Student reviewing loan documents and calculator on desk with financial growth charts in background

How to Get a Student Loan Without a Cosigner?

The key lies in understanding which loan types never require cosigners, meeting specific eligibility criteria for private lenders, and knowing how to strengthen your application before you submit it.

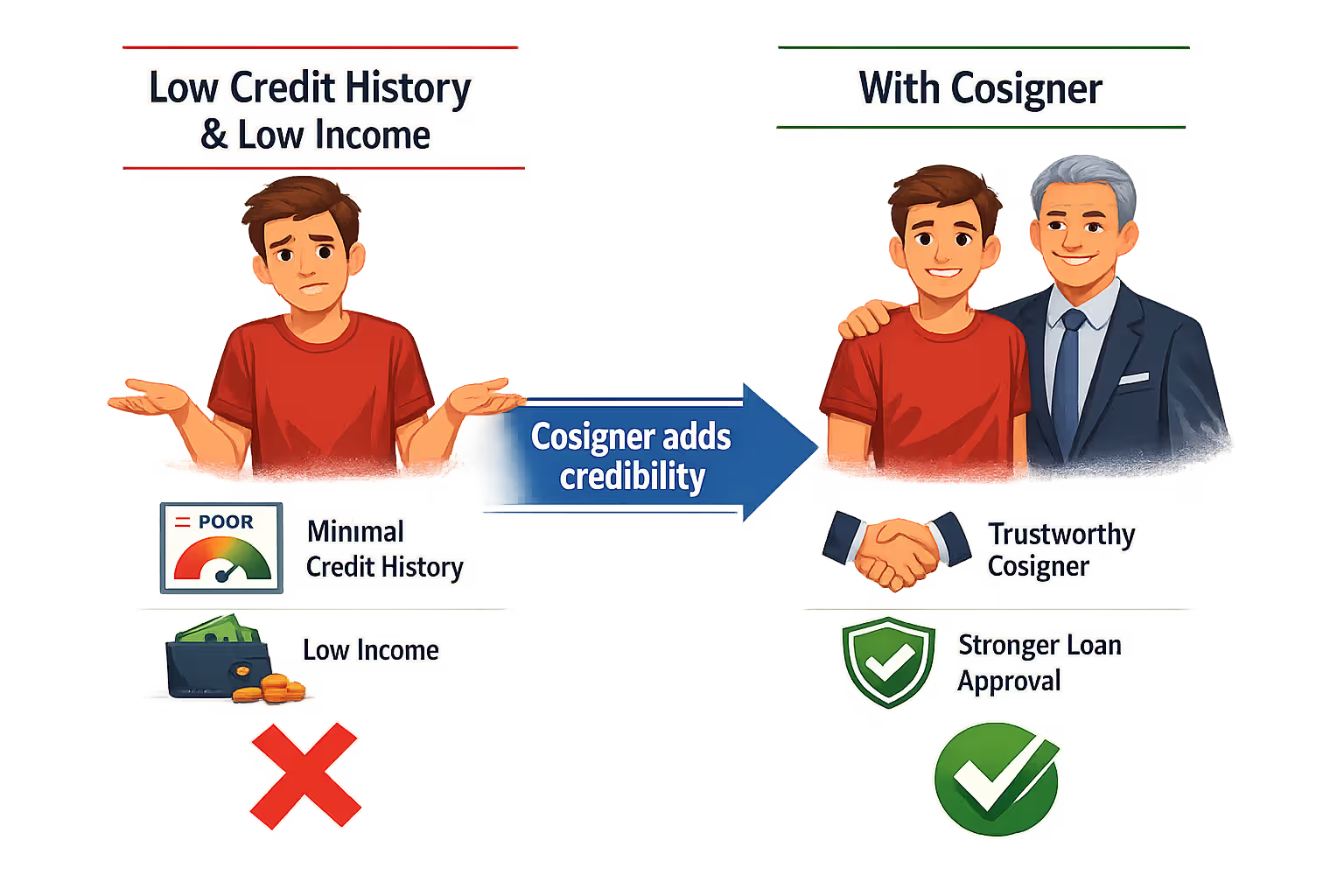

Why Most Students Need a Cosigner for Private Loans

Private lenders operate as for-profit businesses, and their underwriting standards reflect that reality. When you apply for a student loan without a cosigner, the lender evaluates only your personal credit profile and income. Most traditional college students face two immediate problems: they have minimal credit history (often just a few months of a secured card) and limited verifiable income beyond part-time work.

