International student on a U.S. university campus holding documents

Can International Students Get Student Loans?

Studying in the United States costs serious money—we're talking $25,000 to $55,000 per year at most colleges and universities. If you're an international student, you've probably already discovered that the financial aid system here works completely differently than what domestic students deal with. While American citizens can fill out one form and access billions in federal aid, international students face a frustrating reality: most of those government programs are off-limits.

So what options actually exist? And more importantly, which lenders will say yes to someone on an F-1 visa? Let's break down exactly how international students can (and can't) borrow money for their U.S. education.

Federal Student Loan Eligibility for International Students

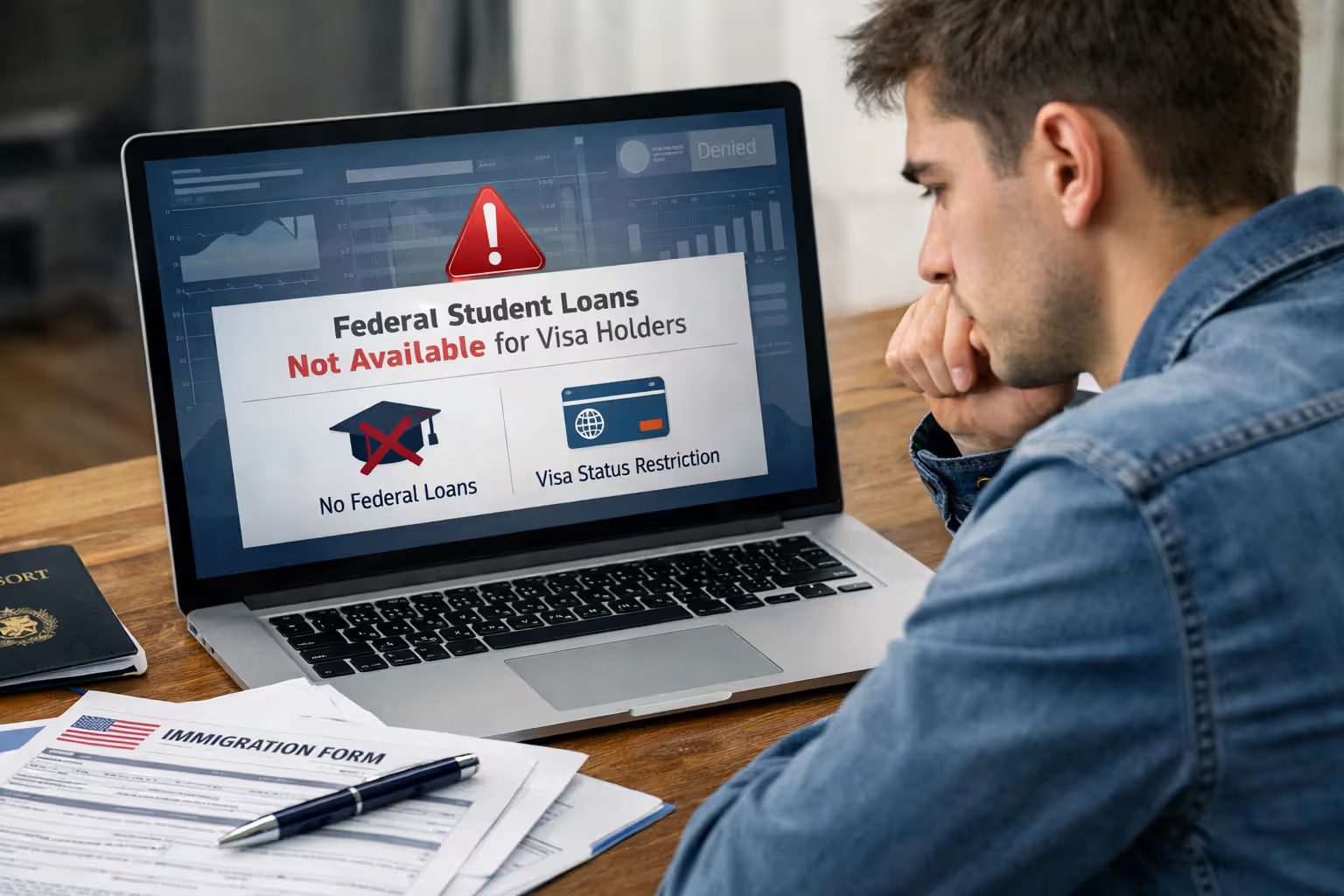

Here's the disappointing news first: the U.S. Department of Education runs the Direct Loan Program, and if you're on a student visa, you're not getting in. The government restricts these loans to citizens, nationals, and what they call "eligible noncitizens."

