Stressed young person sitting at desk with laptop and bills, worried about student loan payments

Student Loan Forbearance Guide

Content

Content

Can't afford your student loan payment this month? You're looking at three choices: let the loan go delinquent (bad idea), scramble to find the money somewhere (maybe not possible), or contact your servicer about forbearance.

Here's what most borrowers don't realize until it's too late: forbearance stops the bleeding now but costs you later. That $400 monthly payment you're skipping? The interest behind it—roughly $200 to $300 depending on your balance—keeps stacking up anyway. After six months of forbearance, you might owe $1,500 more than when you started, even though you haven't made a single payment.

So when does forbearance actually make sense? And when are you just making your problem bigger? Let's break down exactly how this works.

What Is Student Loan Forbearance?

Think of forbearance as hitting the pause button on your loan payments—but the interest meter keeps running.

Your servicer agrees to stop requiring monthly payments for a specific time period. Could be three months, could be a year, depending on your situation and what type you qualify for. During that window, you won't get hit with late fees or delinquency marks. Your loan stays current in the system.

The catch? Interest builds up on everything. Subsidized loans, unsubsidized loans, PLUS loans, private loans—doesn't matter. The interest clock never stops during forbearance.

Federal loans split forbearance into two buckets: general and mandatory. General forbearance is up to your servicer's discretion. You ask, they decide. Mandatory forbearance means your servicer has to approve it if you meet certain requirements (we'll get into those specifics shortly).

Private loans are the Wild West. One lender might give you 12 months maximum over your entire loan life. Another might be more generous. There's no federal regulation requiring private lenders to offer forbearance at all, though most do something.

Here's a key distinction: forbearance versus just... not paying. If you ghost your servicer and stop making payments, you'll rack up late fees immediately. After 90 days, you're officially delinquent. At 270 days on federal loans, you're in default—which means wage garnishment, tax refund seizures, and credit damage that lasts seven years.

Forbearance keeps you out of that nightmare. It's a formal agreement. Your account status shows current, not delinquent.

Who can get it? For federal loans, pretty much anyone can request general forbearance. Whether you get approved depends on your explanation and your servicer's policies. Mandatory forbearance has hard eligibility rules—medical residents, AmeriCorps volunteers, National Guard members on active duty, and people whose monthly debt payments exceed 20% of gross income all qualify automatically with the right documentation.

Private lenders set their own rules. Some want proof of job loss or medical emergency. Others approve forbearance requests more casually. Check what you signed originally or call your lender.

How Student Loan Forbearance Works

Step one: call your servicer before you miss a payment. Seriously. Don't wait until you're already 30 days late.

You'll fill out paperwork—usually available online through your account dashboard. For general forbearance on federal loans, you're basically writing a short explanation: "I lost my job," "Medical bills wiped out my savings," "My hours got cut and I can't cover rent plus loans." For mandatory forbearance, you'll need backup documents. Pay stubs proving your debt-to-income ratio. A letter from your residency program. Your AmeriCorps enrollment confirmation.

Most servicers process requests within a week or so. Sometimes two weeks if they're backed up. Once approved, your first forbearance period usually runs three months. You can extend it, typically up to 12 months at a time. There's a lifetime cap on general forbearance of three years total.

What actually happens during those three months? Your required payment drops to zero. No bills, no autopay deductions. But every single day, interest accrues based on your principal balance.

