Overhead view of a desk with a laptop showing a federal student loan website, documents, a calculator, a pen, and a coffee cup on a light wooden surface

How to Discharge Student Loans in the United States?

Over 43 million Americans carry student loan debt, yet most don't realize their loans might qualify for complete elimination under federal discharge programs. Here's what makes discharge different: you're not gradually paying down your balance or waiting decades for forgiveness. When you qualify for discharge, your entire loan obligation vanishes—sometimes within 90 days of applying.

The catch? You need specific, documented circumstances that federal law recognizes as grounds for discharge. A vague sense that "college wasn't worth it" won't cut it. But if you developed a severe disability, your school shut down mid-semester, or you were defrauded by a diploma mill, discharge programs could wipe out your debt entirely.

This 2026 guide breaks down each discharge pathway available right now, walks you through the actual application steps, and explains what changes after your balance hits zero.

What Is Student Loan Discharge?

When your loans get discharged, the federal government or your lender eliminates your legal responsibility to repay the remaining balance. Collections stop. Your servicer adjusts your account to zero. You're done.

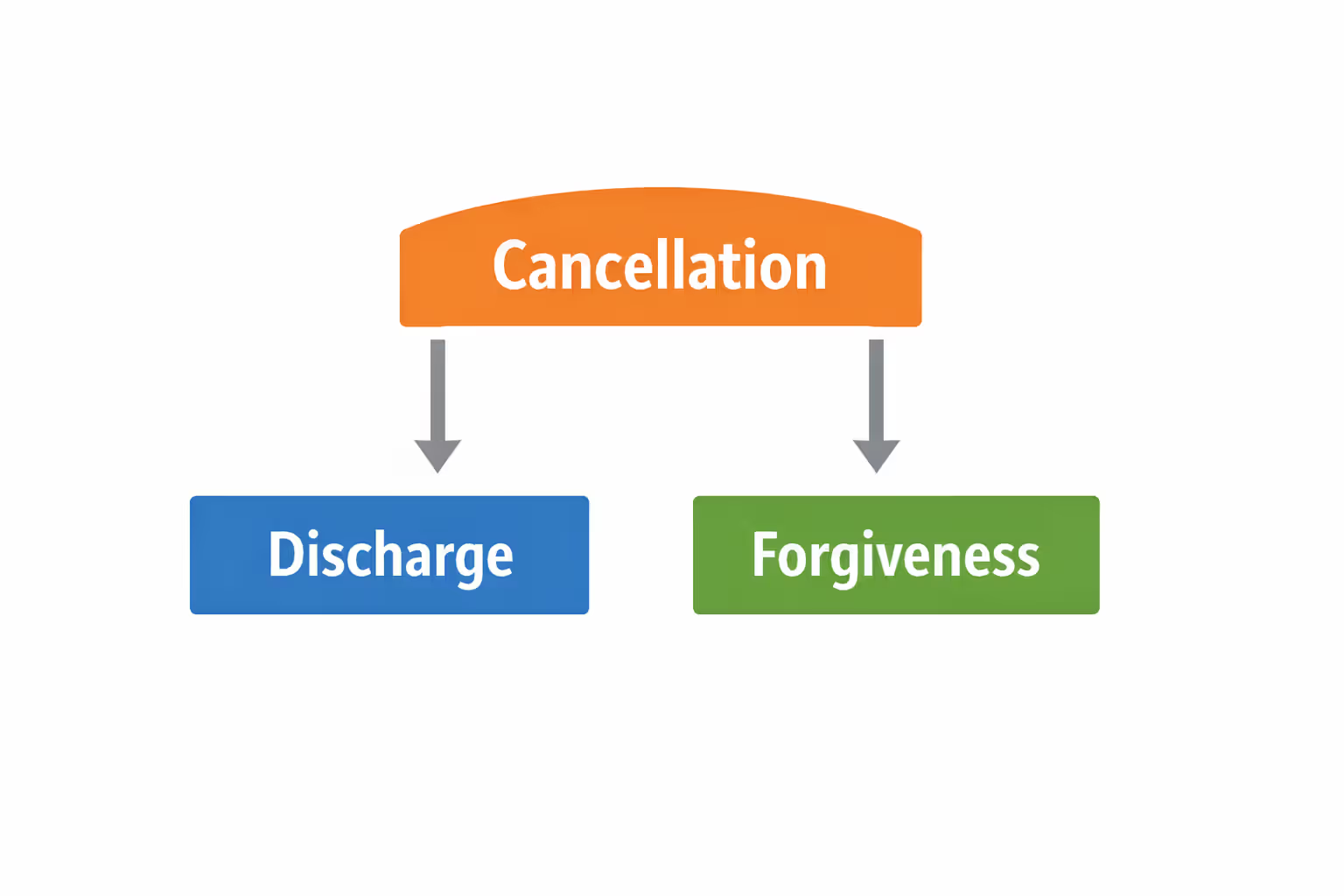

People constantly mix up three related terms—discharge, forgiveness, and cancellation—but they're not interchangeable. Discharge applies when specific external circumstances make continued collection unreasonable: you can't work due to permanent disability, your school disappeared before you graduated, or the school forged your loan application. Forgiveness describes debt elimination after you've jumped through hoops for years—120 monthly payments while working for a nonprofit, or 240-300 payments on an income-driven plan. Cancellation? That's the umbrella term covering both.

Author: Marcus Bennett;

Source: sonicmusic.net

Here's the crucial difference in practice. Federal loan programs include multiple discharge pathways with clear eligibility criteria. The Department of Education administers these for Direct Loans, FFEL loans, and Perkins Loans. Private lenders? They're under no obligation to discharge anything except in cases of death, and even disability discharge varies wildly by lender. If you borrowed from Sallie Mae, Discover, or a credit union, your promissory note controls what's possible—and most private loan contracts offer minimal discharge provisions.

Most federal discharges don't demand years of service or hundreds of payments. Meet the eligibility standard, submit your documentation, and you could see discharge approval in three to four months. That said, each program sets strict requirements, and the Department of Education will reject applications missing critical documentation without a second thought.

