Top-down view of a student desk with a laptop showing interest rate charts, financial documents, a calculator, a graduation cap, and dollar bills

Student Loan Interest Rates Guide

Your tuition bill is just the starting line. By the time you've made your last payment—maybe 10, 15, or even 25 years down the road—you could've paid back nearly twice what you borrowed. That extra money? It's interest, and it's why the rate you lock in today matters so much.

Right now, you might be comparing federal options against private lenders, or scratching your head wondering why your roommate got quoted 4.5% while you're looking at 8%. Here's the thing: understanding how these rates work isn't just helpful—it's the difference between paying $15,000 in interest versus $30,000 on the same loan amount.

What Are Student Loan Interest Rates

Think of interest as rent you pay for using someone else's money to fund your degree. If you take out $10,000 at 5%, you'll owe about $500 in interest that first year (though this drops as you pay down the balance). Simple enough, right?

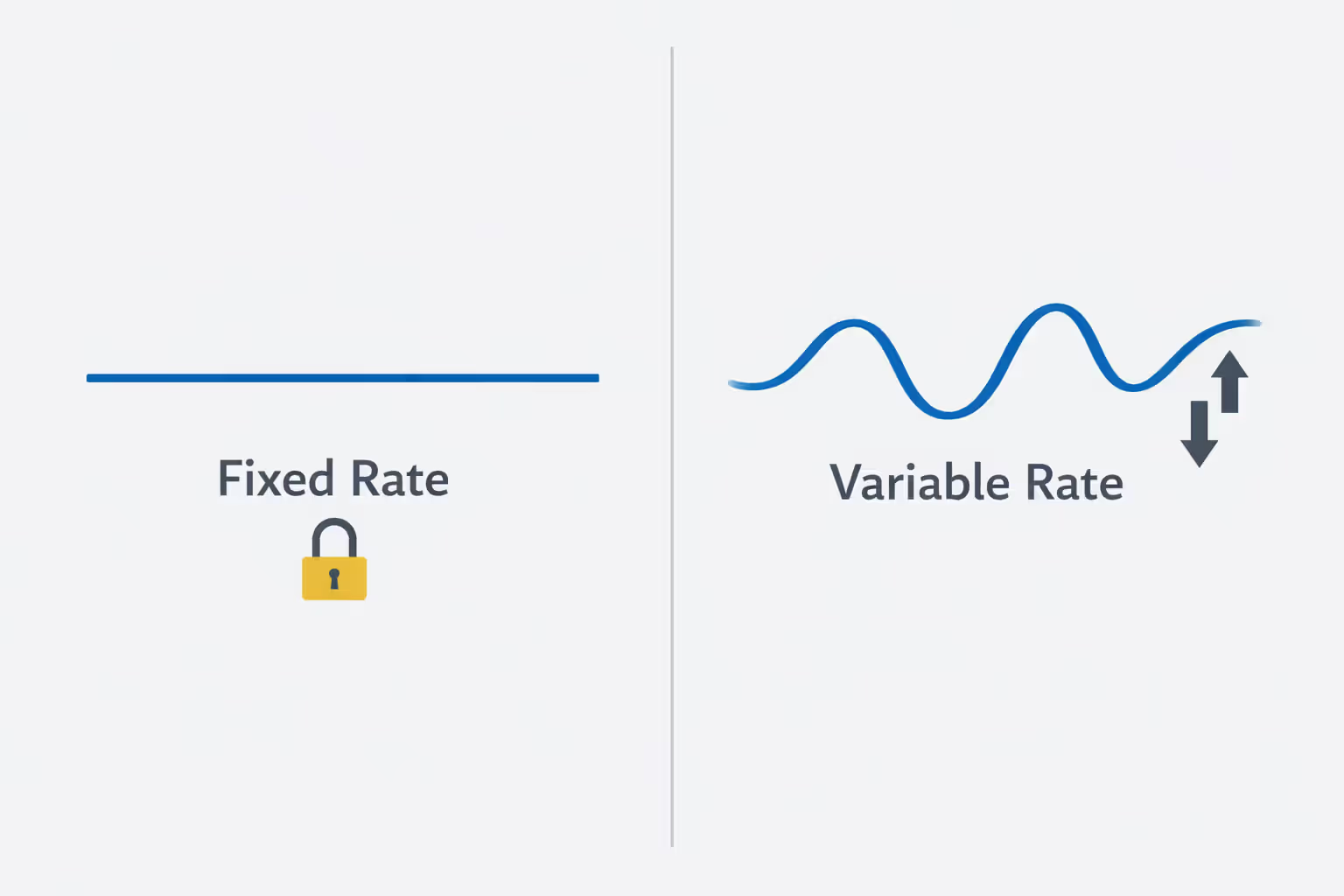

Here's where it gets interesting. Student loan interest rates explained in practical terms: you're choosing between two completely different animals.

Fixed rates lock in at one percentage when you sign, and that number never budges. You could be repaying through economic booms, recessions, whatever—your rate stays put. Planning your budget becomes straightforward because your payment amount won't surprise you five years from now.

Variable rates, though? They're tied to economic indexes like SOFR (Secured Overnight Financing Rate), recalculating every few months. You might start at 4.5%, which sounds great. But two years later, if the Federal Reserve has been hiking rates aggressively, you could be sitting at 7%. Or if markets soften, maybe you'll drop to 3.5%. It's a gamble.

Author: Olivia Harrington;

Source: sonicmusic.net

What is the interest rate on student loans going to cost you in real terms? Consider this: on a $40,000 loan over 10 years, moving from 5% to 7% adds roughly $4,600 to your total repayment. That's a decent used car.

Fixed rates mean you sleep better at night—no payment anxiety. Variable rates often start lower (that's the bait), but you're accepting uncertainty. Can you absorb an extra $200-300 monthly if rates spike?