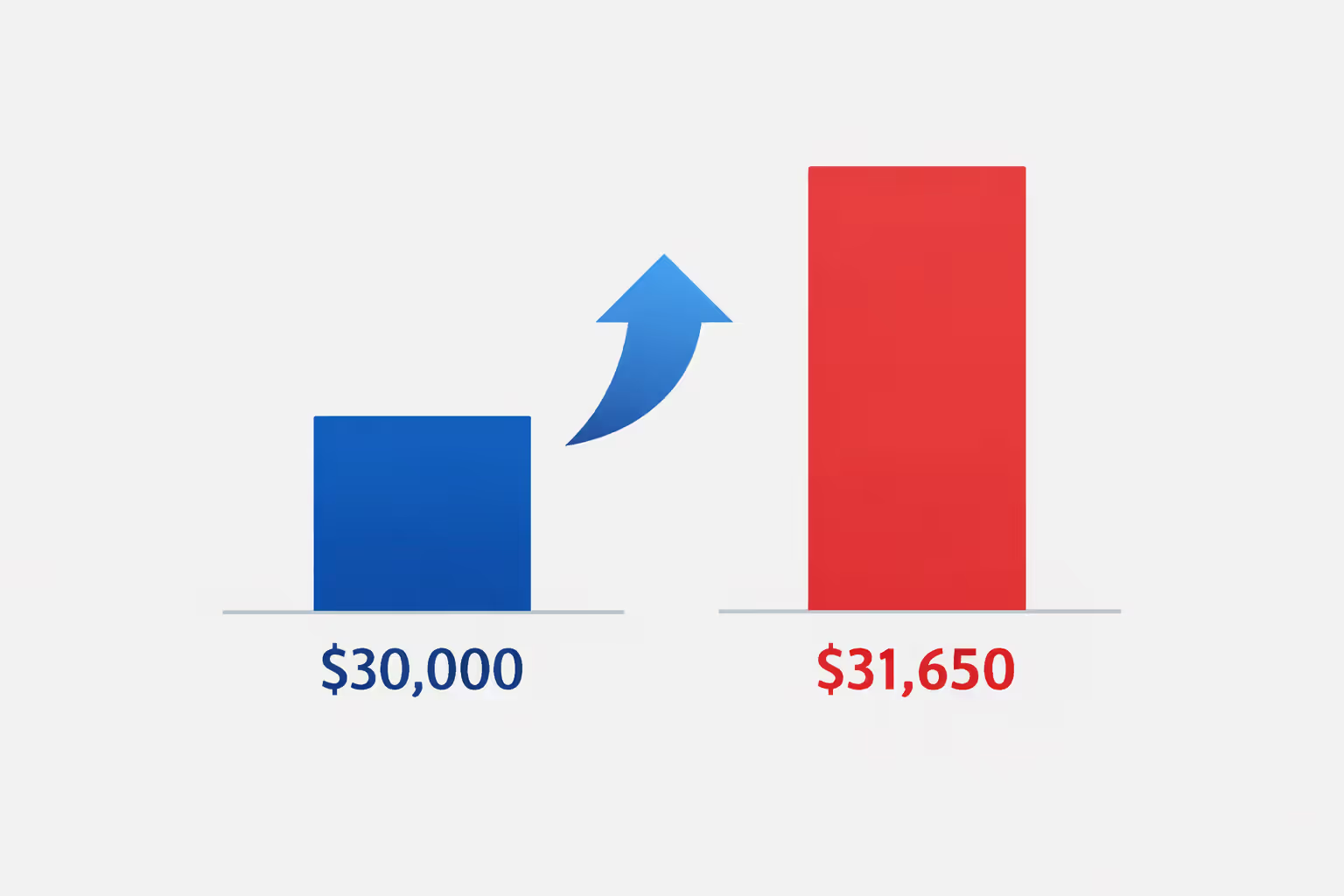

Let's do the math on a real example. Say you've got $30,000 in loans at 5.5% interest. That's about $4.50 in interest per day. Over a month, roughly $137. Over a year of forbearance, $1,650.

Now here's where it gets expensive. When forbearance ends, that $1,650 doesn't just sit there as a separate amount you owe. It capitalizes—meaning it gets added to your principal. Your new balance is $31,650. And from that point forward, you're paying interest on the new, higher amount.

Run that scenario out over a 10-year repayment term, and that one year of forbearance will cost you an extra $1,000+ in total interest by the time you pay off the loan.

