Young person sitting at a home desk reviewing student loan documents on a laptop with a hopeful expression

Fresh Start Program Student Loans Guide

If you've watched your credit score plummet because of defaulted federal student loans, you're not alone—and you might qualify for a limited-time fix. The Department of Education launched what they call the Fresh Start Program back in spring 2022, right as the pandemic payment freeze was winding down. This wasn't just another government announcement that changes nothing. For roughly 7.5 million Americans stuck in default, it meant real consequences disappearing overnight: no more wage garnishments, restored credit reports, and a legitimate shot at loan forgiveness programs that were previously off-limits.

Here's what makes this different from the usual default resolution options: you didn't have to jump through months of hoops to see results. But there's a catch (there's always a catch). Fresh Start had deadlines. Miss them, and you're back to the old, harder methods of escaping default—methods that take longer and do more lasting damage to your finances.

So what exactly did this program offer, who got to use it, and what happens now that enrollment has closed?

What Is the Fresh Start Program for Student Loans?

Think of the fresh start program student loans as a one-time reset button for people whose federal loans went into default before COVID hit. The Department of Education runs it through their Federal Student Aid office—the same folks who process your FAFSA each year.

Default typically kicks in once you've skipped payments for 270 days (about nine months). When that happens, the government can garnish up to 15% of your paycheck, grab your tax refunds, and even take a cut of your Social Security benefits. Your credit score drops anywhere from 50 to 100 points. You can't get more federal financial aid. You're locked out of income-based repayment plans and loan forgiveness programs.

Fresh Start hit the pause button on all of that. The program opened in April 2022 and allowed enrollment through late September 2025. If you had defaulted loans when the pandemic payment pause started in March 2020, you qualified for automatic temporary relief—but you had to enroll and complete follow-up steps to make those benefits stick beyond September 2026.

The Fresh Start program gives borrowers who've experienced default a true second chance—not just to avoid collections, but to access income-driven repayment plans and pursue loan forgiveness that can change the trajectory of their financial lives

— James Kvaal

What separates the fresh start initiative student loans from standard default fixes? Speed and simplicity. Loan rehabilitation takes nine months. Consolidation leaves default marks on your credit for seven years. Fresh Start required just three payments and wiped your record clean—if you acted before the window closed.

Who Qualifies for Student Loan Fresh Start?

Not everyone with defaulted student debt could use this program. The Department of Education drew a specific line in the sand: your loans had to be in default status on March 13, 2020 (when pandemic protections began), and they needed to still be in default when Fresh Start launched in spring 2022.

