Student reviewing college loan documents at desk with laptop and paperwork

How to Get Student Loans with No Credit?

Looking for college funding when you've never borrowed before? You're actually in the majority. Roughly 65% of incoming freshmen have zero credit history—no credit cards, no car loans, nothing for lenders to review. This creates a catch-22: you need loans to pay for school, but traditional lenders want proof you've successfully borrowed money before.

Here's what most students don't realize: the federal government specifically built loan programs for people in exactly your situation. Meanwhile, private lenders? They're trickier but not impossible—you'll just need a different game plan.

Why No Credit History Affects Student Loan Options

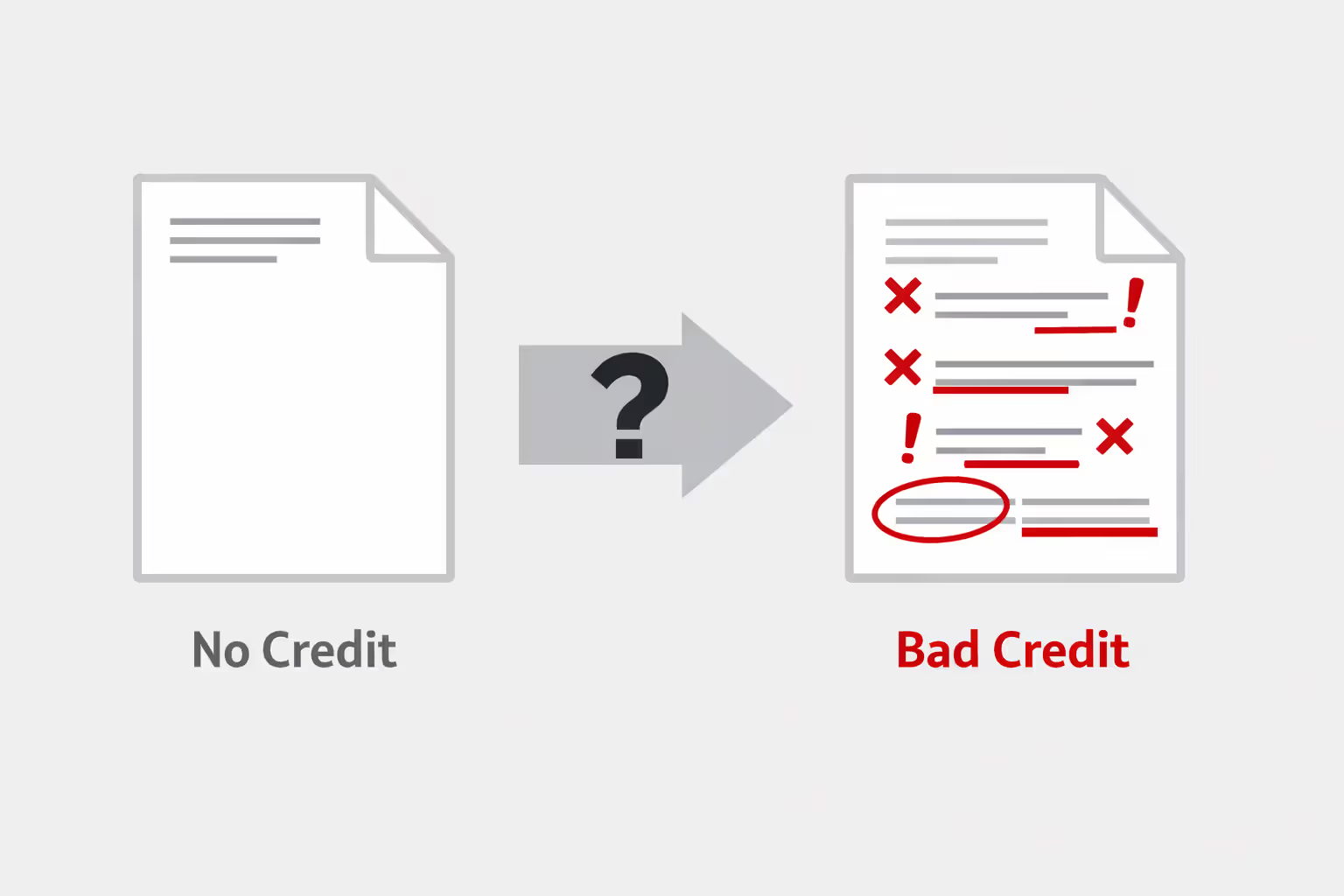

Think of "no credit" versus "bad credit" as two completely different animals. When you have no credit, your financial history is a blank page. Nothing good, nothing bad—just empty. Bad credit, though? That's a page filled with red flags: accounts sent to collections, maxed-out credit cards, or loan payments made 60+ days late.

Why does this matter? The Department of Education treats these situations very differently. For undergraduate federal loans, they essentially ignore credit entirely. Their logic makes sense: how could a 17-year-old possibly have an established credit file when they've been focused on AP classes and college applications? The FAFSA doesn't ask for credit scores or payment histories. Your enrollment status and household income determine eligibility, period.

