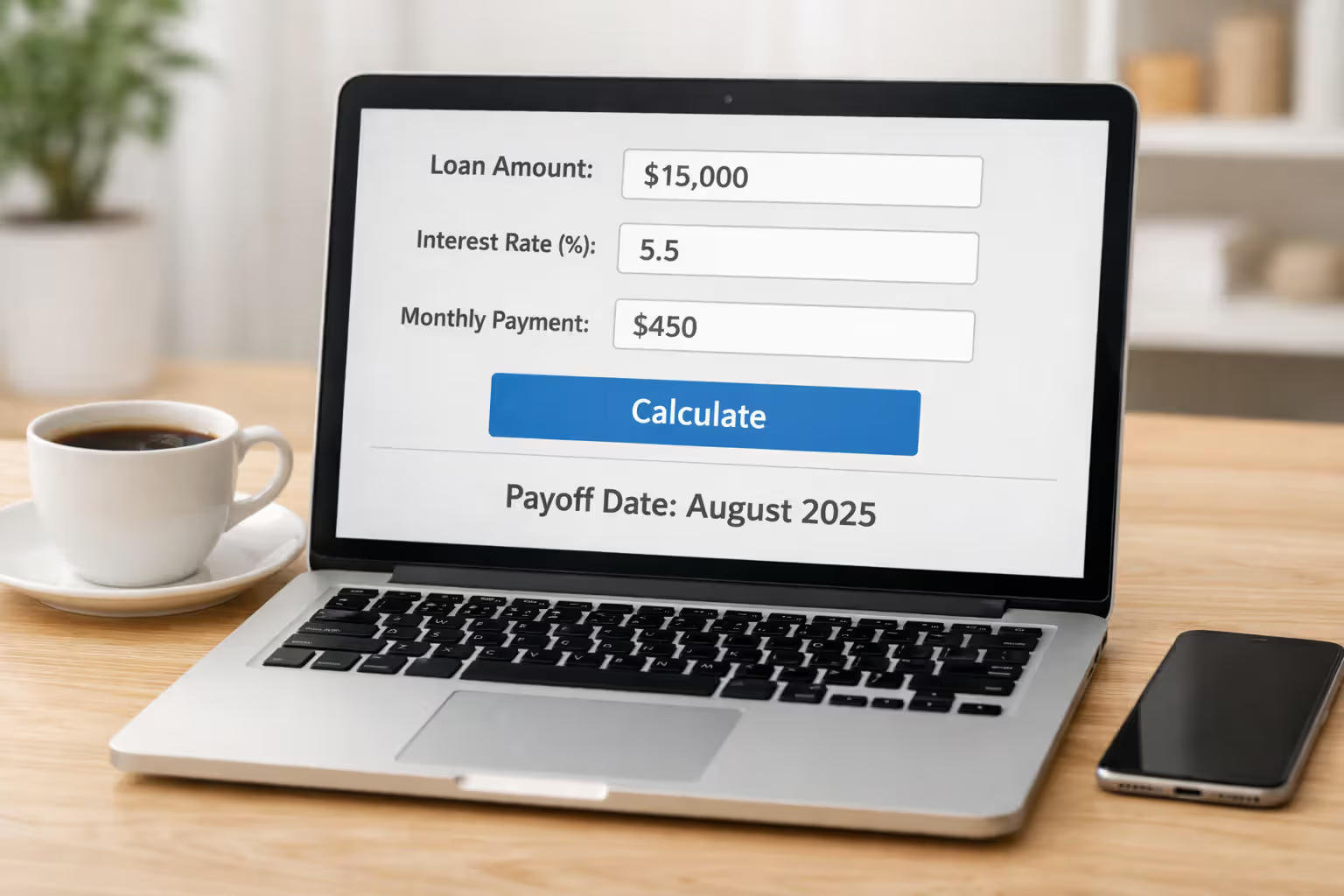

The pay off student loans calculator requires four essential inputs: your current loan balance, the annual interest rate, your monthly payment amount, and any additional payments you plan to make. Some advanced calculators also factor in whether your interest capitalizes (gets added to your principal balance) and how frequently your servicer compounds interest.