Can a noncitizen get a student loan through federal programs? Only if your immigration status fits very specific categories. Green card holders qualify immediately. So do T-visa holders (people who've been victims of human trafficking) and certain refugees or asylum seekers. You'll need documentation like an I-551, I-151, or I-551C card—basically proof of permanent residence or qualifying humanitarian status.

If you're here on an F-1, J-1, or M-1 visa, you're out of luck with federal loans. Period. Doesn't matter if you've been here since freshman year of high school or if you're graduating summa cum laude. Your visa type alone disqualifies you.

The FAFSA form—that's the Free Application for Federal Student Aid—acts as the starting point for all federal education money. Without FAFSA access, you can't touch Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans, Pell Grants, or federal work-study positions. International students on temporary visas simply can't submit a valid FAFSA application.

Student loan rules for international students at the federal level have virtually no flexibility. Some students think that because they've lived here for years, or because they have siblings who are citizens, they might squeeze through. They can't. Others believe that qualifying for in-state tuition at a public university somehow translates to federal aid eligibility. It doesn't—these are completely separate determinations with totally different criteria.

One particularly frustrating misconception: establishing state residency for tuition purposes does absolutely nothing for your federal loan eligibility. States set their own residency rules for tuition discounts, but federal aid eligibility depends solely on citizenship or specific protected immigration categories.

Author: Marcus Bennett;

Source: sonicmusic.net

Private Student Loans for International Students

Since the government won't help, private lenders have stepped in—though they'll cost you more and demand more paperwork. These loans come from regular banks, credit unions, and specialized education finance companies instead of Uncle Sam.

Are international students eligible for student loans from private sources? Yes, but nearly all of them insist on one thing: a U.S. cosigner with solid credit. This cosigner isn't just vouching for you—they're equally responsible for every payment. If you ghost on your loan obligations, your cosigner's credit score tanks right alongside yours.

Current interest rates for international student loans run anywhere from 4.5% up to 14%, depending mainly on your cosigner's financial profile. Engineering and business majors at highly-ranked schools typically score better rates than liberal arts students at lesser-known institutions. Lenders openly acknowledge they're betting on your future earning potential.

Here's what you won't get with private loans: the safety nets built into federal programs. There's no income-driven repayment if your salary disappoints. You can't qualify for Public Service Loan Forgiveness. The generous forbearance options federal borrowers enjoy? Not available. You're locked into fixed repayment schedules lasting 5 to 15 years, starting shortly after graduation or when you drop below half-time enrollment.

Top Lenders Offering International Student Loans

A handful of financial institutions have built dedicated programs for international students:

Sallie Mae works with select universities to offer International Student Loans. You'll need that creditworthy U.S. cosigner—someone who's a citizen or permanent resident with provable income and clean credit history. They'll lend up to your total cost of attendance minus whatever other aid you've scraped together.

Discover Student Loans says yes to international applicants who bring along a qualified U.S. cosigner. Their rates compete favorably if you're attending an approved school, and they throw in a 1% cash reward when you graduate—assuming you haven't missed payments along the way.

Citizens Bank covers up to 100% of your school-certified costs through their international student program. Cosigners are mandatory. One interesting feature: their Multi-Year Approval lets you lock in funding for multiple years with one application, though they reserve the right to adjust rates annually.

MPOWER Financing and Prodigy Finance operate differently than traditional banks. They've built alternative evaluation methods that sometimes benefit students who lack U.S. connections but attend partner institutions.

Cosigner Requirements and Alternatives

Finding someone who qualifies as a cosigner creates the biggest roadblock. Your cosigner needs steady income—usually at least $24,000 yearly—plus a credit score above 670 and a debt-to-income ratio under 43%. Your parents back home, no matter how wealthy, can't cosign unless they're U.S. citizens or permanent residents.

Some lucky students have aunts, uncles, or family friends who immigrated to America and are willing to help. This requires enormous trust, since cosigners carry full legal liability if you default—we're talking the entire loan balance plus collection costs.