You can dodge this by making payments during forbearance. Nobody requires it, but nothing stops you either. Even if you can't swing the full $400 you used to pay, throwing $137 per month at the interest prevents your balance from growing. The principal stays level.

Author: Danielle Pierce;

Source: sonicmusic.net

Types of Student Loan Forbearance

General Forbearance

This is the "my servicer might say yes, might say no" version. Available on Direct Loans and FFEL program loans when you're dealing with financial struggles, medical costs, or employment changes.

You don't have to prove anything with documents, though explaining your situation clearly helps. "I'm between jobs," "I had emergency surgery and the bills are crushing me," "My spouse lost their income and we're struggling"—these all work as explanations.

Your servicer has full discretion. They can approve or deny based on your request. Most approve these pretty routinely for first-time requests.

Grants typically come in three to six-month chunks. You can keep renewing until you hit the three-year lifetime maximum.

Best use case: short-term problems with a light at the end of the tunnel. You got laid off but you're actively interviewing and expect to land something within a few months. You're recovering from an accident and will be back at work by summer. Forbearance gets you through the rough patch.

Mandatory Forbearance

Your servicer must approve these if you qualify and submit proper documentation. No discretion involved.

Here's what triggers mandatory forbearance:

- Medical or dental residency/internship: Up to three years. Given how common six-figure med school debt is, and how residents typically earn $55,000 to $65,000, this forbearance type gets used constantly. On a $250,000 loan balance, though, three years of interest means $40,000+ in additional debt.

- AmeriCorps service: Covers your entire service period. AmeriCorps does provide education awards that can offset this, but interest still accrues during service.

- National Guard active duty: Available while you're deployed or on qualifying active duty.

- Teacher Loan Forgiveness qualification: If you're working toward Teacher Loan Forgiveness but haven't completed the required five years yet.

- Monthly payments exceed 20% of gross income: Renewable in 12-month periods. This one requires math. Take your gross monthly income—that's before taxes. Multiply by 0.20. If your total monthly student loan payment is higher than that result, you qualify. Example: You make $3,200 per month gross, and your combined student loan bills total $700. That's 21.9% of your income, so you're eligible.

The income-based mandatory forbearance needs documentation: recent pay stubs or tax returns showing your income, plus a statement from your servicer listing your monthly payment amounts.

Forbearance vs Deferment for Student Loans

People mix these up constantly. Both pause your payments. The difference is what happens to your interest—and that difference costs real money.

| Feature | Forbearance | Deferment |

| Interest on subsidized federal loans | Keeps accruing—you pay it | Doesn't accrue during certain deferment types—government covers it |

| Interest on unsubsidized federal loans | Accrues on everything | Still accrues, but won't capitalize right away |

| Who qualifies | Financial hardship (general type) or specific situations like residency (mandatory type) | Currently enrolled at least half-time, unemployed and job hunting, receiving specific federal benefits, active military duty, cancer treatment |

| How long it lasts | Up to 3 years total for general forbearance; varies for mandatory types | Up to 3 years for unemployment/economic hardship; unlimited while enrolled in school |

| How hard to get approved | General forbearance is fairly easy; mandatory requires specific documentation | Need to prove enrollment, unemployment status, or benefit receipt—more paperwork |

| Effect on forgiveness programs | Months don't count toward PSLF or IDR forgiveness timelines | Most deferment periods don't count either, except military/Peace Corps/AmeriCorps service |

Deferment wins almost every time if you qualify. The in-school deferment happens automatically when you're enrolled at least half-time—your school reports enrollment to the National Student Loan Data System and your loans automatically defer. During that period, subsidized loans don't accrue any interest.

Economic hardship deferment requires you to receive means-tested benefits (SNAP, TANF, SSI, etc.) or prove your income falls below 150% of the federal poverty line for your household size. For a single person in 2026, that's approximately $22,500 per year. You can get up to three years total of this type, granted in one-year increments.

