Student reviewing an online student loan application at a desk

Do You Need a Cosigner for a Student Loan?

You've filled out loan applications, clicked through disclosure pages, and waited for that approval email. Sometimes it arrives with good news. Other times? The message says you're denied—or worse, approved but with an interest rate that makes your stomach drop.

Here's what often makes the difference: someone else willing to put their credit score and financial reputation on the line for you.

Not everyone needs this extra support. The type of loan you're after matters enormously. So does your credit history (or lack of it), your income, and how much you're trying to borrow. Let's break down when you'll need backup and when you can go it alone.

What Is a Student Loan Cosigner

Think of a cosigner as a financial guarantor who promises to repay your debt if you can't. They're not just writing a recommendation letter or vouching that you're responsible. They're legally binding themselves to your loan by adding their signature to the promissory note.

Lenders evaluate your cosigner's entire financial picture alongside yours. They'll run credit checks on both of you, verify employment for both parties, and analyze how much debt you're each carrying relative to income. Your cosigner brings the creditworthiness you haven't yet established.

Parents handle this role most often, though grandparents, aunts, uncles, or close family friends sometimes step in. The catch? They need to qualify on their own merits. A cosigner drowning in their own debt or carrying recent late payments won't help your application one bit.

Here's what surprises people: cosigning creates identical obligations for both parties. Your cosigner isn't a backup plan lenders contact after giving you a chance to pay. Both credit reports show the loan immediately. When you miss a payment, it damages both credit scores equally. Collections agencies pursue both of you with the same intensity.

Many cosigners sign papers thinking they're just helping with paperwork. Then reality hits when their credit score drops because of someone else's financial struggles.

Author: Olivia Harrington;

Source: sonicmusic.net

When Do You Need a Cosigner for Student Loans

Your need for a cosigner splits sharply based on whether you're borrowing federal or private money. The gap between these two worlds is massive.

Federal vs Private Student Loan Cosigner Requirements

Federal Direct Loans—both subsidized and unsubsidized versions—skip the cosigner requirement entirely. The Department of Education doesn't care about your credit score or whether you've ever held a job. Fill out the FAFSA, enroll at least half-time, and you're eligible. A freshman with pristine credit gets the same terms as one who's never opened a bank account.

Parent PLUS Loans work differently but still don't involve cosigners. Parents borrow these in their own name for their dependent undergraduate children. The Department runs a credit check on the parent, not the student. If the parent gets denied due to negative credit marks, the student can borrow more in unsubsidized loans—still without needing a cosigner.

