Student reviewing college loan documents and online financial aid application

How to Apply for Student Loans?

Planning to pay for college? You'll probably need to start working on loan applications at least six months before your first semester begins—maybe even earlier if you want to maximize state grant money. Between 60-70% of college students graduate with some loan debt, and most piece together funding from multiple sources: federal loans, private lenders, scholarships, family contributions, and part-time work.

Here's what trips people up: federal and private loan applications work completely differently. Federal loans need one government form. Private loans? You'll fill out separate applications for each bank or lender you approach. Mix up the deadlines or forget a required document, and you might find yourself unable to pay your tuition bill when August rolls around.

The government's loan program offers better deals for most people—interest rates that don't change, repayment plans that adjust based on your income, and sometimes loan forgiveness if you work in public service. Private lenders step in when government loans don't cover your full costs, but you'll face credit checks, possibly higher rates that fluctuate over time, and fewer safety nets if you hit financial trouble later.

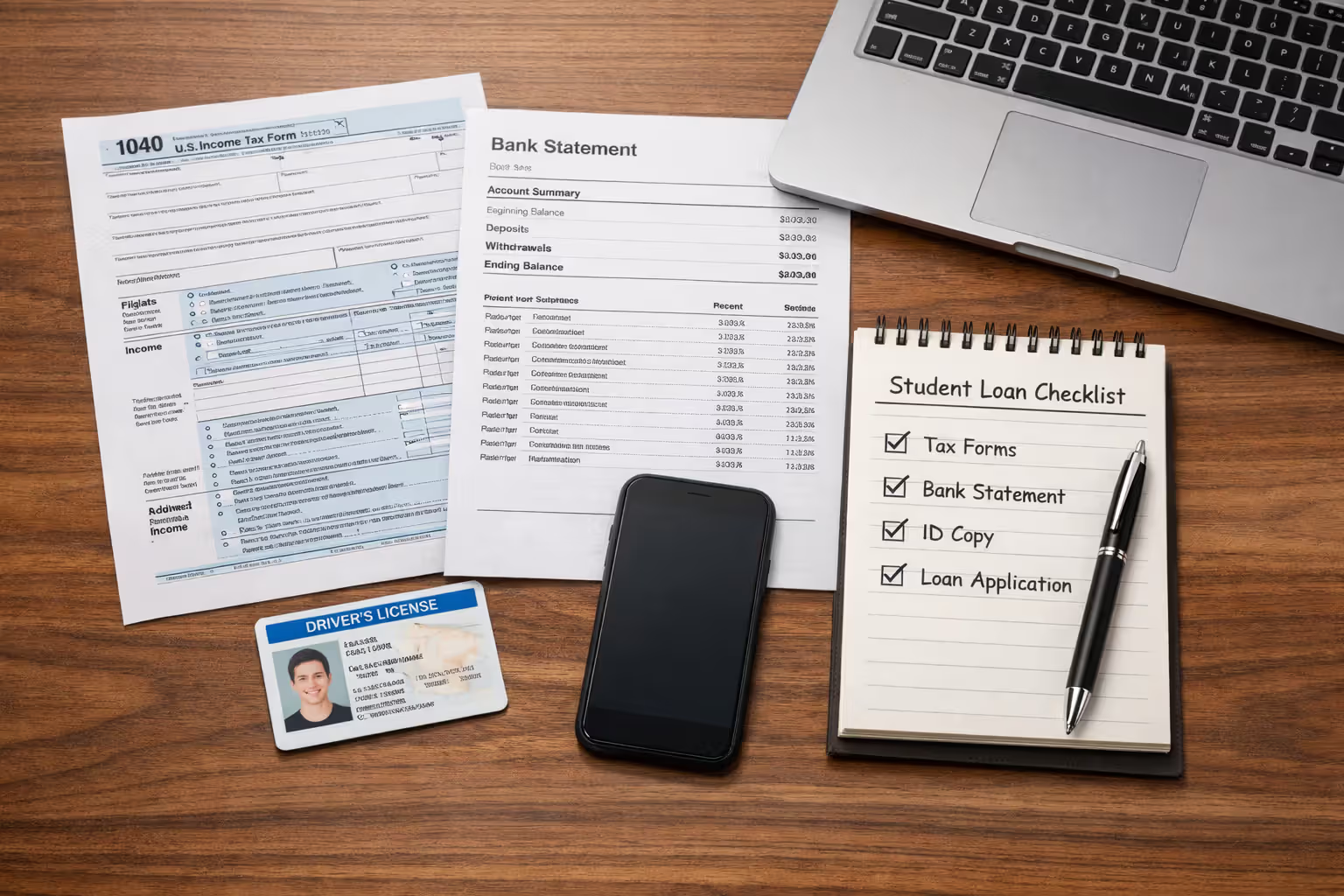

Getting organized now prevents headaches later. You'll need tax forms, bank statements, school codes, and Social Security numbers. Missing even one piece of information can delay everything by weeks.

Understanding Your Student Loan Options

The federal Direct Loan program splits into two categories: Subsidized and Unsubsidized. Here's the practical difference. With a subsidized loan, the government covers your interest charges while you're taking at least six credit hours per semester. Only undergrads with demonstrated financial need can get these—the FAFSA form determines if you qualify.

Author: Danielle Pierce;

Source: sonicmusic.net

Unsubsidized loans? Anyone can get them—undergrads, graduate students, professional degree students. But interest starts piling up the day your school receives the money, even while you're still enrolled. That interest capitalizes (gets added to your principal balance) when you enter repayment, which means you'll pay interest on interest. A $10,000 unsubsidized loan taken freshman year will actually cost you closer to $12,500 by graduation if you don't make payments while in school.

PLUS loans create another option—one for parents of dependent undergrads, and another for graduate students. The government checks your credit history for these. If you have significant negative marks (defaults, bankruptcy, foreclosure), you won't qualify without an endorser. PLUS loans charge higher interest than Direct Loans (currently 8.05% versus 5.50% for undergraduate Direct Loans), but they let you borrow right up to your school's full cost of attendance after subtracting other aid.