Unemployment deferment works if you're getting unemployment benefits or can demonstrate you're actively job-hunting. Also capped at three years total, approved in six-month periods.

Bottom line: try for deferment first. If you don't meet those stricter requirements, forbearance is your backup option.

When to Use Student Loan Forbearance

Forbearance works well for specific, time-limited emergencies.

Good reasons to use forbearance:

- You just lost your job but have solid prospects: Got laid off, but you're already interviewing and expect an offer within two months. Forbearance covers the gap without trashing your credit or triggering collection calls.

- Medical emergency hit your finances: Your kid needed emergency surgery. You're dealing with $8,000 in medical bills even after insurance. Forbearance frees up cash flow for three to six months while you arrange hospital payment plans.

- Natural disaster recovery: Hurricane damaged your home. You're juggling insurance claims, temporary housing costs, and repairs. Forbearance gives you breathing room during crisis mode.

- Waiting for IDR approval: You applied for an income-driven repayment plan but processing takes six weeks. Rather than miss payments during the application window, forbearance keeps you current.

Bad reasons to use forbearance:

- You've been unemployed for eight months with no job prospects: Forbearance won't fix this. You need unemployment deferment or an income-driven plan with a $0 payment—both of which are available and better suited to long-term unemployment.

- Your income never covers all your bills: If you're chronically short every month, forbearance is a band-aid on a bullet wound. You need a structural fix: income-driven repayment that sets payments based on what you actually earn, not what the Standard Plan thinks you should pay.

- You're trying to avoid dealing with your loans: Some borrowers use forbearance for a year, then another year, then another. Meanwhile interest compounds and the problem gets worse. Three years later they owe $12,000 more than they started with.

- You qualify for a $0 income-driven payment: If your income is low enough that SAVE or another IDR plan would set your payment at zero, choose that instead. Those $0 payments count toward your 20-year forgiveness clock. Forbearance months don't count toward anything.

Rule of thumb: use forbearance when you can point to a calendar date when your situation improves. "I'll have a new job by March" or "I'll finish physical therapy and return to work in 10 weeks" = good forbearance candidate. "I have no idea when I'll be able to afford these payments" = you need a different solution.

Author: Danielle Pierce;

Source: sonicmusic.net

Downsides and Risks of Forbearance

Interest accumulation isn't theoretical. It's the actual cost of forbearance, measured in dollars you'll pay later.

Take someone with $50,000 in unsubsidized loans at 6%. Over 12 months of forbearance, about $3,000 in interest piles up. When forbearance ends, that $3,000 capitalizes. New balance: $53,000. Over a standard 10-year repayment, that capitalized interest adds roughly $2,000 to the total amount you'll pay.

Scale it up to medical or law school debt levels. $200,000 at 7% interest. One year of forbearance accrues $14,000 in interest. Capitalize that, and you're now paying interest on $214,000. By the time you finish repayment 10 years later, that single year of forbearance cost you over $9,000 extra.

Most borrowers see forbearance as free money—like the payments just disappear.Then they get the first bill after forbearance ends and the balance is $18,000 higher than they remember. That's when they realize those skipped payments weren't free at all

— Marcus Chen

How forbearance affects forgiveness programs:

Pursuing Public Service Loan Forgiveness? You need 120 qualifying payments while working for a qualifying employer. Forbearance months don't count. Put your loans in forbearance for a year, and you've just added 12 months to your PSLF timeline. Instead of finishing in 10 years, you're looking at 11.

Same story for income-driven repayment forgiveness. Need 20 or 25 years of payments (depending on your plan)? Forbearance months don't count toward that total. Two years of forbearance means you'll make payments for 27 years before receiving forgiveness.

Your repayment timeline stretches:

When interest capitalizes after forbearance, your monthly payment under the Standard Repayment Plan goes up to account for the higher balance. Or, if you keep paying the same amount you paid before, you'll take longer to pay off the loan. Either way, you're paying more total interest over the life of the loan.