Legal Grounds for Student Loan Discharge

Federal regulations recognize six main scenarios where discharge becomes available. Each operates independently with separate applications and proof requirements.

Discharge Due to Total and Permanent Disability

Total and Permanent Disability discharge—everyone calls it TPD—eliminates federal loans when you can no longer work due to a severe, lasting impairment. Three documentation paths exist, and which one you use determines how quickly you'll get approved.

If you're receiving Social Security Disability Insurance or SSI benefits, you can apply using your SSA award information. Veterans with service-connected disabilities rated as unemployable by the VA can submit their VA documentation. Both routes typically lead to faster approval because the federal government has already verified your disability status.

The third path requires physician certification, and it's stricter than most borrowers expect. Your doctor must certify that you cannot engage in "substantial gainful activity" due to a physical or mental condition expected to last at least 60 continuous months or result in death. That's not "I can't do my old job as a construction worker." That's "I cannot perform any work that would earn meaningful income." Many applicants with legitimate disabilities get denied because their condition doesn't meet this federal threshold.

After approval, you'll enter a three-year monitoring period—not a suggestion, but a mandatory review window. During these three years, your annual earnings can't exceed 100% of the federal poverty guideline for your household size. You can't take out new federal student aid. And you must respond to the Department of Education's annual income verification requests. Miss a deadline or earn too much, and your loans get reinstated with all accumulated interest. Successfully navigate three years, though, and your discharge becomes permanent. Current tax law doesn't treat TPD discharge as taxable income, a significant improvement from pre-2018 rules.

School Closure Discharge

Your school closing while you're enrolled—or within 180 days after you withdrew—can trigger automatic discharge of your federal loans. This covers Direct Loans, FFEL loans, and Perkins Loans tied to that school.

You won't qualify if you finished your program before the closure, even if the school shut down a week after your graduation ceremony. Transfer students who completed a comparable program elsewhere also don't qualify—discharge exists for students who paid tuition but never received the credential they were promised.