Banks, credit unions, and online companies provide private student loans. Each one examines your credit score (or your cosigner's) and sets rates accordingly. One lender might quote you 6% fixed, another might offer 4.5% variable that could climb to 12% in five years. Unlike federal loans, private ones rarely include options to pause payments during unemployment or cap payments at 10% of your income.

Here's the strategy most financial advisors recommend: max out federal loans first, then shop for private loans only if needed. Why? Direct Loans from the government don't care about your credit history (except for PLUS loans). You can postpone payments during hardship without ruining your credit. Income-driven plans can reduce your monthly bill to 5-10% of your discretionary income. And certain public service jobs can lead to complete forgiveness after 10 years of payments.

Where you submit applications depends entirely on loan type. Federal loans all run through one place: you file a FAFSA through the Department of Education's website. For private loans, you'll directly contact individual lenders—and comparing offers from five different companies isn't excessive. Rate differences of even half a percentage point will cost or save you thousands over 10 years.

Before You Apply: What You'll Need

The FAFSA demands quite a bit of financial documentation. Start gathering these items at least two weeks before you plan to submit:

Students and contributing parents both need: - Social Security numbers (the student's plus any parent who's providing financial information) - Tax returns from two years ago—if you're applying for 2026-2027 aid, you'll report your taxes - All W-2 forms from that year - Documentation of untaxed income: child support payments you received, workers' compensation, interest income from savings accounts - Your current checking and savings account balances (check the day you file) - Investment values for stocks, bonds, mutual funds, money market accounts, and real estate beyond your primary home (retirement accounts like 401(k)s don't count)

Students also specifically need: - Driver's license if you've got one - Your Alien Registration Number if you're not a citizen - A list of schools with their six-digit federal school codes—search for these at fafsa.gov

That "prior-prior year" tax setup confuses people initially. The government implemented it so families can file the FAFSA earlier using tax information they've already completed. Instead of waiting until April to file taxes for the current year, you'll reference old taxes that are already done.