From a lender's perspective, this creates substantial risk. A 19-year-old with six months of credit history and $8,000 in annual income represents a borrower who statistically has higher default rates. Lenders typically want to see at least two years of credit history, a FICO score above 650, and sufficient income to manage monthly payments—criteria that exclude most undergraduates.

The cosigner solves this problem by adding a second person's creditworthiness to the application. If you default, the lender can pursue the cosigner for repayment. This guarantee allows lenders to approve loans they would otherwise reject and offer lower interest rates than they could justify based solely on a student's limited financial profile.

Income verification presents another hurdle. Private lenders generally require proof that you earn enough to handle monthly payments while attending school. For a $10,000 loan at 8% interest over ten years, you're looking at roughly $121 per month. Lenders often want to see income at least three times your monthly payment obligation, meaning you'd need to earn approximately $4,356 annually just for that loan amount—and that's before considering living expenses.

Author: Olivia Harrington;

Source: sonicmusic.net

Federal Student Loans That Don't Require a Cosigner

Federal student loans represent your first and strongest option because they never require credit checks or cosigners for most borrowers. The Department of Education bases eligibility primarily on enrollment status and financial need rather than credit history.

Direct Subsidized and Unsubsidized Loans

These federal loan programs form the backbone of student financial aid in the United States. If you qualify for subsidized funding based on demonstrated need, the Department of Education covers your interest charges during school enrollment (minimum half-time status required). The unsubsidized version extends eligibility to any undergraduate or graduate student regardless of financial circumstances, but you're responsible for interest from the moment funds are disbursed to your school.

Annual borrowing caps for 2025-2026 range from $5,500 to $7,500 for dependent undergraduates based on academic year, while independent undergraduates access up to $12,500 yearly. Graduate students qualify for as much as $20,500 per year through unsubsidized options. These amounts seem modest compared to private loan limits, but they include crucial borrower protections: fixed interest rates (5.50% currently for undergraduate unsubsidized programs), flexible income-driven repayment structures, and potential forgiveness pathways.