Credit score implications:

Forbearance itself doesn't hurt your credit. Your account shows current—no late payments, no delinquencies reported. But you're not building positive payment history during that time either. Your credit report just shows the account exists and is current.

The real risk comes after forbearance ends. If you can't resume payments and immediately start missing them, your credit score drops fast. That first 30-day late payment can knock 50-100 points off your score. At 90 days delinquent, you're looking at serious damage that takes years to recover from.

Use the forbearance period to actually fix the underlying problem—find new income, cut expenses, apply for income-driven repayment. Don't just coast for six months and hope things magically improve.

Author: Danielle Pierce;

Source: sonicmusic.net

How to Apply for Student Loan Forbearance

Log into your loan servicer's website. Federal loan servicers right now include MOHELA, Nelnet, EdFinancial, and a handful of others. Not sure who services your loans? Check StudentAid.gov—log in with your FSA ID and you'll see your servicer listed.

Look for the forbearance request section. Usually buried under "Manage Payments" or "Repayment Options" or something similar.

You'll answer questions about:

- What type of forbearance you need (general or mandatory)

- Why you need it

- How long you're requesting

- Upload documentation if required

What documents you'll need for mandatory forbearance:

- Income-based mandatory forbearance: Last two pay stubs or most recent tax return. Your servicer's statement showing what you owe monthly. They'll do the math to verify your payments exceed 20% of gross income.

- Medical/dental residency: Letter on official letterhead from your program director confirming enrollment and residency dates.

- AmeriCorps: Enrollment verification letter from your program showing service dates.

- National Guard duty: Copy of your military orders showing active duty period.

General forbearance is looser. You write a paragraph explaining your situation. "Lost my job on March 15, interviewing actively but no offers yet, need three months to get reemployed" works fine. No pay stubs or documentation required unless your servicer specifically asks.

Timeline for approval:

Submit at least two weeks before your next payment due date. Processing usually takes 5 to 10 business days. Sometimes longer during high-volume periods (like fall when lots of borrowers' grace periods end).

If you submit with only a few days before your payment is due, call your servicer to confirm they've received your request and the payment won't process while it's under review.

If they deny your request:

For general forbearance, denial is final for that request. Your servicer decided no. You can submit a new request with more detail or wait a month and try again, but there's no appeal process.

For mandatory forbearance, denial usually means your documentation was incomplete or didn't prove eligibility. Call and ask exactly what's missing. "You need a pay stub from the last 30 days, not from two months ago" or "This letter needs to be on official program letterhead, not just an email from your supervisor." Fix the documentation issue and resubmit—they have to approve if you meet the requirements.

Private loan forbearance works differently:

Each lender makes up their own rules. Discover might offer six months maximum. Sallie Mae might allow 12 months. Some lenders have online forbearance request forms. Others require you to call or mail a paper form.

Be ready to explain why you need forbearance and provide supporting documents—termination letter from your employer, hospital bills, proof of income reduction. Private lenders typically want to see evidence that your hardship is real and temporary.

Alternatives to Student Loan Forbearance

Before you click "submit" on that forbearance request, spend 20 minutes exploring whether something else works better.

Income-driven repayment plans (federal loans):

IDR plans calculate your payment as a percentage of discretionary income—anywhere from 5% to 20% depending on which plan you choose. The SAVE plan, which fully rolled out in 2025, offers the best terms: 5% of discretionary income for undergraduate loans, 10% for graduate loans. Undergraduate-only borrowers get forgiveness after 20 years instead of 25.

Someone earning $28,000 per year with $35,000 in undergraduate loans might qualify for a $30 monthly payment under SAVE. Maybe even $0 if they claim certain deductions or have dependents.