Author: Marcus Bennett;

Source: sonicmusic.net

When major institutions collapsed—ITT Tech in 2016, Corinthian Colleges in 2015, and numerous smaller schools since—the Department of Education identified eligible borrowers and processed discharges automatically for many of them. If your school closed and you haven't received a discharge notice, don't assume you're ineligible. Servicer databases aren't perfect. Submit an application through StudentAid.gov with your enrollment dates and the closure date (the Department maintains a public closure list).

Processing usually takes two to three months once your application is complete. If you transferred credits to another school after closure, be prepared to explain why you couldn't complete a comparable program there—maybe your new school didn't offer your major, or you couldn't afford to continue.

False Certification and Unpaid Refund Discharge

False certification discharge covers three specific situations where schools fraudulently certified your loan eligibility. First: the school forged your signature on loan documents. Second: the school certified you as eligible when you clearly didn't meet basic requirements, like lacking a high school diploma or GED when one was mandatory. Third: the school certified your eligibility despite a disqualifying condition—for instance, enrolling you in a nursing program when state law would prevent you from obtaining licensure due to a prior felony conviction.

Unpaid refund discharge applies when you withdrew from school, qualified for a tuition refund under the school's published policy, but the school never paid that refund and didn't return the loan funds to your lender either. This happened frequently when for-profit chains imploded overnight, leaving students without refunds and lenders without repayment.

Both discharge types require concrete proof. For forged signatures, you'll need to show the signature on your loan documents doesn't match your actual signature (handwriting analysis, notarized statements). For ability-to-benefit fraud, you'll need evidence that you didn't have a high school credential when the school certified you as eligible. For unpaid refunds, bring your withdrawal documentation, the school's refund policy, and records showing you never received payment.

These discharges happen less frequently than TPD or closed school discharges, but they're vital when schools engage in blatant fraud.

Borrower Defense to Repayment

Borrower defense lets you pursue discharge when your school lied to you or violated state consumer protection laws in ways that directly relate to your loan or the education you financed. Common examples: the school advertised a 95% job placement rate when it was actually 40%, promised accreditation it didn't have, guaranteed you'd pass a licensing exam after completion, or inflated graduate salary figures in recruitment materials.

You'll need evidence—not just your recollection. Bring the brochure that promised those outcomes, the recruitment presentation slides, emails from admissions counselors, testimony from classmates who heard the same claims. The more specific you can be—"On March 15, 2019, admissions counselor Jennifer Martinez told me in a recorded phone call that 100% of graduates found work within 30 days"—the stronger your claim.

Author: Marcus Bennett;

Source: sonicmusic.net

The Department of Education reviews each borrower defense application individually, weighing your evidence against the school's records (if available). Processing times stretched to multiple years during the 2017-2021 backlog, but current regulations require decisions within three years of receipt. During review, you can request forbearance to pause payments, though interest keeps accruing unless you're in default.

Approval doesn't guarantee full discharge. The Department may grant partial discharge based on the harm they calculate you suffered. If approved, you'll receive notification of how much is discharged and whether you owe a remaining balance.

Borrower defense claims exploded after Corinthian Colleges, ITT Tech, and other large chains collapsed under fraud investigations. Rules governing borrower defense have changed multiple times—different standards apply depending on when you took out your loans—but 2026 regulations provide clearer timelines and more transparent decision criteria.

Death Discharge

When a borrower dies, their federal student loans are discharged automatically. Parent PLUS loans work slightly differently: the debt disappears if either the parent who borrowed or the student for whom the loan was taken passes away.

Survivors need to contact the loan servicer promptly and submit a certified copy of the death certificate. Most servicers have dedicated phone lines for death discharge notifications. Processing typically takes 60 to 90 days, and any payments made after the date of death should be refunded to whoever made them or to the estate.

Private loan death discharge is entirely lender-dependent. Many major private lenders now discharge loans upon death, but not all, and some only implemented these policies in the past five years. Without a death discharge provision in your loan agreement, the debt becomes part of the deceased borrower's estate, meaning it must be paid from estate assets before heirs receive anything. Check your private loan promissory note or contact your servicer directly to confirm their death discharge policy.