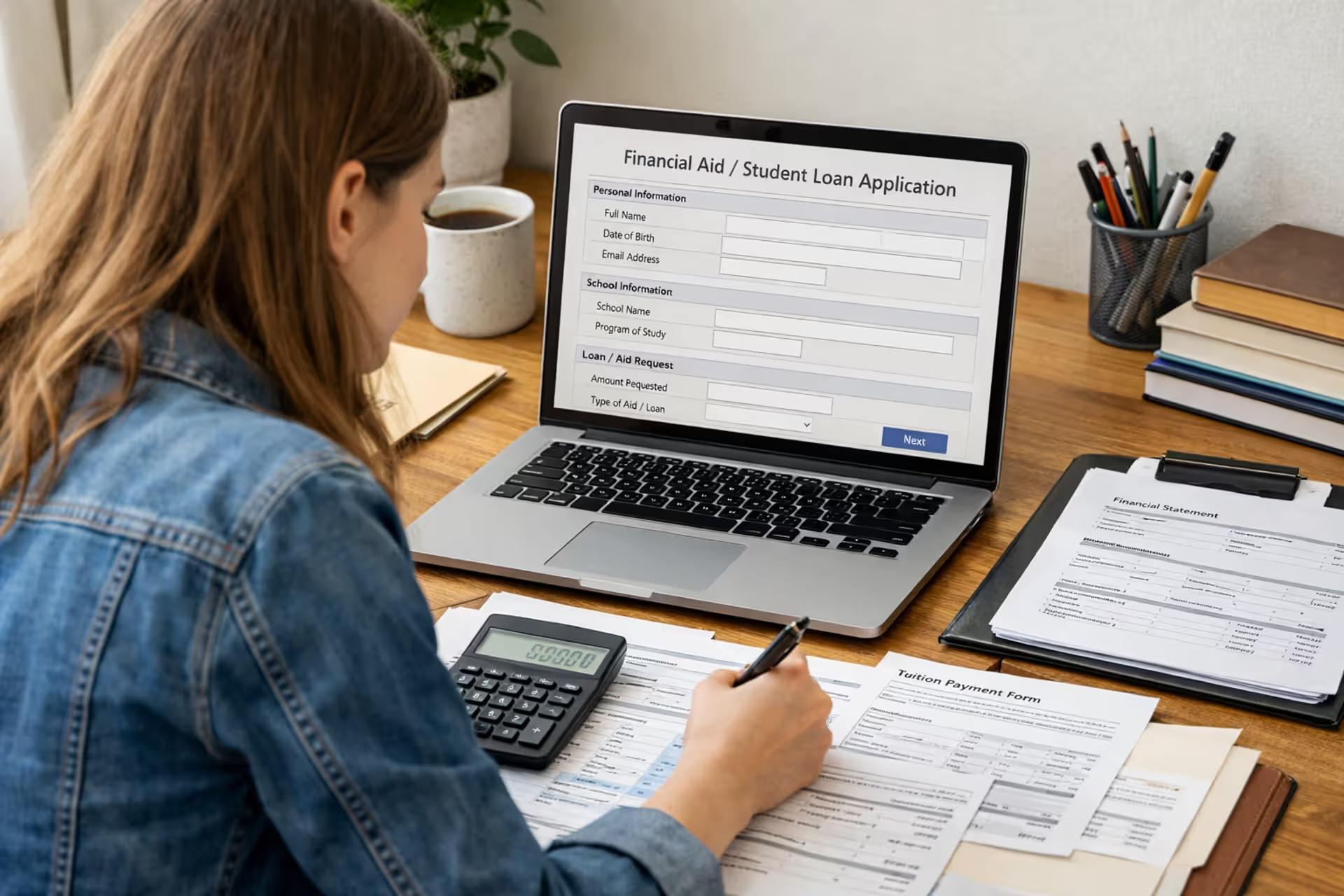

To access these student loans without a cosigner, you'll need to submit the FAFSA before your institution's financial aid deadline. Your college determines exact eligibility amounts and sends funds directly to your student account, applying them to tuition and fees first, then issuing any remaining balance for living expenses.

Author: Olivia Harrington;

Source: sonicmusic.net

Direct PLUS Loans for Graduate Students

Graduate students gain access to an expanded federal option that covers up to your total attendance cost after subtracting other aid you've received. The PLUS program differs from standard unsubsidized loans by including a basic credit evaluation, though the bar sits remarkably low—the Education Department simply checks whether you have serious adverse history like recent bankruptcies, tax liens, or accounts in collection status.

Current rates sit at 8.05% for these graduate-level PLUS loans, running higher than undergraduate federal programs but often competing favorably against private alternatives. If adverse credit history triggers a denial, you can either appeal by documenting extenuating circumstances or bring in an endorser (functionally similar to a cosigner), though that defeats the purpose if you're trying to borrow independently.

One detail catches many borrowers off guard: PLUS loans deduct a 4.228% origination fee before disbursement. Requesting $15,000 means you'll receive $14,366 but owe the full fifteen thousand. Build these origination costs into your borrowing calculations to avoid shortfalls.

Private Student Loans Without a Cosigner

A growing number of private lenders now offer no cosigner student loan options, particularly targeting graduate students, upperclass undergraduates with established credit, and career-focused borrowers. These products typically require stronger financial profiles than federal loans but can fill funding gaps when you've exhausted federal options.

Most lenders set minimum credit scores between 650 and 680, though some specialized programs accept scores as low as 620 if you have consistent income. You'll need to demonstrate enrollment at an eligible institution (most lenders maintain school lists), maintain satisfactory academic progress, and show proof of income or employment.

Interest rates vary dramatically based on your credit profile, ranging from approximately 4.99% to 14.99% APR for fixed-rate loans. Variable-rate loans might start lower but carry risk of increases over your repayment period. Loan amounts typically range from $1,000 to the full cost of attendance, though lenders may cap undergraduate borrowing at $75,000-$100,000 in total.