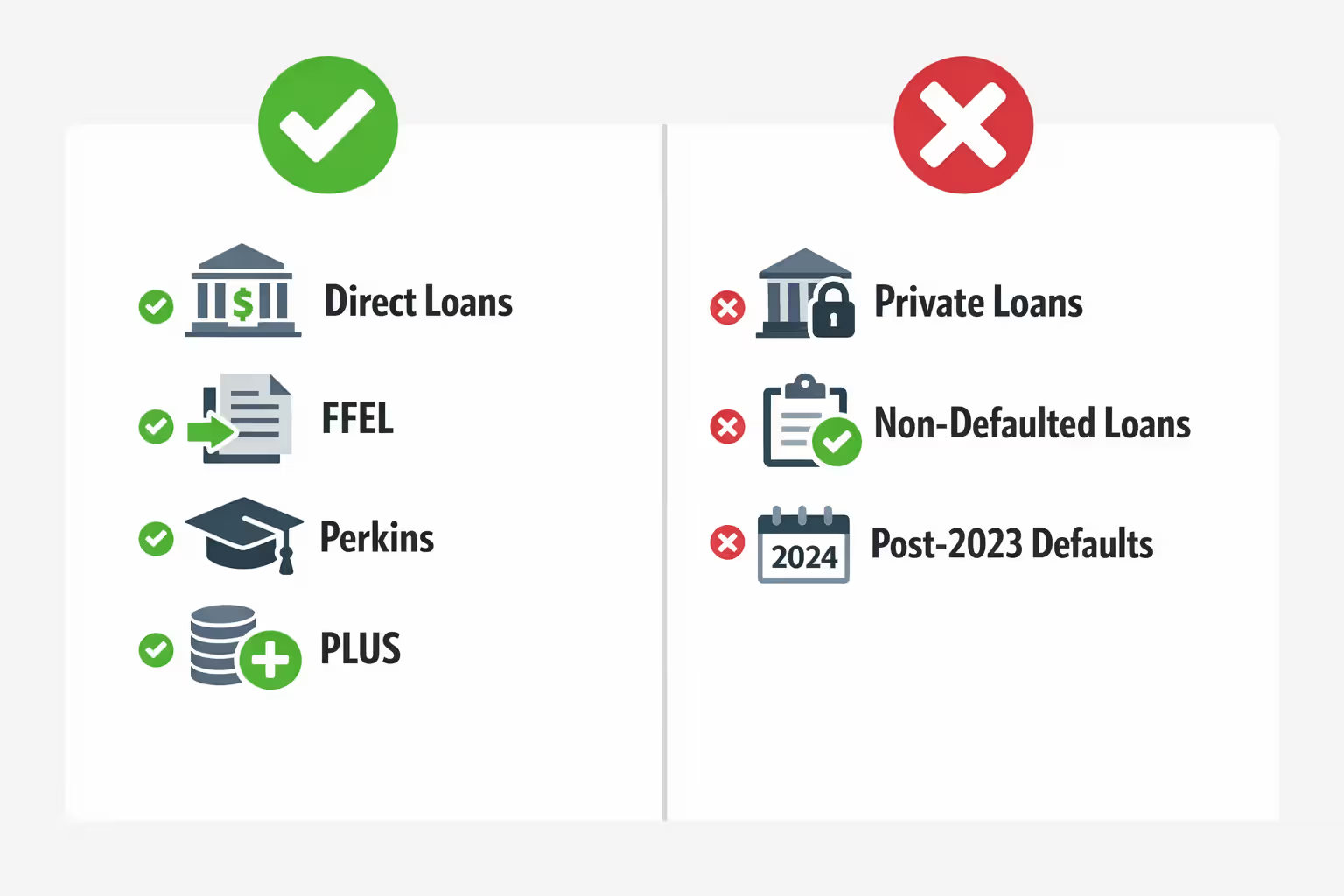

Here's what qualified:

- Direct Loans (the subsidized and unsubsidized loans most students take out)

- FFEL Program loans (older loans from the Federal Family Education Loan program)

- Federal Perkins Loans that the Department of Education holds

- PLUS loans (whether you're a parent who borrowed for your kid or a grad student)

Here's what didn't:

- Private student loans from Wells Fargo, Sallie Mae, or any bank

- Federal loans that never went into default in the first place

- Loans you defaulted on after the pandemic payment pause ended in October 2023

- HEAL program loans (a defunct federal health professions program)

- State loan programs

One question that came up constantly: do Parent PLUS loans count? Yes—if you borrowed a PLUS loan for your child's education and it was in default during the qualifying window, you got the same benefits as student borrowers.

The timing matters here. Someone who defaulted in 2019? Qualified. Defaulted in 2024? Out of luck for Fresh Start, though rehabilitation and consolidation still work.

Author: Danielle Pierce;

Source: sonicmusic.net

How to Enroll in the Fresh Start Initiative Student Loans

The enrollment process confused a lot of people because some benefits happened automatically while others required you to pick up the phone and make things official.

Automatic vs. Manual Enrollment

When the Department of Education rolled out Fresh Start, they automatically gave certain protections to everyone who qualified:

- Collections stopped (no more garnishments or tax offsets)

- Default removed from your credit report (temporarily)

- Federal financial aid eligibility restored

- Access reopened to income-driven repayment options

Sounds great, right? Except these automatic protections expire in September 2026 unless you actively enrolled in the program. That meant calling your loan servicer and taking specific steps.

The enrollment process looked like this:

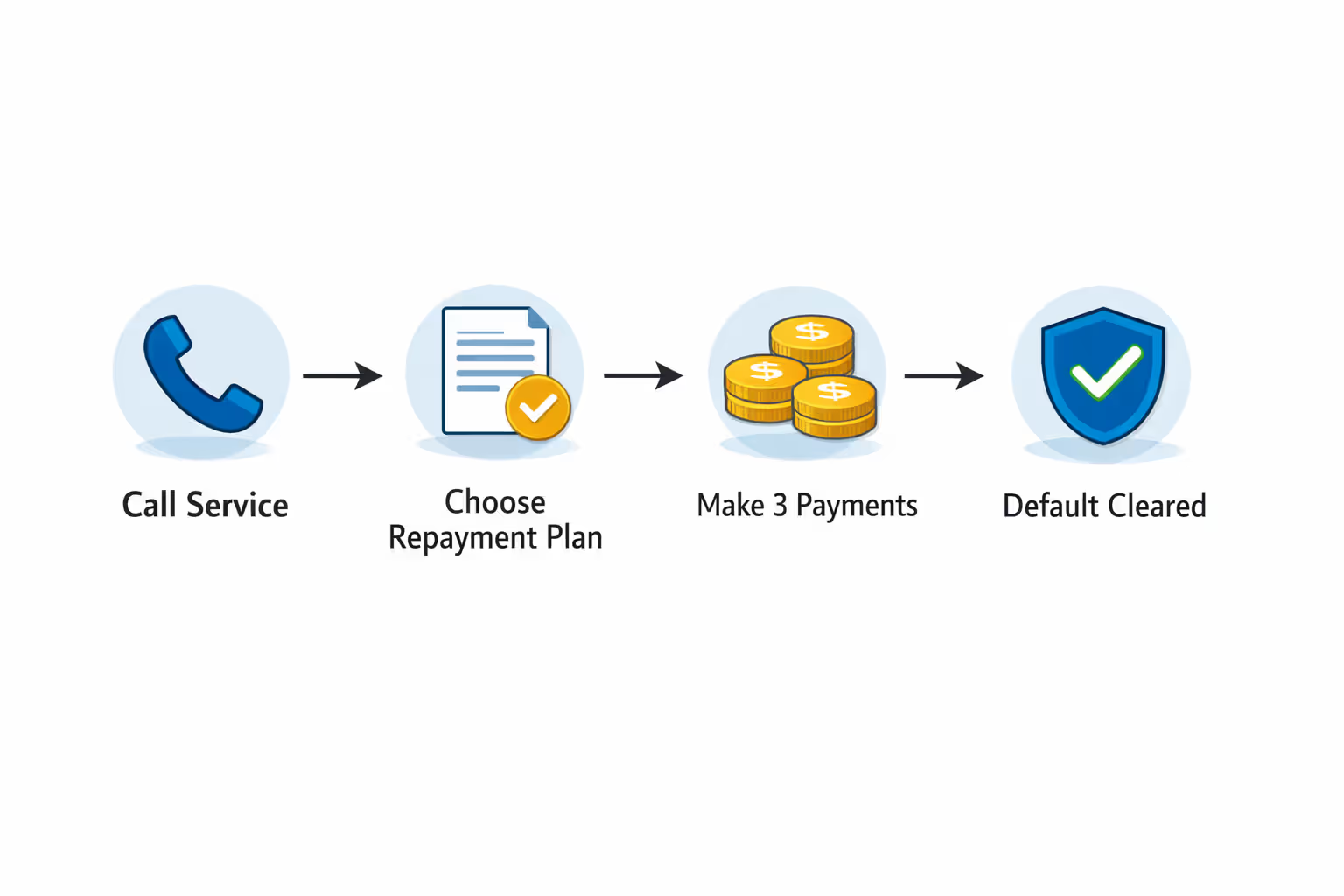

- Figure out who services your defaulted loans. Log into StudentAid.gov and check your loan details. Defaulted loans usually sit with something called the Default Resolution Group or with collection agencies the Department contracts with.

- Call them and say the magic words. Tell them explicitly: "I want to enroll in the Fresh Start program." Don't assume they'll offer it. Get a confirmation number or email proving you enrolled.

- Pick a repayment plan that makes sense. Most people chose income-driven plans (SAVE, IBR, PAYE, or ICR) because the payment amount ties to what you actually earn. If your income is low enough, your required payment might be zero dollars.

- Submit your paperwork. Income-driven plans need proof of income. Go to StudentAid.gov, fill out the IDR application, and upload your recent tax return or pay stubs.

- Make three payments within 10 months. This is the make-or-break requirement. Three consecutive payments—even if those payments are $0 under an income-driven plan—permanently remove your default status.

The deadline to start this process was September 30, 2025. If you missed it, your automatic protections vanish in September 2026, and you're back to square one with default consequences.

What Happens After You Enroll

Once you enrolled in student loan fresh start, your account moved through a multi-step process that took a few months to complete.

Within the first 30-90 days: Your loans transferred from the collection agency back to a regular federal loan servicer. During this limbo period, you won't get bills. It's easy to think nothing's happening, but the transfer is processing. Check StudentAid.gov weekly to see when the transfer completes.

After the transfer finishes: Your new servicer sends you a welcome packet showing your repayment plan and monthly payment amount (which might be $0 if you're on an income-driven plan based on low income).