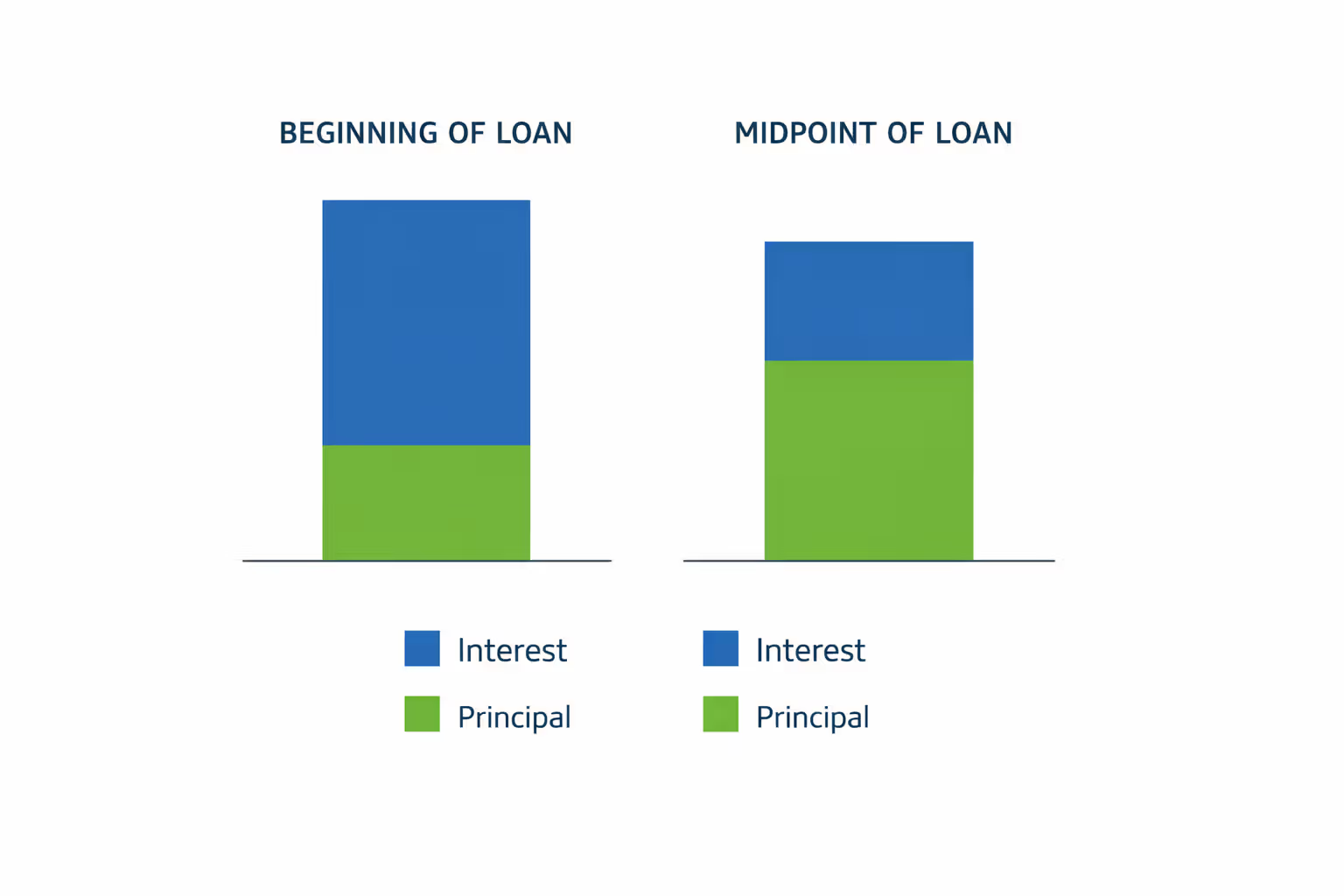

When you enter this information, the calculator generates a payoff date and shows your total interest cost over the life of the loan. Most tools also display an amortization schedule—a month-by-month breakdown showing how each payment splits between interest and principal. This visibility helps you understand why early payments have such a dramatic impact on your total cost.

The fundamental difference between a basic loan calculator and a student loan payoff calculator lies in the flexibility to model different repayment scenarios. You can instantly see what happens if you add $50 per month or make a one-time lump sum payment after receiving a tax refund.

How Student Loan Payoff Calculators Work

Behind the interface, a student loan repayment payoff calculator uses a standard amortization formula that accounts for compound interest. Each month, your servicer calculates interest on your outstanding balance, applies your payment to that interest first, then allocates the remainder to your principal.

Here's the calculation process broken down: Your servicer divides your annual interest rate by 12 to get a monthly rate. They multiply this monthly rate by your current principal balance to determine how much interest accrued that month. If your payment is $400 and $150 goes to interest, the remaining $250 reduces your principal balance.

This process repeats every month, but the ratio shifts over time. In the early years of a 10-year loan, you might pay $150 toward interest and $250 toward principal. Five years later, with a lower balance, you might pay $75 toward interest and $325 toward principal—even though your payment amount hasn't changed.