A few lenders dangle the possibility of cosigner release: make 24 to 36 consecutive on-time payments, meet their income requirements, and you might be able to release your cosigner from the obligation. But approval isn't automatic, and lenders regularly deny these release requests even when borrowers meet the basic criteria.

Author: Marcus Bennett;

Source: sonicmusic.net

No-Cosigner International Student Loan Options

A small number of lenders have figured out how to evaluate creditworthiness without requiring a U.S.-based guarantor. The trade-off? Much stricter limitations on who qualifies.

MPOWER Financing looks beyond credit scores entirely. They weigh your grades, your career prospects in your chosen major, and your school's reputation. They serve students from over 200 countries, but only at roughly 400 approved U.S. schools. Undergrads can typically borrow $2,000 to $50,000; graduate students might access up to $100,000.

Prodigy Finance targets graduate students in specific fields: business, engineering, law, public policy, and health sciences. Their model assesses your likely future salary instead of your current credit file. They fund students at top-ranked universities where employment data is well-documented. Interest rates run 6% to 12%, varying by program and institution.

Ascent offers cosigner-free loans to upperclassmen and graduate students who clear specific hurdles: enrollment at an approved school, satisfactory academic progress, and expected graduation within 12 months. International students need valid visa documentation and a realistic path to post-graduation employment.

Can international students get student loans explained in simpler terms? Yes, but without a cosigner, you're trading one requirement for several others. These lenders restrict loans to specific schools, specific degree programs, and students with strong profiles. If you're attending a newer institution or pursuing a degree with uncertain job prospects, you probably won't qualify.

Loan caps run lower too. You might get approval for $15,000 annually without a cosigner versus $40,000 with one. That gap means you'll need scholarships, savings, or other funding sources to cover the difference.

Author: Marcus Bennett;

Source: sonicmusic.net

International Student Loan Eligibility Requirements

Beyond the cosigner situation, several baseline criteria apply almost universally across private lenders.

Visa status matters immediately. F-1 visa holders represent the largest eligible group. J-1 exchange visitors might qualify if their specific program allows private borrowing. M-1 vocational students find fewer options. Tourist visas (B-1/B-2) or dependent visas (F-2, J-2) typically disqualify you as a primary borrower.

Enrollment verification means you must be accepted and enrolled at least half-time in a degree program at an approved school. Certificate programs won't cut it. Neither will English language institutes or non-degree coursework. Your school's financial aid office must certify both your cost of attendance and any other financial assistance you're receiving.

Credit history considerations vary wildly between lenders. Some will examine credit reports from your home country. Others care exclusively about U.S. credit history. If you lack U.S. credit and you're applying with a cosigner, that's usually fine—the cosigner's credit carries more weight. But no-cosigner programs demand some proof that you're financially responsible.

School certification represents a step you can't skip. Lenders maintain approved school lists, generally featuring regionally accredited universities and colleges with solid track records. Brand-new schools or unaccredited institutions rarely make the cut. Check whether your specific school appears on a lender's approved list before wasting time on an application.

Income or cosigner financial requirements ensure someone can actually repay the debt. With cosigned loans, the cosigner's finances matter most. With no-cosigner options, lenders evaluate factors like your academic major, your expected graduation date, and the typical starting salaries for graduates from your program at your institution.

How to Apply for Student Loans as an International Student

The application process demands careful planning, especially since you can't fall back on federal aid if private loans fall through.

Author: Marcus Bennett;

Source: sonicmusic.net

Step 1: Research lender options and requirements. Don't settle for the first lender you find. Compare at least three to five options, examining not just interest rates but also fees, repayment flexibility, and eligibility standards. Verify that your school appears on each lender's approved institution list. Start this research six to eight months before you need the money.

Step 2: Identify potential cosigners if required. Have honest conversations with anyone you're considering asking. Make sure they understand they're not just signing a character reference—they're committing to repay the full amount if you can't or don't. Share detailed information about loan terms, monthly payment amounts, and what happens in default scenarios. If nobody can or will cosign, shift your focus to no-cosigner lenders and alternative funding.

Step 3: Gather required documentation. You'll need your passport, visa paperwork, I-20 or DS-2019 form, proof of enrollment, school cost of attendance information, and documentation of any other financial resources you're bringing to the table. Cosigners need to provide Social Security numbers, income verification, and current employment details.

Step 4: Complete the application. Most lenders use online applications that take 15 to 30 minutes. Provide accurate information about your degree program, anticipated graduation date, and how much you need to borrow. Here's a tip: request slightly less than you think you need rather than more. You can usually request additional funds later, but overborrowing creates unnecessary debt.