Here's the key advantage over forbearance: even a $0 payment counts as a qualifying payment toward forgiveness. Make $0 payments for 12 months on an IDR plan, and you've made 12 months of progress toward your 20-year forgiveness timeline. Make zero payments for 12 months in forbearance, and you've made zero progress toward anything except accumulating interest.

Apply at StudentAid.gov. Use the Loan Simulator tool to estimate your payment under different plans. Application processing takes four to six weeks typically. If you need coverage during that gap, request forbearance temporarily—but the end goal is getting onto IDR, not staying in forbearance.

Deferment options:

Already covered the details earlier, but worth repeating: if you're unemployed and receiving benefits (or actively job hunting), apply for unemployment deferment. If you receive means-tested federal benefits or earn below 150% of poverty level, apply for economic hardship deferment. Both beat forbearance because subsidized loan interest doesn't accrue during certain deferment periods.

Federal consolidation:

A Direct Consolidation Loan combines multiple federal loans into one new loan. Your interest rate becomes the weighted average of your old rates, rounded up to the nearest eighth of a percent. So you're not saving money on interest.

Why consolidate then? Access to repayment plans. Parent PLUS loans don't qualify for most IDR plans, but if you consolidate them and jump through specific hoops (the "double consolidation loophole"), you can access IDR. Similarly, some older FFEL loans need consolidation before they're eligible for SAVE or PSLF.

Consolidation also resets your grace period, giving you six months before payments resume. Use that strategically if you need breathing room.

Don't consolidate just to consolidate. Do it when it unlocks a specific benefit you need.

Refinancing (kills federal protections):

Refinancing means a private lender pays off your federal loans and issues you a new private loan, ideally at a lower interest rate. If you've got strong credit and steady income, you might refinance a 6.5% federal loan down to 4.0% private.

The catch: your loans are now private. Forever. You've permanently given up access to income-driven repayment, PSLF, federal deferment and forbearance options, and any future federal relief programs.

Only refinance federal loans if you're absolutely certain you won't need federal protections. Good candidate: high earner with stable job, no interest in forgiveness programs, wants to pay loans off quickly and save on interest.

Bad candidate: anyone pursuing PSLF, anyone working in a field with income volatility, anyone who might need income-driven repayment if their financial situation changes.

Servicer payment plans:

Some servicers offer alternative payment arrangements outside the official forbearance/deferment system. Might be a temporary payment reduction, or spreading missed payments across future months, or a short-term modified payment plan.

Call your servicer and ask what options exist beyond forbearance. Sometimes they can work out a solution that keeps you actively paying (which is better for your forgiveness timeline and interest costs) while still reducing your burden temporarily.

Author: Danielle Pierce;

Source: sonicmusic.net

Frequently Asked Questions About Student Loan Forbearance

Forbearance keeps you from drowning when financial emergency strikes. It stops the collection calls, prevents default marks on your credit report, and gives you space to catch your breath.

But breathing room isn't free. Every month in forbearance costs you interest that compounds over time. On a $50,000 loan balance, a year of forbearance might add $2,500 to $3,500 in interest that capitalizes and then accrues its own interest for years afterward.

Before you request forbearance, exhaust better options. Income-driven repayment might set your payment at $0 based on your income—same immediate relief as forbearance, but those $0 payments count toward forgiveness and you avoid interest on subsidized loans. Deferment provides similar payment pauses with potentially better interest treatment. Servicer payment plans might reduce your payment temporarily without the full forbearance cost.

If forbearance truly is your best option, use it strategically. Set a specific end date tied to when your situation improves. Pay interest monthly if you can afford even $50 or $100. And use those forbearance months productively—find new work, apply for income-driven repayment, restructure your budget, address the root cause of your hardship.

The worst forbearance outcome: stringing together year after year of forbearance, watching your balance grow by $10,000 or $15,000, and emerging with the same income problem you started with but way more debt.

The best outcome: three to six months of forbearance while you solve a specific, temporary crisis, then resuming payments with your finances stabilized and minimal long-term cost.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.