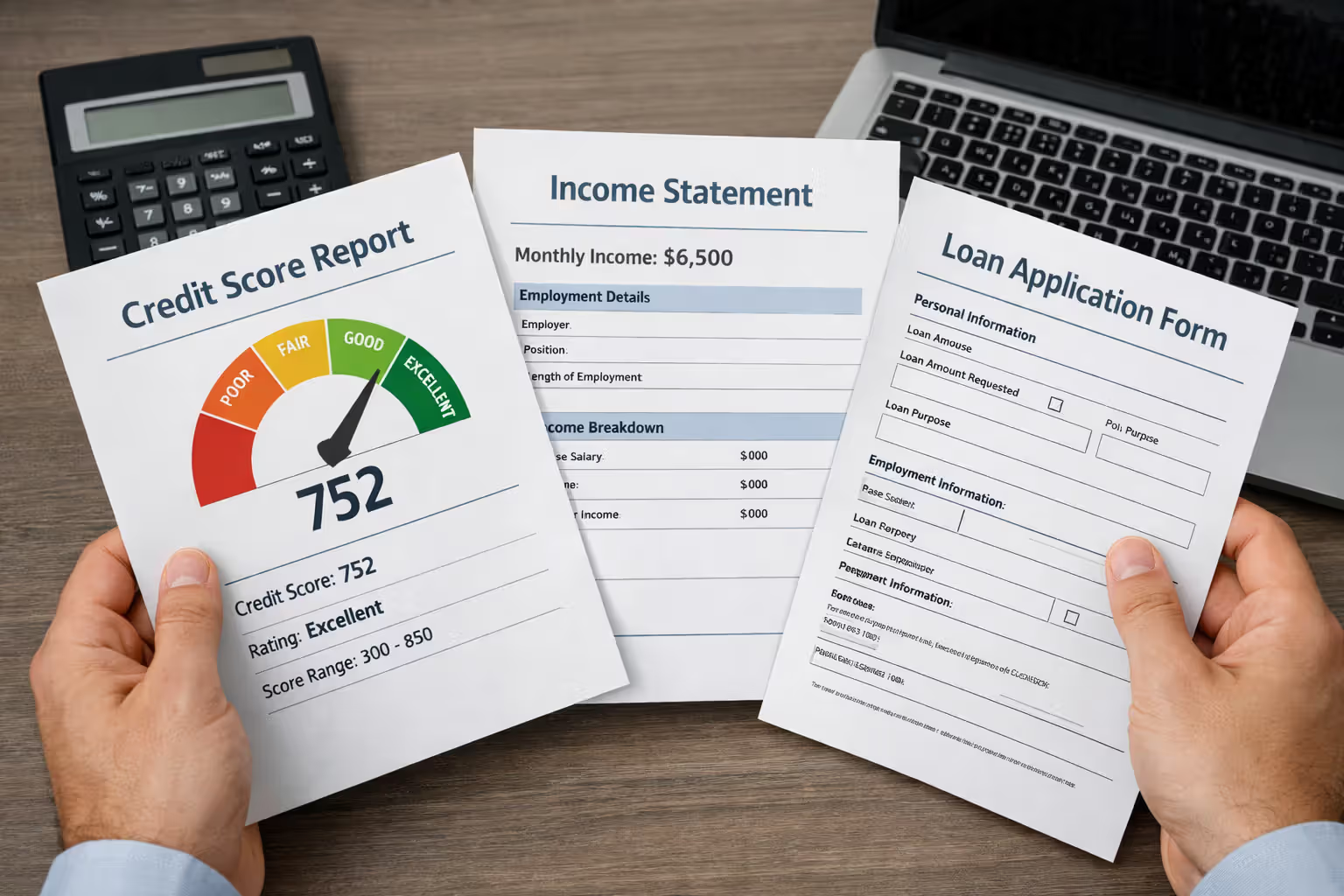

Private lenders flip this script completely. Banks, credit unions, and online lenders treat student loans like any other credit product. They're evaluating risk. Can you repay? They check credit scores, verify income, review employment stability, and calculate existing debt burdens.

Industry data from 2025 shows about 90% of private student loan borrowers bring a cosigner to the table. That percentage dips for graduate students and undergrads in their late twenties who've had years to build credit. Traditional college-age students? They almost never qualify solo.

Credit and Income Thresholds That Trigger Cosigner Needs

Most private lenders draw the line at credit scores around 650, though rates become competitive closer to 700. Students straight from high school face a unique problem: they don't have bad credit—they have no credit file at all. Without at least twelve months of credit history, automated underwriting systems reject applications before a human ever reviews them.

Income presents another hurdle. Lenders commonly want annual earnings at least double your loan amount. Borrowing $15,000? They're looking for $30,000 in documented income. That campus job paying $8,000 a year won't cut it.

Your debt-to-income ratio matters too. Take all monthly debt payments, divide by gross monthly income, and lenders get nervous when that number exceeds 40%. Already making car payments or carrying credit card balances? Adding student loan payments might push you into rejection territory even with decent earnings.

Some students qualify independently. Maybe you've worked full-time since graduating high school. You opened a secured credit card two years ago and never missed a payment. You financed a used car and paid it off. You earn $40,000 annually with minimal debt. That profile works. It's just rare among traditional students.

Author: Olivia Harrington;

Source: sonicmusic.net

Can You Get a Student Loan Without a Cosigner

Absolutely—though your options become more limited, especially in the private loan market. Federal loans remain your strongest no-cosigner option.