When evaluating no cosigner student loan options from major private lenders, consider these key differences:

| Lender Name | Credit Score Requirement | APR Range | Loan Maximum | Repayment Periods | Notable Benefits |

| Ascent | 540 minimum (specific programs) | 4.99% - 15.89% | Full attendance cost | 5, 7, 10, 15, or 20 years | Future earnings potential factors into approval |

| Funding U | No score required | 7.99% - 13.99% | $15,000 annually | 10-year term | Academic program and school performance drive decisions |

| MPOWER Financing | No score required | 9.99% - 14.99% | $50,000 lifetime | Up to 10 years | Designed for international and DACA students |

| Sallie Mae | 650 suggested minimum | 4.50% - 14.83% | Full attendance cost | 5, 10, or 15 years | Pre-approval for future years available |

| College Ave | 660 suggested minimum | 5.04% - 15.99% | Full attendance cost | 5, 8, 10, or 15 years | Flexible term customization |

| Citizens Bank | 680 suggested minimum | 4.96% - 14.96% | Full attendance cost | 5, 10, or 15 years | Auto-pay enrollment reduces rate 0.25% |

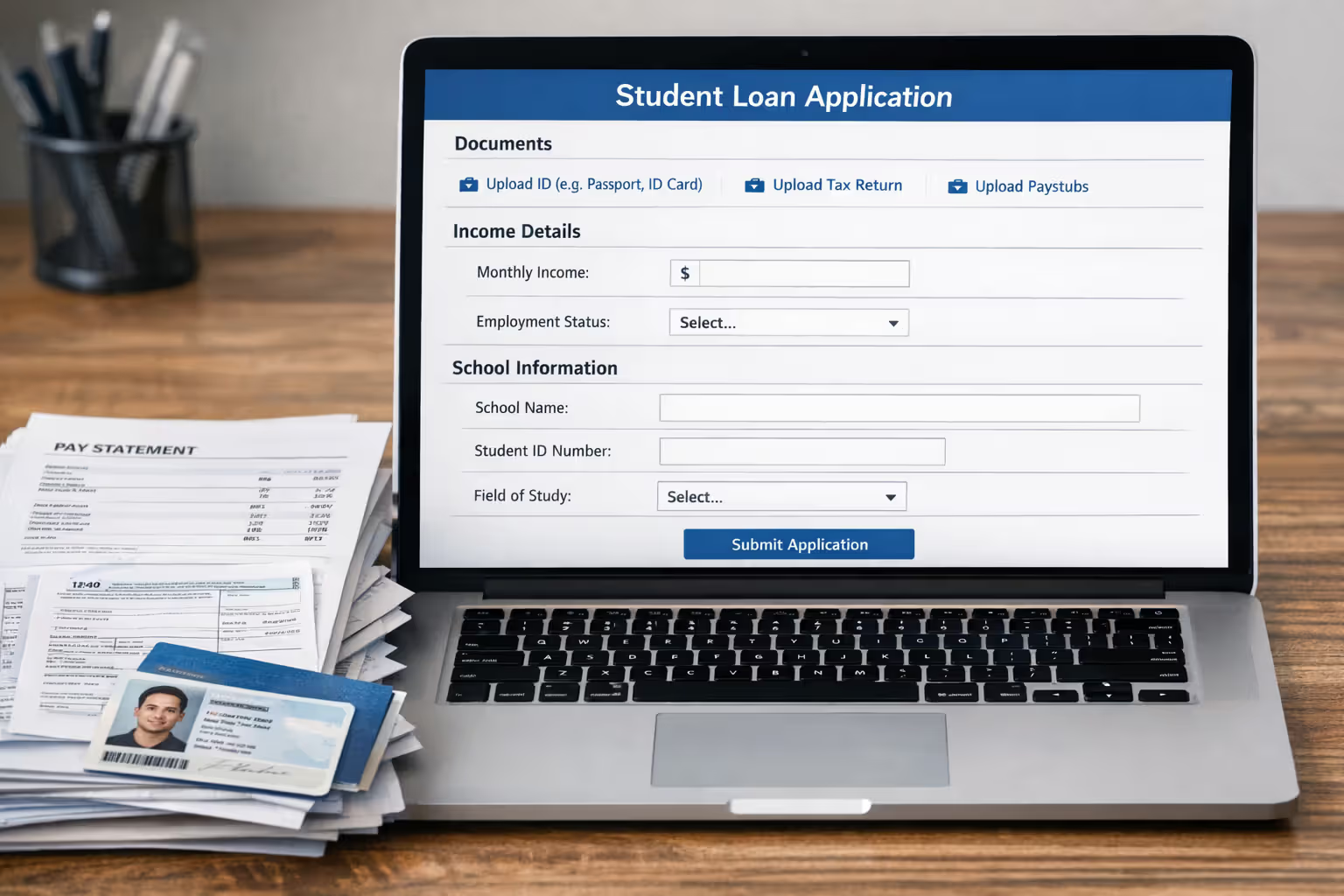

Unlike the FAFSA process where you submit one application for all federal aid consideration, getting a student loan without a cosigner from private lenders means completing separate applications at each company's website. You'll submit documentation including recent pay stubs, previous year's tax returns, enrollment verification from your school, and government-issued identification. Most lenders respond within minutes to several business days with approval decisions.