Step 5: Submit for school certification. After preliminary approval, the lender contacts your school's financial aid office. They verify your enrollment status, confirm the cost of attendance, and report any other aid you're receiving. This step alone can consume one to three weeks, so factor this timeline into your planning.

Step 6: Review and sign loan documents. When you receive final loan terms, read everything carefully. Scrutinize the interest rate, repayment schedule, origination fees, and any provisions for cosigner release. If anything seems confusing or concerning, ask for clarification before signing anything.

Step 7: Receive funds. Lenders send money directly to your school, which applies it first to tuition and mandatory fees. Whatever's left gets refunded to you for housing, books, and living expenses. This typically happens one to two weeks before the semester starts.

Timeline considerations: From application to actual funding, expect four to eight weeks. Start applications at least two months before tuition deadlines unless you enjoy late fees and registration cancellations.

Alternative Financing Options for International Students

I've watched too many students sign loan agreements without calculating what their monthly payments will actually be after graduation. They don't consider exchange rates, or how difficult it might be to earn U.S. dollars while working in their home country. Before borrowing a penny, calculate your realistic starting salary and figure out whether you can actually afford the monthly payments on that income

— Maria Chen

Smart students don't rely on loans alone. Diversifying your funding sources reduces how much you'll owe later.

Scholarships and grants represent free money you never have to repay. Plenty of universities offer merit-based scholarships designed specifically for international students, though you'll compete against thousands of other applicants for limited awards. EducationUSA maintains searchable databases of scholarship opportunities. Country-specific programs—like Fulbright or government scholarships from your home country—provide substantial funding if you qualify.

Institutional aid comes straight from universities. Schools with large endowments sometimes offer need-based aid to international students, though policies vary dramatically between institutions. Private universities often prove more generous than public schools. Before accepting admission anywhere, ask the financial aid office directly what funding they offer international students.

Home country loans provide another avenue worth exploring. Banks and government programs in your home country might offer education loans for study abroad. These sometimes feature more favorable terms than U.S. private loans and allow repayment in your local currency—though you're still taking on debt either way.

Payment plans let you spread tuition payments across the semester or academic year without interest charges. This doesn't reduce your total cost, but it improves cash flow and might reduce how much you need to borrow.

Part-time work options include on-campus employment, which F-1 students can pursue up to 20 hours weekly during the academic year. After your first year, you might qualify for Curricular Practical Training (CPT). Post-graduation, Optional Practical Training (OPT) provides work authorization in your field. These earnings can reduce your borrowing needs significantly.

Comparing Loan Types for International Students

| Feature | Federal Loans | Private International Student Loans |

| Who Qualifies | Citizens and eligible noncitizens only | International students on valid visas (usually with cosigners) |

| Current Interest Rates | 5.50% - 8.05% fixed | 4.50% - 14.00% fixed or variable |

| Repayment Options | 10-25 years; income-based plans available | 5-15 years; fixed schedules only |

| Cosigner Needed | Not for Direct Loans; sometimes for PLUS | Usually yes; limited no-cosigner programs exist |

| Credit Requirements | None for Direct Subsidized/Unsubsidized | Required for borrower and/or cosigner |

| Maximum Amounts | $5,500-$12,500 yearly (undergrad); $20,500 (grad) | Up to total cost of attendance |

Frequently Asked Questions About International Student Loans

International students can absolutely borrow money to finance U.S. education through private lenders, but the process looks nothing like what American students experience. Most lenders demand a creditworthy U.S. cosigner, creating a massive hurdle for students without family or close connections who've immigrated here. Specialized no-cosigner lenders have improved access, particularly for graduate students at top schools, though these programs serve a much narrower population.

Success depends on early planning and spreading your funding across multiple sources. Students who start researching options six to nine months before enrollment, who actively hunt for scholarships and institutional aid, and who honestly calculate the true cost of borrowing—including currency exchange issues and international employment realities—tend to make better decisions. Loans should supplement other funding sources, not serve as your only solution.

Before signing anything, run the numbers on your expected monthly payments based on realistic starting salaries. Think carefully about how long you'll stay in the U.S. after graduation. Understand what it means to repay U.S.-dollar debt while earning income in your home country's currency. Your education might open incredible opportunities, but the debt you take on will follow you through every door you walk through next.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.