Federal Direct Loans let dependent first-year undergraduates borrow up to $5,500. That climbs to $7,500 by junior year. Independent students—anyone over 24, married, in the military, or supporting dependents—can access up to $12,500 annually. Graduate students qualify for up to $20,500 per year. These amounts frequently fall short of total costs, particularly at private colleges, but they come with zero credit requirements.

Building credit before you need private loans opens doors. Open a secured credit card six to twelve months ahead of time. Keep charges under 30% of your limit. Pay the full balance monthly. This creates a credit score where none existed before. Even a modest 670 score paired with part-time work income might push you over approval thresholds.

Some lenders advertise "no cosigner required" student loans, but dig into the requirements. These products typically target graduate students in medicine, dentistry, law, or MBA programs. Underwriters bet on high future earnings. Undergraduates rarely qualify unless they demonstrate substantial employment history.

Income-share agreements present an alternative structure. Instead of traditional loans, you receive education funding in exchange for paying a percentage of future earnings over a set timeframe. No credit checks. No cosigners. But they bring their own complexities around total repayment amounts and how income gets calculated.

Credit unions sometimes bend where big banks won't. If you or a family member holds membership, ask about their student loan programs. Smaller institutions occasionally approve borrowers that national lenders reject, though interest rates might run higher.

Student Loan Cosigner Requirements by Lender Type

Different lenders set different standards for cosigners, but patterns emerge across the industry.

| Lender | Cosigner Credit Floor | Release Option Timeline | What They're Looking For |

| Sallie Mae | Around 670 works; 700+ better | Available following 12 payments made on schedule | Cosigner income must be verifiable; primary borrower needs to show independent repayment capacity later |

| Discover | Low 680s minimum | Student can request release after 12 consecutive payments | Requires completed degree plus passing updated creditworthiness review |

| College Ave | Low 660s accepted | Becomes possible after 24 payments without missed due dates | Fresh credit evaluation for both parties at the time of release request |

| Earnest | Floor around 650 | Release process starts after 12 payments | Income documentation required; borrower might need to refinance or hit income benchmarks |

| Citizens Bank | Low 680s preferred | Longer 36-payment waiting period | Extended timeline but evaluates broader financial circumstances |

These credit minimums represent the absolute floor, not what you should aim for. Cosigners with scores in the 700s boost approval chances dramatically and typically secure lower interest rates. A cosigner carrying a 720 score might shave a full percentage point off your rate compared to someone at 660.

Income verification typically means submitting recent pay stubs, tax returns from the previous year, or several months of bank statements. Self-employed cosigners face tougher scrutiny—lenders want evidence of consistent earnings across multiple years, not just one profitable quarter. Retirees can serve as cosigners using pension payments, Social Security income, or investment distributions, assuming these sources meet minimum requirements.

Debt-to-income calculations apply to cosigners just like primary borrowers. If your parent already juggles a mortgage, car payment, and existing student loans for a sibling, adding your loan could spike their ratio beyond acceptable limits. Most lenders cap DTI at 43% for approval, though some stretch to 50% for applicants with exceptional credit.

Job stability enters the equation too. A cosigner who's bounced between three employers in two years raises concerns, regardless of income level. Lenders prefer seeing two-plus years with one employer, or at minimum, steady work within the same field.

Author: Olivia Harrington;

Source: sonicmusic.net

Cosigner Rules and Responsibilities You Should Know

Cosigning isn't symbolic support—it's a legally enforceable commitment with real consequences.

Primary borrowers and cosigners shoulder equal responsibility. The loan shows up on both credit reports from day one. Make payments on schedule, and both credit scores benefit. Fall 30 days behind, and both scores can plummet by 50 to 100 points.

Lenders don't give the primary borrower a chance to fix problems before involving the cosigner. They report delinquencies to credit bureaus immediately and pursue collection from both parties at once. Cosigners receive payment notices, but by the time they realize something's wrong, credit damage has often already happened.

Serious delinquency brings aggressive collection tactics. Lenders can sue either party for the entire balance. Wage garnishment becomes possible. Bank accounts get levied. Property liens emerge as options. The cosigner's retirement savings and home equity face genuine risk if unpaid debt leads to legal judgments.