Author: Marcus Bennett;

Source: sonicmusic.net

The student loan payoff calculator explained in mathematical terms uses the formula: M = P[r(1+r)^n]/[(1+r)^n-1], where M is your monthly payment, P is the principal, r is your monthly interest rate, and n is the number of payments. You don't need to memorize this formula—the calculator handles it—but understanding that it exists helps you grasp why small rate differences or extra payments create such large impacts.

When you add extra payments, the calculator recalculates the entire amortization schedule. That additional $100 doesn't just reduce your balance by $100—it eliminates all the future interest that would have accrued on that $100 over the remaining loan term. For a loan with 15 years remaining at 6% interest, eliminating $100 of principal today saves you about $140 in total interest.

How to Use a Student Loan Payoff Calculator

Effective use of a student loan payoff calculator guide requires more than just plugging in numbers. The accuracy of your results depends entirely on the quality of your inputs and how you interpret the outputs.

Entering Your Loan Information

Start by logging into your loan servicer's website to get exact figures. Your current balance changes monthly as payments post and interest accrues, so using an estimate from memory will skew your results. Look for your "current principal balance" rather than your original loan amount.

For the interest rate, use the actual rate shown on your servicer's website, not a rounded number. The difference between 5.5% and 5.75% might seem trivial, but over 20 years on a $50,000 loan, it amounts to nearly $1,500 in additional interest.

If you have multiple loans at different rates, you'll need to decide whether to calculate them individually or combine them. Calculating separately provides more precision, especially if you're targeting high-rate loans first with extra payments. However, for a quick overall estimate, you can use a weighted average interest rate—just know this sacrifices some accuracy.

Your monthly payment should reflect what you actually pay, not what your servicer's minimum requires. If you're on an income-driven repayment plan paying $200 but the standard 10-year payment would be $350, enter $200 to see your current trajectory.

Author: Marcus Bennett;

Source: sonicmusic.net

Adding Extra Payments

The student loan extra payment calculator function is where these tools become powerful. You can model three types of extra payments: recurring monthly additions, periodic lump sums, or one-time payments.

For recurring extra payments, be realistic about sustainability. Adding $200 per month sounds great until an unexpected car repair derails your budget. A better approach: calculate what happens with an extra $50 or $100, then treat any amounts beyond that as bonuses that accelerate your timeline further.

Lump sum payments require strategic timing. If you receive a $3,000 tax refund, the calculator can show whether applying all of it to your highest-rate loan saves more than splitting it across multiple loans. Generally, concentrating extra payments on the highest-rate debt maximizes interest savings, but seeing the numbers makes the decision easier.

Some calculators let you specify whether extra payments apply to principal or the next scheduled payment. Always choose "principal only" if your servicer allows it. Applying extra money to future payments doesn't reduce your balance faster—it just pre-pays upcoming months while interest continues accruing on your full balance.

Interpreting Your Results

A student loan payoff estimate shows two critical numbers: your payoff date and total interest paid. Compare these figures to your current trajectory to quantify the impact of your strategy.

Look at the amortization schedule to identify inflection points. You'll notice that in the early years, your balance drops slowly despite making payments. This isn't an error—it's the reality of compound interest. Understanding this helps you avoid frustration and reinforces why starting extra payments early matters so much.

Pay attention to the "interest saved" figure when modeling extra payments. This number represents real money that stays in your pocket instead of going to your servicer. If adding $100 monthly saves you $8,000 in interest, you're effectively earning an 80% return on those extra payments—far better than most investments.

Author: Marcus Bennett;

Source: sonicmusic.net

Benefits of Using a Payoff Calculator

The primary advantage of a student loan early payoff calculator is visibility. Most borrowers know their monthly payment but have no idea when their loans will actually be gone or how much interest they'll pay. The calculator eliminates this uncertainty, transforming debt from an abstract burden into a solvable problem with a clear timeline.

Interest savings quantification is particularly valuable. When you see that an extra $75 per month saves you $6,200 in interest and eliminates your loans 3 years earlier, the trade-off becomes concrete. You can weigh that benefit against other uses for that $75—whether it's retirement savings, an emergency fund, or discretionary spending.

Testing scenarios without commitment lets you explore options risk-free. You might discover that aggressive payments for just two years, followed by minimum payments, achieves 80% of the benefit of aggressive payments for the entire loan term. This insight could inform a strategy where you focus intensely on debt while your expenses are low, then ease up when life gets more expensive.