How to Apply for Student Loan Discharge

Application mechanics vary significantly across discharge types, but a common pattern emerges: assemble your documentation first, then submit through the correct channel, and expect a waiting period measured in months, not weeks.

For TPD discharge, you'll work through the dedicated portal at disabilitydischarge.com rather than StudentAid.gov. SSA and VA applicants can often complete the entire process online by providing their benefit information. Physician certification requires your doctor to fill out a specific form (available on the portal) with detailed medical information, then sign and date it. You submit that completed form through the portal or by mail. Expect 90 to 120 days for a decision, sometimes faster if you're using SSA or VA documentation since the government's already verified your disability status.

School closure discharge applications go through StudentAid.gov, though many eligible borrowers receive automatic discharge without applying. If you're waiting for automatic discharge but it hasn't arrived six months after your school closed, don't wait longer—submit your application manually. You'll need documentation proving your enrollment dates and the school's closure date (both available from the Department's closure list). Allow 60 to 90 days for processing.

False certification, unpaid refund, and borrower defense applications all funnel through StudentAid.gov, but they're more complex than other discharge types. For borrower defense specifically, you'll complete a detailed narrative explaining what your school told you, why it was false or misleading, and how you relied on that misinformation when taking out loans. Vague accusations won't work—you need dates, names, specific statements, and supporting documentation. Processing times range from six months to two years depending on how many applications the Department is reviewing and how well-documented yours is.

Death discharge begins with a phone call to your servicer (or the deceased's servicer) followed by mailing or uploading a certified death certificate. Most large servicers have specialized departments handling these requests. Processing is usually straightforward, completed within 60 to 90 days barring unusual circumstances.

During the review period, your loans stay in whatever status they were in when you applied. You can request forbearance for most discharge types, which pauses required payments but lets interest pile up. TPD applicants using SSA documentation automatically enter forbearance. Here's critical: keep making payments if you're financially able until you receive official written confirmation of discharge. Stopping payments prematurely based on an assumption of approval can trigger delinquency, tank your credit score, and potentially push you into default.

Bankruptcy and Student Loan Discharge

Yes, student loans can be discharged in bankruptcy—but the bar is set considerably higher than for credit cards, medical bills, or personal loans. You must file what's called an adversary proceeding, essentially a lawsuit within your bankruptcy case, and convince a judge that repaying your loans would create "undue hardship" for you and your dependents.

Most courts apply the Brunner test, named after a 1987 Second Circuit case that established a three-part standard. You must prove: (1) you can't maintain even a minimal standard of living for yourself and your dependents while repaying the loans, (2) additional circumstances exist showing this situation will persist for a significant portion of the repayment period, and (3) you've made good faith efforts to repay before seeking discharge.

Courts historically interpreted Brunner extremely strictly. Judges denied discharge to borrowers who theoretically could take a second job, move to cheaper housing, or enroll in income-driven repayment plans—even when those options would leave the borrower in poverty indefinitely. Bankruptcy discharge became nearly mythical, something everyone had heard was possible but almost no one successfully obtained.

Recent developments have cracked the door open wider. In November 2022, the Department of Justice issued new guidance urging bankruptcy courts to apply the undue hardship standard more realistically, acknowledging decades of overly harsh interpretations. Several circuit courts have adopted more flexible approaches to Brunner, and some jurisdictions use different tests entirely (the Totality of Circumstances test, for example).

In 2026, more borrowers are succeeding at bankruptcy discharge than in previous decades, particularly those with severe, permanent disabilities that don't quite meet TPD standards, older borrowers (50+) with high debt-to-income ratios and limited future earning potential, and borrowers with exceptionally high balances relative to their career earnings prospects. Still, bankruptcy discharge remains uncommon. It's expensive, time-consuming, and absolutely requires an attorney—preferably one with specific experience in student loan adversary proceedings.