The primary borrower's death or permanent disability doesn't automatically free the cosigner. Some lenders discharge loans when the student dies, but others expect the cosigner to continue payments. Disability discharge policies vary dramatically between lenders. Read promissory note fine print covering these scenarios before anyone signs anything.

Cosigner release programs offer an exit, but they're not automatic or easy. Most demand 12 to 36 consecutive on-time payments, proof the primary borrower now meets income and credit standards independently, and sometimes graduation verification. Lenders deny roughly 90% of release applications, frequently citing insufficient income or inadequate credit history for the primary borrower.

Refinancing provides a cleaner exit strategy. Once you've built adequate credit and income, refinancing the loan solely in your name removes the cosigner from all obligation. This route succeeds more often than formal release programs because refinancing lenders actively compete for qualified applicants.

The relationship dynamics deserve honest discussion. Financial conflicts destroy family bonds. When a parent cosigns and you miss payments, holidays become tense. Clear communication about payment ownership, contingency plans for financial emergencies, and regular status updates prevent ugly surprises.

Author: Olivia Harrington;

Source: sonicmusic.net

How to Decide If You Need a Cosigner

Begin with brutal honesty about your financial situation. Pull your credit report from AnnualCreditReport.com to see exactly what lenders will see. No credit score showing up? Private loans will require a cosigner. Score under 650? Same result.

Run your debt-to-income calculation. Add every monthly debt payment—credit cards, car loans, existing student loans. Divide that total by your gross monthly income. Over 40%? Lenders want someone else on the hook.

Think about how much you're borrowing. If federal loans cover 80% of costs and you need just $3,000 from private sources, some lenders show more flexibility. Trying to borrow $30,000 privately with minimal credit history? Not happening without help.

Evaluate your potential cosigner's financial health. If your parent is nearing retirement, carrying significant existing debt, or has borderline credit themselves, asking them to cosign creates mutual risk. A cosigner with a 680 score and high debt load might not strengthen your application enough to justify putting them on the hook.

Consider the relationship implications carefully. Can you handle the psychological pressure of knowing your mistakes damage someone else's credit? Can they avoid micromanaging your spending once they're legally responsible? Some families navigate this smoothly. Others create lasting resentment.

Students frequently treat cosigners like a quick fix to access borrowed funds, but the decision deserves careful conversation about worst-case scenarios.I recommend families create written agreements spelling out payment responsibility, communication expectations, and backup plans if job loss occurs. Your loan servicer won't care about verbal understandings—only whose signatures appear on the promissory note

— Michael Torres

Explore alternatives before committing to a cosigned loan. Could you attend a less expensive institution where federal loans cover more ground? Could you work for a year to build credit and savings before borrowing? Could you enroll part-time while working more hours, spreading education costs across additional years?

The tradeoff between borrowing now versus delaying education isn't straightforward. Graduating a year later costs you a year of career earnings, potentially outweighing the benefit of avoiding cosigned debt. But graduating with crushing debt and a fractured relationship with your cosigner carries steep costs too.

Frequently Asked Questions About Student Loan Cosigners

Whether you need a cosigner boils down to two factors: which type of loan you're pursuing and your current financial profile. Federal loans eliminate the question entirely—no credit evaluation, no income verification, no cosigner necessary. Private loans, which bridge the gap when federal borrowing limits fall short, almost always demand cosigners for students with thin credit files.

If you need a cosigner, have transparent conversations about risks and obligations. Both parties should understand the credit implications, the challenges of getting released from the loan, and the relationship dynamics at stake. Written agreements clarifying payment responsibility and communication expectations head off misunderstandings before they create problems.

Building credit early expands your options considerably. A year of responsible credit card management before you need private loans could mean the difference between borrowing independently and needing assistance. Even if you start with a cosigner, focus on your exit strategy—making consistent payments and developing the credit profile necessary for eventual release or refinancing.

College financing paths vary dramatically between students. Federal loans form your foundation, cosigners bridge gaps when necessary, and careful planning minimizes both debt burdens and relationship stress. Understanding when and why cosigners become necessary empowers you to make informed decisions rather than panicked ones when application deadlines arrive.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.