Every federal loan comes fixed. Period. Private lenders? They'll offer you both flavors, and you'll need to pick your poison based on your financial situation and risk tolerance.

Current Federal Student Loan Interest Rates

Congress sets these rates using a formula: they check the 10-year Treasury note auction in May, add some percentage points on top, and boom—that's your rate for any loan disbursed between July 1 and June 30 of the next year. Everyone borrowing during that window gets the identical rate.

For the 2025-2026 academic year (that's July 1, 2025 through June 30, 2026), here's what we're working with:

Undergraduate Federal Loan Rates

Author: Olivia Harrington;

Source: sonicmusic.net

Direct Subsidized and Unsubsidized Loans for undergrads? You're looking at 5.50% fixed. Doesn't matter if you're a freshman borrowing $3,500 or a senior maxing out at $12,500—same rate.

Now, "subsidized" versus "unsubsidized" doesn't change your percentage. What changes is when interest piles up. Got a subsidized loan? The government covers your interest while you're in school (at least half-time), during your six-month grace period, and if you defer payments later. Unsubsidized loans start racking up interest immediately after disbursement, even though you won't need to make payments until after graduation.

Graduate and Parent PLUS Loan Rates

Graduate students taking Direct Unsubsidized Loans pay 7.05% fixed. You can borrow up to $20,500 annually this way. The higher rate reflects that you're borrowing more over a longer timeline.

PLUS Loans—available to grad students and parents of dependent undergrads—hit 8.05% fixed. But wait, there's more (and not in a good way): you'll also pay a 4.228% origination fee upfront. Borrow $15,000, and they'll skim off about $634 before sending money to your school. You receive $14,366, but you owe $15,000. Then interest starts accumulating on that full $15,000.

Want some perspective on current student loan interest rates? During 2020-2021, undergrads were paying just 2.75%—less than half today's rate. Students who borrowed then locked in dramatically cheaper loans for the life of that debt.

Private Student Loan Interest Rates

Private lenders play by completely different rules. Banks, credit unions, online lenders—they're setting rates based on your credit profile, what's happening in financial markets, and honestly, how badly they want your business that quarter.