Banks and credit unions take the opposite approach. They built their lending models on risk assessment, and without data about your borrowing behavior, they can't calculate that risk. You might be incredibly responsible with money—budgeting carefully, maintaining a savings account, working part-time throughout high school. None of that matters to their algorithms. No credit score equals higher risk category, which equals either denial letters or demands for someone with established credit to co-sign.

Most students arrive at college with blank credit files for completely ordinary reasons. You turned 18 recently. Your parents handled family finances and never added you as an authorized user on their cards. Maybe you worked summer jobs and saved cash instead of opening credit accounts. Some families actively avoid credit cards for cultural or religious reasons. None of these situations suggest financial irresponsibility, yet they all create the same obstacle when you're filling out private loan applications.

The practical impact depends entirely on which type of loan you're pursuing. Federal Direct Loans? Your blank credit history doesn't matter at all. Private loans from Sallie Mae, Discover, or Citizens Bank? You'll face either outright rejections or requirements for a creditworthy cosigner with a FICO score above 670. Understanding this divide before you start applying saves you from wasting hours on applications destined to go nowhere.

Author: Evan Thornton;

Source: sonicmusic.net

Federal Student Loans That Don't Require Credit Checks

The federal student loan system provides the clearest path forward when your credit report looks like a blank document. These programs were deliberately designed to make higher education accessible regardless of borrowing history.

Direct Subsidized and Unsubsidized Loans

Direct Subsidized and Unsubsidized Loans represent your best option, hands down. Zero credit check involved. The government won't pull your credit report, won't ask about your FICO score, and won't penalize you for never having used a credit card before.

Subsidized loans deliver the strongest terms you'll find anywhere. While you're enrolled in classes (at least half-time), the Education Department covers your interest charges. That benefit continues during the six-month grace period after graduation and throughout any approved deferment periods. To qualify, your FAFSA results must demonstrate financial need based on the cost of attendance minus expected family contribution. First-year dependent students can borrow up to $3,500 in subsidized loans, while third-year and fourth-year students qualify for $5,500 annually.

Unsubsidized loans skip the financial need requirement entirely. Interest starts accumulating the moment funds hit your school's bursar account, but you won't make payments until after you graduate. These loans plug funding gaps when subsidized amounts fall short of your actual costs. Independent undergraduates and graduate students can access up to $20,500 per year through unsubsidized loans.

Both loan categories come with fixed interest rates that Congress sets annually each spring. For loans disbursed between July 1, 2025, and June 30, 2026, undergraduates pay 6.53% while graduate students pay 8.08% on unsubsidized loans. Here's the key advantage: those rates apply whether you have perfect credit, terrible credit, or no credit whatsoever. Private lenders would charge someone without credit history anywhere from 9% to 14%, making federal loans substantially cheaper.

Direct PLUS Loans for Parents

Parent PLUS Loans help families cover remaining costs after exhausting undergraduate federal loan limits. These do involve credit checks, but the criteria work completely differently than what private lenders use.

The Education Department searches for what they call "adverse credit history" rather than calculating credit scores. Specifically, they look for five types of negative events occurring within the past five years: accounts in default status, bankruptcy discharge, foreclosure, repossession, tax lien, wage garnishment, or federal student loan charge-off. Having no credit history at all? That doesn't count as adverse. Parents with completely blank credit files typically receive approval without issues.

What happens if a parent has adverse credit on their record? Two options remain available. They can ask someone with clean credit to serve as an endorser (the PLUS loan equivalent of a cosigner), or they can document extenuating circumstances that explain the negative events—serious illness, job loss, divorce. This flexibility makes Parent PLUS Loans more accessible than many families realize when they first investigate options.

Parents can borrow the full cost of attendance at your school, minus any other financial aid you've received (grants, scholarships, federal student loans). For the 2025-2026 academic year, Parent PLUS Loans carry a 9.08% fixed interest rate. That's higher than undergraduate rates, sure, but it remains competitive with what private lenders charge borrowers who lack strong credit profiles.

Author: Evan Thornton;

Source: sonicmusic.net

Private Student Loan Options for Borrowers with No Credit

Private lenders step in when federal aid leaves gaps between what you've received and what you actually need to cover tuition, housing, books, and living expenses. However, navigating private loans without credit history requires understanding your limited pathways.

Nearly every major private lender sets minimum credit score thresholds between 650 and 700 for applicants without cosigners. Since you can't have a score without a credit history, you automatically fall short. Three realistic strategies exist:

Cosigner arrangements represent your most likely path to approval. A cosigner—usually a parent, grandparent, aunt, uncle, or family friend with established credit—legally agrees to repay your loan if you don't. Lenders primarily evaluate the cosigner's financial profile: credit score, annual income, existing debt obligations, employment history, and debt-to-income ratio (typically must stay below 43%).