Once you've made three payments: Your default status disappears permanently. The credit bureaus remove the default notation within 60-90 days. Your loans show as "in repayment" instead of "in default."

Going forward: You've got full access to federal student loan benefits again—deferment if you go back to school, forbearance during financial hardship, and eligibility for Public Service Loan Forgiveness if you work for a qualifying employer.

Here's where people screwed up: they thought enrolling alone fixed everything. It didn't. You had to complete those three payments. Skip that step, and when September 2026 rolls around, you'll slide right back into default with all the wage garnishments and credit damage that come with it.

Author: Danielle Pierce;

Source: sonicmusic.net

Benefits of the Fresh Start Student Loans Program

The fresh start student loans program delivered advantages that went way beyond just stopping collection agencies from calling you.

Your credit report gets fixed: Default marks typically stick around for seven years from the date you defaulted. That's seven years of getting denied for mortgages, car loans, and even some jobs. With Fresh Start, once you complete the three-payment requirement, the default notation vanishes completely—not just marked "satisfied" or "paid," but actually deleted. Your score can jump 50-100 points overnight.

You can go back to school: Students with defaulted loans can't receive Pell Grants, work-study, or any new federal loans. Parents with defaulted PLUS loans can't borrow for their kids' college expenses. Fresh Start flipped that switch back on immediately, before you even made the three payments. If you or your child needed to return to school, this benefit alone could be worth tens of thousands of dollars.

Income-driven plans become available again: Before Fresh Start, you had to fully rehabilitate your defaulted loans before you could access income-based repayment options. That meant nine months of payments before you could even apply for a plan that bases your bill on what you earn. The fresh start program student loans explained in simple terms gave you immediate access to these plans, which can legally reduce your monthly payment to zero dollars if your income falls below certain thresholds.

Forgiveness programs reopen: Default disqualified you from every federal forgiveness program. With Fresh Start, you could suddenly pursue:

- Public Service Loan Forgiveness (PSLF) if you work for government or qualifying nonprofits—forgiveness after 120 payments

- Income-driven plan forgiveness after 20-25 years of payments (with any remaining balance forgiven)

- Borrower Defense to Repayment if your school lied to you or broke laws

- Total and Permanent Disability discharge if you have qualifying medical documentation

Collections stop immediately: The government can garnish up to 15% of your take-home pay. They can seize your entire tax refund. They can take up to 15% of your Social Security benefits. All of that stops the moment you enroll in fresh start for student loans. For someone earning $40,000 who was losing $400+ a month to garnishment, that's immediate breathing room.

Author: Danielle Pierce;

Source: sonicmusic.net

Collection costs disappear: When loans go into default, collection agencies tack on fees up to 16% of your balance. On a $30,000 loan, that's $4,800 in extra costs. Fresh Start enrollment waived these fees entirely—money you'd never have to pay back.

The trade-off? This opportunity had an expiration date. People who waited too long lost access to the easiest path out of default that's ever existed.

Fresh Start Program vs. Loan Rehabilitation vs. Consolidation

When your federal student loans fall into default, you've got three main escape routes. They work differently, take different amounts of time, and leave your credit in different states.

| What You're Comparing | Fresh Start Program | Loan Rehabilitation | Direct Consolidation |

| Who Can Use It | Only loans that defaulted before March 2020 | Any federal loan currently in default | Any federal loan currently in default |

| How Long It Takes | Three payments spread across 10 months | Nine monthly payments over 10 months | One application; takes 60-90 days to finalize |

| What Happens to Your Credit | Default notation completely erased | Default notation completely erased | Default stays on your report but shows as "paid"; remains visible seven years |

| Extra Fees You Pay | None; waives collection costs | None; waives collection costs | Collection costs get added to your new loan balance |

| When Financial Aid Reopens | Right away, before you finish payments | Only after you complete all nine payments | Right after consolidation processes |

| Best Match For | Anyone who defaulted before pandemic and enrolled before Sept 2025 | People who missed Fresh Start but want their credit cleaned up | People who need immediate default resolution or want to start PSLF quickly |

What made Fresh Start better: Speed. Clean credit in 10 months or less. Zero fees. Instant federal aid eligibility.

What limited Fresh Start: It only worked if you defaulted before March 2020. You had to enroll by September 2025. You still had to make those three payments or nothing became permanent.

Why rehabilitation still matters: Available anytime. Completely removes default from your credit just like Fresh Start did. The catch? It takes nine full months and you can only use it once per loan. Default again, and rehabilitation isn't an option anymore.