Not all bankruptcy lawyers handle these cases. Many avoid them because they're complex and success isn't guaranteed. If you're considering this route, find an attorney who's successfully discharged student loans in bankruptcy before. Expect the process to cost several thousand dollars in legal fees beyond your regular bankruptcy costs.

Common Mistakes When Seeking Discharge

Borrowers frequently torpedo their own discharge applications through preventable errors. Here are the deadliest mistakes and how to avoid them.

Missing deadlines. Closed school discharge has specific timeframes—you must have been enrolled within 180 days of closure. Borrower defense claims face statute of limitations issues depending on when you attended school and which regulations apply to your loans. Mark every deadline clearly and submit applications at least two weeks before they expire. Mail delays happen. Website glitches happen. Give yourself buffer time.

Submitting incomplete documentation. A TPD application with physician certification requires your doctor to complete every single field on the form and sign it with their license number. Leaving the "expected duration of disability" section blank? Automatic rejection. For borrower defense, writing "My school lied about job placement" without specific examples, dates, or evidence gets you nowhere. Before hitting submit, review your application as if you're the skeptical bureaucrat who has to approve it. Does every claim have supporting documentation? Is every form field filled out? Did everyone who needs to sign actually sign?

Author: Marcus Bennett;

Source: sonicmusic.net

Misunderstanding eligibility requirements. Your school being investigated by the FTC doesn't automatically entitle you to discharge. You must show how the school's specific misconduct affected you personally. Having a disability doesn't guarantee TPD approval—your condition must meet the federal "unable to engage in substantial gainful activity" standard. Read eligibility criteria carefully and honestly assess whether you meet them before applying.

Applying for the wrong relief program. School closed while you were enrolled? Apply for closed school discharge, not borrower defense. Developed a permanent disability? Pursue TPD discharge, not forbearance or deferment. Each discharge type serves a specific purpose with defined eligibility standards. Using the wrong application wastes months.

Assuming private loans work like federal loans. Private lenders are not bound by federal discharge programs. If you have private loans from Sallie Mae, Discover, Wells Fargo, or a credit union, those lenders have no obligation to offer closed school discharge, borrower defense, or any discharge except what's written in your original loan contract. Contact your private lender directly to understand what options exist—don't waste time applying for federal programs that don't apply to your private debt.

Comparison of Student Loan Discharge Types

| Discharge Type | Who Qualifies | How to Apply | How Long It Takes | Tax Bill? |

| Total and Permanent Disability | You receive SSA disability benefits or VA unemployability determination, OR your physician certifies you cannot perform substantial gainful work for at least 60 months | Submit application at disabilitydischarge.com with SSA/VA documentation or completed physician certification form; three-year income monitoring follows approval | Typically 90-120 days to decision; must complete three years of monitoring before discharge is permanent | No tax consequences under 2026 law |

| School Closure | You were enrolled when your school closed its doors, or you withdrew within the 180 days before closure; you didn't finish your program at another school | Often processed automatically by Department of Education; if not, submit application at StudentAid.gov with proof of enrollment dates and school closure | 60-90 days from application, though automatic discharge may happen without any action from you | No tax consequences under 2026 law |

| False Certification | Your school forged your signature on loans, certified you as eligible when you lacked required high school credentials, or certified you despite a legal disqualification | Apply at StudentAid.gov with documentation proving the false certification (signature analysis, credential records, disqualifying status proof) | Six to twelve months | No tax consequences under 2026 law |

| Borrower Defense | Your school made substantial misrepresentations about job placement, accreditation, costs, or other key factors that you relied on when borrowing | Apply at StudentAid.gov with detailed narrative and evidence of the school's misrepresentation and the harm you suffered | Six months to two years (regulations require decision within three years) | No tax consequences under 2026 law |

| Death Discharge | Borrower passes away (for Parent PLUS loans, discharge occurs if either the parent borrower or the student dies) | Family member or estate executor submits certified death certificate to loan servicer | 60-90 days after servicer receives death certificate | No tax consequences under 2026 law |

| Bankruptcy | You prove "undue hardship" to a bankruptcy judge through an adversary proceeding (typically using Brunner test: can't maintain minimal living standard, situation is long-term, made good faith repayment efforts) | File adversary proceeding within your bankruptcy case with an attorney; must present evidence and argue case before judge | Highly variable; typically six to eighteen months from adversary proceeding filing to decision | Discharged in bankruptcy means no tax bill |