Dependent students—that's most undergraduates under 24 who aren't married, don't have kids, and haven't served in the military—need a parent to share financial details as a "contributor." Independent students only report their own finances, plus their spouse's if married.

Here's something critical that costs people money every year: states and colleges set priority deadlines that come way before the federal June 30 cutoff. Illinois, for example, requires FAFSA submission by October 1 for priority consideration of state grants. California's deadline hits March 2. Some states distribute grant money first-come, first-served until funds run out. Miss your state's deadline by one day and you could lose $5,000 in grants.

Private loan applications need different paperwork: - Your college acceptance letter or proof you're currently enrolled - A cost of attendance breakdown from your school's financial aid office (they'll email you this) - Government ID like a driver's license or passport - Proof you (or your cosigner) earn income: recent pay stubs, last year's tax return - A complete list of scholarships, grants, and federal loans you're receiving

Author: Danielle Pierce;

Source: sonicmusic.net

Step-by-Step Federal Student Loan Application Process

Everything federal starts with the FAFSA, which tells the government and your school what aid you qualify for—grants, work-study programs, and federal loans. Schools build your financial aid package based on what the FAFSA reveals about your finances.

Creating Your FSA ID

You can't submit anything until you have an FSA ID—think of it as your digital signature for federal student aid documents. Head to StudentAid.gov and click the account creation link. The system will ask for:

- Your Social Security number

- Your full legal name exactly matching your Social Security card (middle names matter)

- Your birth date

- An email you actually check daily

- Your cell number

- Answers to security questions

- Your chosen username and password

If your parents need to sign your FAFSA (they will if you're a dependent student), they must create their own separate FSA ID. Don't ever share login credentials—this ID legally signs documents worth tens of thousands of dollars.

Sometimes the system will verify your identity by pulling questions from your credit report—things like "Which of these streets have you lived on?" If online verification fails, you'll print a signature page, physically sign it, and mail it in. That delays your FAFSA processing by 10-14 days minimum.

Completing the FAFSA Form

Sign into StudentAid.gov and look for the current year's FAFSA form. You'll move through sections covering basic demographics, your school list (up to 10 schools can receive your information), whether you're dependent or independent, how many people live in your household, and all that financial data you gathered.

Watch for the IRS Data Retrieval Tool when you hit the income section. This feature connects directly to IRS computers and imports your tax information automatically. Using it cuts down on errors and often prevents your school from demanding extra verification documents later. If you filed jointly with a spouse, the tool imports all income from your joint return.

You might not be able to use the retrieval tool in certain situations—if you filed an amended return, got married recently, or your parents are married but filed separately. In those cases, you'll manually type in numbers from your tax forms. Keep those 1040s next to your keyboard and double-check every figure. A transposed number can throw off your aid by thousands or trigger verification requests.

The Department of Education shortened the 2026-2027 FAFSA significantly compared to previous years. You'll answer fewer questions, though the core financial information hasn't changed much.

Review everything before hitting submit. The confirmation page shows which schools will receive your data. Save this confirmation or screenshot it.

Reviewing Your Student Aid Report

Your Student Aid Report arrives three days to three weeks after submission. This multi-page document recaps everything you told the government and displays your Student Aid Index—the SAI, which replaced the old Expected Family Contribution term.

Your SAI represents what the federal calculation determines your family can afford for college. Schools calculate your financial need with simple math: their cost of attendance minus your SAI equals your need. A school costing $35,000 with an SAI of $10,000 means you have $25,000 in financial need.

Scan your SAR carefully for mistakes. Catch an error? Log back into the FAFSA site and make corrections. Certain mistakes dramatically affect your aid—reporting yourself as dependent when you actually meet independent criteria, or vice versa, for instance.

Your SAR might flag you for verification—a process where your school confirms your FAFSA information's accuracy. Roughly one out of every three FAFSAs gets selected. If yours is, your financial aid office will email you requesting documents like IRS tax transcripts, verification worksheets, or proof of untaxed income. Respond within a week to avoid losing aid.