A critical consideration: private loans lack the flexible repayment options and forgiveness programs attached to federal loans. If you encounter financial hardship, your options are typically limited to forbearance periods (which accrue interest) or refinancing (which requires good credit). Exhaust federal options before pursuing private loans.

Students often underestimate the value of federal loan protections.Income-driven repayment can reduce payments to as low as zero dollars during financial hardship—something no private lender offers. That safety net is worth considering before maximizing private borrowing

— Maria Chen

Building Credit to Qualify Without a Cosigner

If you don't currently meet private lender requirements, strategic credit-building can position you to qualify within 6-12 months. Your FICO score calculation weighs five distinct components: how reliably you've paid bills on time (35% of your score), how much you owe relative to your limits (30%), how long you've maintained accounts (15%), how frequently you've opened new credit (10%), and whether you use diverse credit types (10%).

The secured credit card strategy offers the fastest entry point for students with no existing credit history. These cards function by holding a cash deposit you provide—typically $200 to $500—which the issuer uses as your spending limit. If you put down $300, that becomes your available credit line. Choose cards from Capital One, Discover, or local credit unions that report your activity to Equifax, Experian, and TransUnion without charging annual fees. Use the card monthly for small recurring charges like Netflix or Spotify, then pay the entire balance before the due date arrives.

Becoming an authorized user on a parent's or trusted friend's credit card can accelerate your timeline. When they add your name to a long-standing account with consistent on-time payments and low balance-to-limit ratios, many card issuers report that positive history to your credit file. This strategy carries risk—if the primary cardholder develops late payment patterns, those negatives damage your score too. Verify the card company reports authorized user activity to credit bureaus before implementing this approach.

Credit-builder loan programs, available through credit unions and online platforms like Self, flip traditional lending on its head. Rather than receiving money upfront, you commit to monthly payments (typically $25-$150) that the lender deposits into a restricted savings account. They report your payment behavior to credit bureaus throughout the 12-24 month term. After completing all payments, you receive the accumulated funds minus administrative fees. This essentially converts forced savings into positive credit history.

Payment history matters most, so set up automatic payments for everything reportable—your secured card, credit-builder loan, and any existing bills like utilities or phone service if they report to bureaus. A single 30-day late payment can drop your score 60-100 points and remain on your report for seven years.

Timeline expectations vary by starting point. Someone with no credit history who opens a secured card and becomes an authorized user might reach a 650 score in 6-8 months with perfect payment behavior. Someone recovering from past mistakes like collections or late payments faces a longer road, potentially 12-18 months or more. Check your credit reports free at AnnualCreditReport.com every four months (rotating through the three bureaus) to monitor progress and dispute any errors.

Author: Olivia Harrington;

Source: sonicmusic.net

Alternative Ways to Finance College Without a Cosigner

Loans aren't your only funding source. Combining multiple strategies often reduces borrowing needs significantly.

Scholarships and Grants

Free money should always come first. Federal Pell Grants provide up to $7,395 for eligible undergraduates in the 2025-2026 academic year, determined automatically through your FAFSA. State grants vary widely—California's Cal Grant program offers up to $12,788 for qualifying students, while other states provide more modest amounts.

Private scholarships require more effort but can yield substantial returns. Focus on local opportunities through community foundations, your employer, your parents' employers, and professional associations related to your field of study. These typically have fewer applicants than national scholarships. Websites like Fastweb, Scholarships.com, and your college's financial aid portal aggregate opportunities, but expect to spend 5-10 hours weekly on applications during peak season (January-March for fall enrollment).

Merit-based institutional aid from your college may be negotiable if you have competing offers from similar schools. Financial aid offices sometimes match or improve packages to enroll students they want, particularly if your academic profile sits above their typical admitted student.