Interest rates on student loans from private sources typically range from 3.50% up to 14.50% for fixed options. Variable rates? Usually 2.75% to 13.00% as of early 2026.

Why such a massive spread? Because they're pricing based on risk. Someone with a 780 credit score, steady income, and a cosigner with excellent credit might snag something close to 3.5%. Another applicant with limited credit history and no cosigner could face 12% or higher—if they get approved at all.

Credit evaluation dominates everything here. Lenders are dissecting your credit score, debt-to-income ratio, employment history, and even your degree program. A nursing student at an accredited university typically gets better terms than someone pursuing an unaccredited certificate program, even with identical credit scores.

Loan amount and repayment timeline matter too. A 5-year loan often carries a lower rate than a 15-year loan from the same lender. Borrowing $5,000 versus $50,000 can affect your rate, though policies vary widely.

One upside: most private lenders skip origination fees entirely. The rate they quote is what you actually pay, making student loan rate comparison cleaner.

How Lenders Determine Your Student Loan Rate

Your credit score basically controls private student loan pricing. Most lenders won't even consider you below 650-680, but just clearing that bar doesn't mean you're getting their best offer. The difference between a 680 score and 750 score? Easily two full percentage points. On a $30,000 loan over 10 years, that's roughly $3,000 extra in interest you're paying.

Lenders check both FICO and VantageScore, usually applying whichever is lower if there's a discrepancy. Your payment history carries the most weight, followed by credit utilization and the age of your credit accounts. One single 30-day late payment in the past year can bump you up a rate tier.

Author: Olivia Harrington;

Source: sonicmusic.net

Adding a cosigner with strong credit can slash your rate by 1-3 percentage points—sometimes more. Lenders essentially underwrite based on your cosigner's financial profile instead of yours. Most let you remove the cosigner after 24-48 consecutive on-time payments, though approval isn't guaranteed and requires demonstrating you can handle the debt solo.

Picking your repayment term is a balancing act. A 5-year term might come at 5.5% while a 15-year schedule costs 7.5% from the same lender. The shorter term saves you thousands in total interest but demands higher monthly payments—think $566 versus $278 monthly on $30,000. Can you swing the higher payment? If yes, you'll save big long-term.

Your degree program and school can influence rates at some lenders. Medical and dental students often qualify for specialized products with higher borrowing limits and occasionally better rates (because lenders know their income potential). Students at schools with poor graduation rates or high default rates might face higher rates or outright denials.

Market conditions shift things too. When lenders are competing aggressively for borrowers, rates drop. During economic uncertainty or when student loan defaults are climbing, even qualified applicants see higher rates and tighter approval standards.

Comparing Student Loan Rates Across Lenders

Smart shopping means looking beyond the advertised rate. Start by getting quotes from at least 3-5 lenders using their prequalification tools—these run soft credit checks that won't hurt your score. Most deliver rate estimates within minutes once you've entered basic information.

Ignore the marketing ranges completely. That flashy "rates starting at 3.50%" only applies to their absolute best borrowers—stellar credit, short repayment terms, often with an auto-pay discount stacked on. Your actual offer might land several points higher.

Effective student loan rate comparison means examining the APR (annual percentage rate), which factors in fees. Federal loans charge origination fees—1.057% on Direct Loans, 4.228% on PLUS Loans—which aren't reflected in the stated interest rate. Most private lenders don't charge origination fees, so their APR matches their interest rate.

Author: Olivia Harrington;

Source: sonicmusic.net

Repayment options vary wildly. Some lenders require you to start paying immediately while you're still in school. Others let you defer everything until six months after graduation (matching the federal grace period). A few allow interest-only payments during school, which reduces total cost without requiring full monthly payments.

Hardship options matter more than you'd think upfront. Federal loans offer extensive deferment, forbearance, and income-driven repayment plans. Private lenders? All over the map. Some grant 12-24 months of forbearance for unemployment or financial emergencies. Others offer minimal flexibility beyond the initial grace period.