How to Apply for Private Student Loans

Only turn to private lenders after accepting all available federal aid. Private loans should bridge whatever gap remains between your total costs and everything else: scholarships, grants, federal loans, family money, and what you can earn from a campus job.

Calculate your precise borrowing need first. Start with total cost of attendance—your school lists this figure on their website, and it includes tuition, fees, room, board, books, supplies, transportation, and personal expenses. Now subtract: - Every scholarship and grant you've received - Federal loans you've accepted - Money your family will contribute this year - Realistic work-study earnings (if you're certain you'll work enough hours)

What's left is your private loan need. Don't borrow extra for spring break trips or a nicer apartment. Every additional $1,000 you borrow will actually cost you $1,300-$1,500 after 10 years of payments with interest.

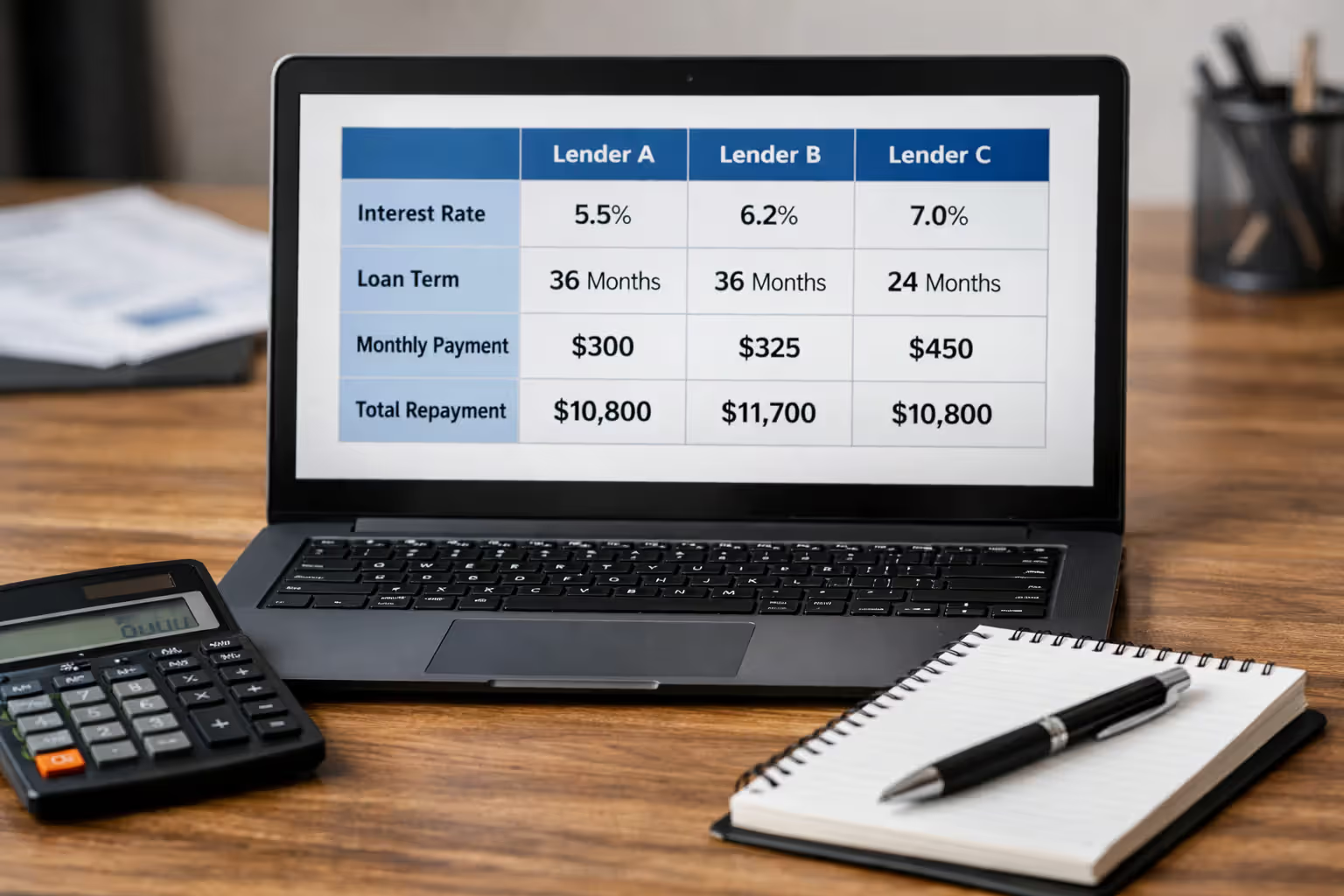

Compare lenders across these factors: - Interest rates—fixed rates stay the same for 10-15 years; variable rates change quarterly based on market indexes - Origination fees—some companies charge 1-5% upfront, others charge nothing - Repayment term length—5, 10, 15, or 20 years, with longer terms meaning lower monthly payments but much higher total interest - Cosigner release policies—can you remove your cosigner after 24-36 consecutive on-time payments? - In-school deferment—will they let you postpone payments until six months after graduation? - Hardship forbearance—what happens if you lose your job and can't pay?

Most undergrads need a cosigner—usually a parent or other relative with solid credit (typically 670+ score) and steady income. Your cosigner becomes equally legally responsible. If you miss payments, their credit suffers and the lender can pursue them for repayment.

Get rate quotes from at least three to five lenders. Many allow "soft" credit checks that don't affect your credit score while shopping. Once you've got actual offers in hand, calculate total repayment cost over the full loan term, not just the monthly payment. A $20,000 loan at 6% fixed over 10 years costs $26,645 total. The same loan at 8% costs $29,147—a $2,502 difference.

Author: Danielle Pierce;

Source: sonicmusic.net

Here's what the private loan application process typically looks like: 1. Fill out an online application with your contact info, income, housing costs, and employment details 2. Enter your school's name and how much you need to borrow 3. Add your cosigner's information if required—they'll complete their section of the application 4. Upload requested documents: enrollment verification, your ID, proof of income 5. Review loan terms carefully and electronically sign the agreement