Work-Study Programs

Federal Work-Study provides part-time employment for students with financial need, with earnings exempt from financial aid calculations for the following year. Jobs typically pay at least federal minimum wage ($7.25, though many states require higher) and are often on-campus positions like library assistant, research support, or administrative work.

Work-study appears as part of your financial aid package after completing the FAFSA. Unlike loans, you earn money through actual work rather than receiving upfront disbursement. This limits how much you can earn (typically $2,000-$4,000 per academic year) but creates no debt burden.

Employer Tuition Assistance

Many employers offer education benefits, particularly large corporations, healthcare systems, and retail chains. Starbucks, Walmart, Target, Amazon, and UPS all maintain programs covering partial or full tuition at partner institutions. Some programs require you to study in fields relevant to the company, while others allow any degree program.

The trade-off involves working substantial hours while attending school—often 20-30 hours weekly—and potentially limiting your school choices to partner institutions. However, graduating debt-free while gaining work experience can justify these constraints.

Income Share Agreements

ISAs represent a fundamentally different financing model: rather than borrowing a fixed amount, you receive funding in exchange for paying a percentage of your future income for a set period. For example, you might receive $20,000 and agree to pay 8% of your income for seven years after graduation, but only when you earn above $30,000 annually.

The appeal lies in income protection—if you earn below the threshold or face unemployment, you pay nothing during those periods. The risk is that high earners might pay significantly more than they borrowed. Some coding bootcamps and specialized programs offer ISAs, though they're less common for traditional four-year degrees. Read terms carefully, particularly the payment cap (maximum total repayment) and whether periods of low income extend your repayment timeline.

Author: Olivia Harrington;

Source: sonicmusic.net

Common Mistakes When Applying for No-Cosigner Loans

Checking your credit score should happen before you apply anywhere, not after you're denied. Many students assume they have decent credit only to discover a collections account they didn't know existed or that their single credit card has only generated three months of history. Use free services like Credit Karma or your bank's credit score tool to check before starting applications. Hard inquiries from loan applications typically reduce your score by 3-5 points each, so unnecessary applications create real consequences.

Ignoring federal options costs students thousands in unnecessary interest and lost protections. Some borrowers mistakenly believe private loans offer better terms or that the FAFSA only applies to low-income students. Submit your FAFSA regardless of your family's income—many schools require it for merit aid, and you might qualify for unsubsidized loans even without financial need. Federal loans should always fill your funding gap first, up to their annual limits, before considering private alternatives.

Applying to multiple private lenders simultaneously seems efficient but can backfire. Each application generates a hard credit inquiry, and multiple inquiries within a short period signal risk to lenders. Credit scoring models typically count multiple student loan inquiries within a 30-day window as a single inquiry, but lenders may still view numerous recent applications negatively. Apply strategically: prequalify where possible (soft inquiry that doesn't affect your score), then submit formal applications only to your top 2-3 choices.

Missing documentation delays or denies applications unnecessarily. Private lenders typically request proof of enrollment, income verification (pay stubs or tax returns), identification, and sometimes academic transcripts. Gather these documents before starting your application. Incomplete applications often result in automatic denials, forcing you to reapply and generating additional hard inquiries.

Borrowing the maximum offered rather than what you actually need creates unnecessary debt. Just because a lender approves you for $25,000 doesn't mean you should accept the full amount. Calculate your actual gap: tuition plus fees plus room and board plus books, minus scholarships, grants, and federal loans. Borrow only what remains. Every dollar borrowed costs roughly $1.30-$1.60 over a ten-year repayment period at typical interest rates.

FAQ: Student Loans Without a Cosigner

Getting a student loan without a cosigner requires more preparation than traditional borrowing, but it's entirely achievable with the right approach. Start by maximizing federal Direct Loans through the FAFSA—these provide the strongest safety net and never require cosigners for most borrowers. If you need additional funding, evaluate whether your credit profile meets private lender requirements or if spending 6-12 months building credit would position you better.

Remember that borrowing represents only one piece of your financing strategy. Scholarships, grants, work-study, and employer assistance can reduce your loan needs significantly. When you do borrow, choose amounts carefully based on your actual expenses rather than maximum approval amounts.

The independence of securing financing on your own terms comes with responsibility. You alone bear the repayment obligation, so understand your loan terms, interest rates, and monthly payment expectations before signing. But that same independence also means you're building your financial profile, establishing credit history, and developing the money management skills that will serve you long after graduation

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.