Why you might choose consolidation instead: It's fast—the only option that resolves default in under three months. You can consolidate multiple times (unlike rehabilitation's one-time limit). If you need to start making qualifying PSLF payments immediately, consolidation gets you there.

Consolidation's downside: That default stays on your credit report until the seven-year mark hits. Collection costs don't disappear; they get rolled into your new consolidated loan balance. If you'd made progress toward PSLF, consolidation used to reset your count to zero (though recent policy changes preserved some IDR payment counts).

The student loan fresh start program offered the cleanest exit from default for anyone who qualified. But if you defaulted after the pandemic pause or missed the enrollment window, rehabilitation gives you the next-best outcome for credit repair. Consolidation works when speed trumps everything else—like when you're racing to get into PSLF before changing jobs.

Common Mistakes to Avoid with Student Loan Fresh Start

Even with a program designed to be simple, borrowers found ways to shoot themselves in the foot.

Blowing past the deadline: September 30, 2025 wasn't a suggestion. The Department of Education didn't extend it (unlike other deadlines they've pushed back multiple times). People who thought "I'll do it next month" past that date lost their shot at the easiest default resolution option available.

Taking someone's word for it on the phone: Call center workers at loan servicers make mistakes. They're overworked and undertrained. If you called to enroll but didn't get written confirmation—an email, a letter, a confirmation number you can reference—you might not actually be enrolled. Always document everything. Screenshot your StudentAid.gov account. Save emails. Take notes with dates and names during phone calls.

Thinking Fresh Start meant loan forgiveness: Fresh Start removed default status. It didn't forgive a single dollar of principal or interest. Some borrowers stopped engaging entirely because they thought "Fresh Start" meant their loans were gone. Then collections started up again after September 2026, and they were blindsided.

Losing track during servicer transfers: When your loans moved from a collection agency back to a regular servicer, communication fell through the cracks. Borrowers who didn't proactively check their StudentAid.gov dashboard sometimes missed the first bill from their new servicer. Then they didn't make those critical three payments because they literally didn't know who to pay.

Stopping at two payments: The three-payment rule wasn't negotiable. Two payments did nothing. Your third payment had to post within 10 months of your first payment. If you were on an income-driven plan with a $0 monthly payment, you still had to submit documentation three times confirming your enrollment and income level. Those counted as your "$0 payments."

Forgetting to update your address and contact info: You moved apartments. Changed your phone number. Started using a different email. If your servicer couldn't reach you with important notices about payment deadlines or plan recertification, you missed critical steps that could tank your Fresh Start benefits.

Picking a payment plan you couldn't afford: Some people chose the standard 10-year repayment plan—often $300-500 monthly—when they qualified for income-driven plans that would've cost them zero or close to it. Before selecting any plan, spend 10 minutes with the Loan Simulator tool at StudentAid.gov. It shows exactly what you'd pay under each plan based on your actual income and family size.

Mixing up different relief programs: Fresh Start, the SAVE plan, the one-time IDR account adjustment, and various loan forgiveness initiatives all launched around the same timeframe. They're separate programs. Qualifying for one didn't automatically enroll you in the others. You had to research and apply for each one individually.

Author: Danielle Pierce;

Source: sonicmusic.net

Frequently Asked Questions About Fresh Start for Student Loans

The Fresh Start Program gave defaulted borrowers something federal student loan programs rarely offer: a clean slate without years of consequences. For the 7.5 million people stuck in default when COVID hit, this represented the fastest, simplest path to restored credit and renewed access to federal benefits that's ever existed.

But it had an expiration date. Enrollment closed in late September 2025. If you got in before that deadline, your job now is finishing those three payments. Set up autopay if your servicer offers it. Mark your calendar. Check StudentAid.gov monthly to confirm each payment posted correctly. Missing this final step wastes everything you've already accomplished.

If you missed the enrollment window entirely, you're not out of options—just out of easy options. Rehabilitation still removes default from your credit but takes nine months of payments. Consolidation resolves default quickly but leaves the mark on your credit report for seven years. Both reopen access to income-driven repayment and forgiveness programs. They're harder than Fresh Start was, but they work.

The bigger lesson here? Federal student loan relief programs come with strict deadlines and specific requirements. Whether it's Fresh Start, Public Service Loan Forgiveness, income-driven forgiveness, or whatever program launches next, success requires paying attention and following through. Default doesn't have to define your financial life forever, but getting out of it means taking action when opportunities appear—not six months after the deadline passes.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.