What Happens After Your Student Loans Are Discharged

Your loan servicer will send written notification once your discharge is approved. Your loan balance immediately drops to zero. You're no longer legally obligated to make payments. If you made payments during the review period after the qualifying event occurred—for example, payments made after you became disabled but before your TPD application was approved—you may receive refunds for those payments.

Tax implications have changed dramatically in recent years and depend on which discharge program eliminated your debt. As of 2026, essentially all federal student loan discharges are excluded from taxable income. TPD discharge, closed school discharge, borrower defense, false certification, death discharge—none generate taxable income under current federal law. This represents a major shift from pre-2018 rules when many discharged balances were treated as "cancellation of debt income" that triggered surprise tax bills. Tax laws change, though, so consult a CPA or tax attorney when you receive discharge to confirm current treatment.

Your credit report will be updated to reflect the discharge. The loan accounts remain on your report for seven years from either the discharge date or the date of last activity before discharge, but they'll show zero balances and a notation indicating discharge. Discharge itself isn't negative—eliminating debt actually improves your debt-to-income ratio. However, if your loans were in default before discharge, that negative payment history stays on your report for the full seven-year period.

TPD discharge recipients face a three-year monitoring period during which the Department of Education tracks your income and student aid activity. You'll receive annual requests to verify your income. Respond to every single one. If your income exceeds the poverty guideline for your household size, if you receive new federal student aid, or if you ignore monitoring requests, your discharged loans can be reinstated with all accumulated interest. After three years of successful monitoring, your discharge becomes permanent and cannot be reversed.

Partial discharge through borrower defense means you still owe whatever balance wasn't discharged. The Department will notify you of your adjusted balance, and you'll resume repayment according to your previous plan or a new plan you select.

Keep your discharge documentation forever. Store your approval letter, final discharge notice, and final account statements in a fireproof safe or secure digital storage. Loan servicers make mistakes, databases get corrupted, and records get lost. If your discharged loans ever reappear as active or get sent to collections due to servicer error, your discharge paperwork is your proof that you don't owe anything.

We've seen substantial evolution in how the Department of Education handles discharge applications over the past five years, particularly for borrower defense claims and automatic closed school discharges.The Department has taken a much more favorable stance toward borrowers who attended schools that engaged in misconduct. But here's what borrowers consistently get wrong: they assume discharge happens automatically, or they assume they don't qualify without actually checking. The reality is you must actively apply for most discharge types, your documentation needs to be thorough and specific, and processing can take months or even years. The biggest mistake I see is people giving up before they start because they assume the process is impossible or not worth the effort

— Michael Stratton

Frequently Asked Questions About Student Loan Discharge

Student loan discharge provides a legitimate escape route for borrowers facing specific qualifying circumstances. Whether you're dealing with permanent disability, attended an institution that collapsed or defrauded students, or face other recognized grounds for discharge, understanding these programs could save you decades of payments and eliminate six figures of debt.

The critical factor is taking action when you identify potential eligibility. Collect your documentation, complete applications with thorough detail, and maintain regular contact with your loan servicer throughout the process. These discharge programs exist because Congress recognized that certain situations make loan repayment fundamentally unjust or impossible—don't let confusion or intimidation prevent you from pursuing relief you're legally entitled to receive.

If you're uncertain about your eligibility, multiple resources can help. StudentAid.gov provides comprehensive information about each discharge program, downloadable application forms, and your loan servicer's contact information. For complicated situations—particularly borrower defense claims involving institutional fraud or bankruptcy proceedings—consulting with a student loan attorney or nonprofit credit counselor can clarify your options and improve your approval odds. Many legal aid organizations and nonprofit counseling agencies offer free or low-cost consultations for borrowers navigating discharge applications.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.