Lenders transfer approved funds directly to your school. The school certifies the amount first—they verify you're not borrowing beyond your cost of attendance minus other aid. This certification process takes one to three weeks.

Common Mistakes When Applying for Student Loans

Blowing past priority deadlines: The federal FAFSA accepts applications through June 30 for each academic year, but most states and schools enforce earlier deadlines—sometimes as early as February. Missing these priority dates won't disqualify you from federal loans, but state grants and school-based aid often get distributed first-come, first-served. Create a spreadsheet listing every relevant deadline when you start this process.

Failing to compare aid packages properly: Multiple college acceptances? Compare the net price—not the sticker price. A private school charging $60,000 might offer you $35,000 in grants and scholarships, making your net cost $25,000. A public school charging $30,000 might only offer $5,000 in grants, costing you $25,000 net—the same price. Also look at how much of each package consists of loans. You're never required to accept offered loans.

Accepting maximum loan amounts: Loan approval for $12,500 doesn't mean you should borrow all $12,500. Calculate expected monthly payments using online calculators. A useful guideline: keep your total student debt below your anticipated first-year salary. Majoring in social work with a likely starting salary of $40,000? Try to limit total borrowing to $40,000 or less. That makes repayment much more manageable.

Rushing through entrance counseling: First-time federal loan borrowers complete required entrance counseling before receiving funds. This isn't busywork—the session explains your responsibilities, repayment options, interest rates, and default consequences. Read carefully instead of clicking through just to finish.

Confusing loan types: Parent PLUS loans belong to your parents—not you. They're legally responsible for repayment. Some families don't realize this until years later when the parent can't make payments and expects their graduate to take over. Similarly, accepting unsubsidized loans when you qualify for subsidized loans costs you thousands in accumulated interest.

Jumping to private loans prematurely: Federal loan protections—income-based repayment, potential Public Service Loan Forgiveness, generous deferment policies—don't exist with private lenders. Always exhaust federal borrowing before contacting banks.

After You Apply: Next Steps and Loan Disbursement

Your school receives your FAFSA results and sends an award letter within a few weeks of accepting you. This letter breaks down your complete aid package: federal and state grants, institutional scholarships, work-study eligibility, and offered loans.