Auto-pay discounts typically trim 0.25 percentage points off your rate. Small, but on a standard 10-year loan, that saves hundreds—plus you'll never miss a payment.

Death and disability discharge protections differ dramatically. Federal loans automatically discharge if you die or become permanently disabled. Some private lenders match this protection. Others don't, leaving cosigners stuck with the full balance.

Average Student Loan Interest Rates by Loan Type

Knowing what rates borrowers typically receive helps you gauge whether your offer is competitive. Here's what the landscape actually looks like (not what the brochures promise):

Current Rate Ranges by Loan Type

| Loan Type | Rate Structure | Typical Rate Range | Who Qualifies |

| Direct Loans (Undergrad) | Fixed | 5.50% | U.S. citizen or eligible non-citizen, enrolled at least half-time |

| Direct Loans (Graduate) | Fixed | 7.05% | U.S. citizen or eligible non-citizen, admitted to grad/professional program |

| PLUS Loans (Parents & Grad Students) | Fixed | 8.05% | No adverse credit history, meets citizenship requirements |

| Private Fixed (Excellent Credit) | Fixed | 4.25% - 7.50% | Credit score 750+, verifiable income or qualified cosigner |

| Private Fixed (Good Credit) | Fixed | 7.50% - 10.50% | Credit score 680-749, income verification required |

| Private Variable (Excellent Credit) | Variable | 3.75% - 6.25% | Credit score 750+, income verification or qualified cosigner |

| Private Variable (Good Credit) | Variable | 6.25% - 9.50% | Credit score 680-749, income verification required |

Federal rates apply universally—your credit score, income, and demographics don't factor in. Every undergrad borrowing during 2025-2026 pays 5.50%, no exceptions.

Private loans tell a different story. Data from major lenders shows borrowers with cosigners receive rates averaging 2.5 percentage points lower than solo borrowers with similar credit scores.

Variable rates currently run about 1-1.5 percentage points below comparable fixed rates. But here's the catch: variable rates have climbed roughly 4 percentage points since early 2022 as the Federal Reserve raised benchmark rates repeatedly. Borrowers who chose variable rates in 2021 have watched their payments increase substantially. Those who locked fixed rates back then? Still enjoying historically low costs.

Refinancing rates—for consolidating existing education debt—typically span 3.99% to 9.50% fixed and 3.25% to 8.75% variable in early 2026. Just remember: refinancing federal loans into private products means you lose income-driven repayment and forgiveness options permanently. Only consider this if you're earning steady, solid income and won't need those protections.

The biggest mistake I see? Students celebrating approval without checking if they're getting ripped off on rate. A two-point difference seems abstract at signing, but on $50,000 over ten years, you're talking almost $6,000 in extra interest. Spend a few hours getting multiple quotes—your future self will thank you profusely

— Michael Torres

Frequently Asked Questions About Student Loan Interest Rates

Your student loan rate shapes your financial life for years—potentially decades—after you toss your graduation cap. A single percentage point difference translates to thousands in extra costs over standard repayment. That's money you could be funneling into retirement savings, a house down payment, or other financial goals.

Start with federal programs. They offer fixed rates and borrower protections that private loans can't match. Exhaust federal borrowing before touching private lenders, even if private rates look tempting. The flexibility of income-driven repayment and potential forgiveness programs provides crucial insurance against financial setbacks—job loss, disability, economic downturns.

When you need private loans to cover gaps, treat rate shopping like the major financial decision it is. Your credit profile, fixed-versus-variable choice, and repayment term all dramatically impact total costs. Borrowers who invest several hours comparing offers and understanding loan terms typically save thousands compared to those accepting the first approval letter they receive.

Remember: the lowest rate doesn't always deliver the best value. A slightly higher rate from a lender offering robust forbearance options and cosigner release might prove more valuable than rock-bottom pricing with zero flexibility. Balance rate competitiveness against the protections and features you might need during repayment.

The student loan interest rate you accept today echoes through your financial future. Choose carefully, borrow only what you absolutely need, and make sure you understand exactly what you're signing up for before you put pen to paper.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.