Here's how different payment strategies compare for a $35,000 loan at 5.8% interest on a 10-year term:

| Monthly Payment Amount | Extra Payment | Time to Payoff | Total Interest Paid | Total Savings |

| $386 (minimum) | $0 | 10 years | $11,320 | $0 |

| $436 | $50 | 8.5 years | $9,180 | $2,140 |

| $486 | $100 | 7.4 years | $7,580 | $3,740 |

| $586 | $200 | 5.8 years | $5,460 | $5,860 |

The progression isn't linear—each additional dollar has slightly more impact than the last because it eliminates interest that would have compounded over more years.

Motivation and goal-setting become easier when you can visualize progress. Seeing that you'll be debt-free by your 35th birthday instead of your 40th birthday makes the sacrifice feel worthwhile. Many borrowers print their amortization schedule and cross off months as they pass, creating a tangible sense of progress.

A payoff calculator transforms student loans from an emotional burden into a math problem you can solve.When clients see the actual dollar-for-dollar impact of extra payments, they stop feeling helpless and start feeling empowered. That psychological shift is often more valuable than the interest savings

— Marcus Chen

Common Mistakes When Using Payoff Calculators

The most frequent error is calculating only one loan when you have multiple loans at different rates. Your total debt picture requires either separate calculations for each loan or a weighted average rate. Using the rate from your largest loan while ignoring three smaller loans at different rates produces meaningless results.

Ignoring loan servicer fees and prepayment penalties can skew your estimates, though most federal student loans don't have prepayment penalties. Some private loans do, or they may charge processing fees for extra payments. Check your loan agreement before assuming every extra dollar goes directly to principal.

Unrealistic extra payment amounts doom many repayment plans. Calculating that you'll add $400 monthly when your budget only has $150 of genuine flexibility sets you up for failure. Start conservative—you can always pay more, but falling short of an aggressive goal feels demoralizing.

Author: Marcus Bennett;

Source: sonicmusic.net

Forgetting tax implications of forgiveness programs is critical for those pursuing Public Service Loan Forgiveness or income-driven repayment forgiveness. If you're on track for forgiveness after 10 or 20 years, aggressively paying down your loans might actually cost you money. Run the numbers both ways: payoff calculator versus forgiveness estimator.

Another subtle mistake: not updating your calculations as circumstances change. Interest rates on variable-rate private loans can shift. Refinancing changes your rate and term. Income changes affect how much extra you can pay. Recalculate every 6-12 months to ensure your strategy still makes sense.

Payoff Calculator vs. Other Student Loan Tools

Student loan borrowers have access to several specialized calculators, each serving a different purpose. Understanding which tool answers which question prevents confusion and helps you make better decisions.

| Tool Type | Primary Use | Best For | Key Output |

| Payoff Calculator | Estimating payoff timeline with extra payments | Borrowers committed to aggressive repayment | Payoff date, interest savings from extra payments |

| Refinance Calculator | Comparing current loans to refinanced terms | Borrowers with good credit considering refinancing | New monthly payment, total interest comparison |

| Forgiveness Estimator | Calculating potential loan forgiveness | Public service workers or income-driven plan users | Forgiveness amount, required payment period |

| Repayment Plan Calculator | Comparing federal repayment plan options | Federal loan borrowers choosing a repayment plan | Monthly payment by plan, forgiveness eligibility |

A payoff calculator assumes you'll pay off your full balance and focuses on optimization through extra payments. A forgiveness estimator assumes you'll make minimum payments for 10-20 years and calculates what gets forgiven. These are fundamentally different strategies—use the tool that matches your actual plan.

Refinance calculators help you compare your current loan terms to potential new terms from private lenders. You might use both a refinance calculator and a payoff calculator together: first, determine if refinancing saves money, then use the payoff calculator with your new rate to plan extra payments.

Repayment plan calculators are specific to federal loans and help you choose between Standard, Graduated, Extended, and income-driven plans. Once you've selected a plan, you'd then use a payoff calculator to model what happens if you pay more than the minimum.

Frequently Asked Questions About Student Loan Payoff Calculators

A student loan payoff calculator transforms your debt from an intimidating obligation into a manageable challenge with a clear solution. By showing exactly how your payments break down between interest and principal, these tools reveal why early action matters so much and quantify the real-world impact of different repayment strategies.

The most valuable insight these calculators provide isn't just your payoff date—it's the understanding that you have control over your debt timeline. Whether you can add $25 per month or $250, the calculator shows that progress is possible and helps you find the sustainable strategy that fits your budget.

Start by gathering your current loan details and running your baseline scenario with minimum payments. Then experiment with realistic extra payment amounts to find the sweet spot between aggressive repayment and maintaining financial flexibility for other goals. Revisit your calculations every six months as your income, expenses, and priorities evolve.

Your student loans won't disappear overnight, but with the right tools and strategy, you can see the finish line and chart the most efficient path to reach it.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.