You must formally respond to each component—accepting, declining, or reducing amounts. If you only need $5,000 but they offered $8,500, request the lower amount. Log into your school's financial aid portal to submit your decisions. Some schools impose response deadlines; miss them and they'll withdraw the offer.

Federal loan first-timers complete two additional requirements:

Entrance counseling: Takes about 30 minutes at StudentAid.gov. The session covers loan basics, realistic budgeting, all available repayment plans, and borrower responsibilities. You can pause and return later, but your school can't disburse any funds until you finish.

Master Promissory Note: This legal contract outlines loan terms and your repayment promise. Sign it electronically at StudentAid.gov using your FSA ID. One MPN typically covers all loans you receive over 10 years at the same institution, so you usually only sign once.

Schools must split annual loan amounts across at least two disbursements—typically one per semester or quarter. Money goes directly to your student account, covering tuition, mandatory fees, and school-billed housing and meals first. If loan funds exceed your school charges, you'll receive the remaining amount as a refund within 14 days. That refund covers books, off-campus rent, transportation, and other costs.

Disbursement timing varies by school, but most process refunds within the first two weeks of each term. Don't count on refund money to pay September rent if you need it August 1—timing might not work.

Track your federal loan disbursements through the National Student Loan Data System at nslds.ed.gov. This database displays all your federal aid: loan amounts, disbursement dates, current servicer handling your account, and outstanding balances.

Private lenders send funds to your school after you complete the application and the school certifies your loan amount. Processing typically takes two to four weeks, so apply well before payment deadlines. Like federal loans, private money pays school charges first, then you receive remaining amounts.

The biggest mistake I see students make is treating student loans like free money.Every dollar you borrow today is a dollar you'll repay with interest, often for a decade or more. I always advise students to work part-time if possible, live frugally, and borrow only what they absolutely need to complete their degree

— Michael Chen

Federal vs. Private Student Loans Comparison

| Feature | Federal Loans | Private Loans |

| Interest rates | Fixed rates set annually by Congress; identical for all borrowers within the same loan category | Fixed or variable rates determined by your credit profile; rates vary significantly between lenders and individual borrowers |

| Application process | One FAFSA form provides access to all federal student aid programs | Individual applications required for each lender you're considering |

| Credit requirements | No credit check needed for Direct Subsidized and Unsubsidized Loans; credit review required only for PLUS loans | Credit check mandatory for all applicants; most undergraduates require creditworthy cosigners |

| Repayment options | Multiple plans available: standard 10-year, graduated, extended 25-year, and four income-driven options; Public Service Loan Forgiveness available | Generally limited to standard or extended repayment; few flexible alternatives during financial hardship |

| Loan limits | Annual caps range from $5,500 to $12,500 yearly for dependent undergraduates based on grade level; aggregate lifetime limits also apply | Lenders typically approve up to full cost of attendance minus all other financial aid received |

| Cosigner requirements | Never required for Direct Loans; PLUS loans require parent or graduate student borrower to pass credit evaluation | Most undergraduate borrowers need cosigners; some lenders permit cosigner removal after 24-36 on-time payments |

Frequently Asked Questions About Student Loan Applications

Student loan applications involve multiple stages that differ dramatically between federal and private funding sources. Begin with the FAFSA to access federal loans—these deliver superior terms and more flexible repayment structures for the vast majority of borrowers. Submit the application early, organize required documents in advance, and watch state and institutional priority deadlines closely to capture maximum aid eligibility.

Turn to private lenders only after exhausting available federal aid. Get quotes from multiple companies, understand complete borrowing costs, and resist taking more than you genuinely need. Your post-graduation self will thank you when monthly payments begin six months after your final semester.

The application process demands attention to detail and proactive timing, but dividing it into discrete steps makes everything less overwhelming. Build a timeline marking specific deadlines, organize your paperwork systematically, and contact your school's financial aid office whenever questions arise. They exist to guide you through the process and help you make informed borrowing choices that support educational goals without creating crushing debt.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.