Selecting a cosigner carries real weight for both parties. That person takes on full legal responsibility for potentially $20,000, $40,000, or more in debt. The loan appears on their credit report immediately and stays there throughout repayment. If you miss a payment, their credit score drops alongside yours. Many lenders advertise cosigner release programs that supposedly remove the cosigner after 24-48 consecutive on-time payments plus proof of income and credit score requirements. Reality check: fewer than 20% of borrowers who apply for cosigner release actually receive approval. Read the fine print carefully and never assume release is guaranteed.

Income-based programs exist but remain extraordinarily rare for traditional full-time students. Maybe three or four lenders nationwide offer programs that evaluate current employment income instead of credit history. The catch? You'll need verifiable annual income of $35,000 to $45,000—essentially impossible if you're taking 15 credits per semester. These programs work for part-time students with full-time jobs, but even then, interest rates typically run 2-3 percentage points higher than what cosigned loans offer.

School-specific lending partnerships occasionally create alternative pathways. Some universities negotiate special programs with regional credit unions or community banks. These partnerships might offer streamlined applications that consider your major, GPA, or enrollment status alongside traditional credit factors. Availability varies wildly—a state university in Ohio might have three partner lenders while a private college in California has none. Terms aren't automatically better than national lenders, so compare carefully.

When shopping for private lenders, dig deeper than advertised interest rates. Application fees ranging from $25 to $100 add immediate costs. Origination fees between 1% and 5% get deducted from your loan proceeds before money reaches your school. Late payment penalties vary from $25 flat fees to 5% of the missed payment amount. Repayment terms spanning 5, 10, 15, or 20 years dramatically affect monthly payments and total interest paid. A $30,000 loan at 7% costs roughly $41,600 total over 10 years but $54,500 over 20 years—nearly $13,000 extra.

Hardship options become critical if you face unemployment or medical emergencies post-graduation. Some lenders provide three to twelve months of forbearance for unemployment. Others offer temporary interest-only payments. A few provide essentially nothing beyond the standard six-month grace period. You're stuck with that servicer for years—choose one with decent customer service ratings and meaningful flexibility options.

How to Apply for Student Loans Without a Credit History

Strategic application processes maximize your approval odds and minimize costs. Following these steps in order matters.

Completing the FAFSA

The Free Application for Federal Student Aid unlocks every federal loan, grant, and work-study program available to you. Submit it the moment it opens on October 1 for the following academic year—don't wait. Why? Many states allocate grant funding first-come, first-served. California's Cal Grant deadline hits March 2, missing it costs you up to $12,630 annually. Illinois' MAP Grant typically exhausts funding by late spring. Procrastination literally costs thousands of dollars in free money.

You'll need Social Security numbers for yourself and parents (if you're dependent), previous year's federal tax returns, W-2 forms, records of untaxed income (child support, veterans benefits, etc.), and current bank account balances. Dependent students under age 24 must provide parent financial information unless specific circumstances apply (married, have dependents, military service, emancipated minor, or homeless). Independent students report only their own finances and spouse's if applicable. Set aside 45 minutes to complete the application—longer if your parents are divorced or you have complicated financial situations.

Your FAFSA generates a Student Aid Index (SAI) that schools use to determine your federal aid eligibility. Financial aid offices build packages combining grants (free money), work-study opportunities, and loan offers. Review these packages skeptically—some schools automatically include Parent PLUS Loans even though parents must separately apply. Others stack loans generously but provide minimal grant aid.

Prioritize accepting aid in this sequence: grants first (free money you never repay), then Direct Subsidized Loans, followed by Direct Unsubsidized Loans, and only then consider private options. This hierarchy keeps borrowing costs lowest and maintains maximum flexibility during repayment.

Author: Evan Thornton;

Source: sonicmusic.net

Finding a Cosigner

When federal loans fall short of covering your costs, identify potential cosigners before touching private loan applications. Your ideal cosigner brings a credit score above 700, steady employment for at least two years, total debt payments (including your potential student loan) below 40% of monthly gross income, and genuine willingness to accept the legal obligation.

Schedule honest conversations about expectations before anyone signs paperwork. Discuss backup plans if you struggle with payments post-graduation. Will they expect monthly status updates? How do they feel about cosigner release processes? Some families draft informal written agreements outlining responsibilities and expectations, though these don't override actual loan contracts.

Evaluate your cosigner's complete financial picture, not just their willingness to help. Cosigning for $50,000 in student loans affects their ability to qualify for mortgages, car loans, or credit cards because those debts count in their debt-to-income calculations. A parent helping you might inadvertently block themselves from refinancing their house or buying a newer vehicle.

If your first-choice cosigner declines or doesn't qualify, explore alternatives: grandparents who've paid off their mortgages, aunts or uncles with strong incomes, or close family friends who trust your commitment to education. Some students split borrowing across multiple academic years with different cosigners to spread the obligation, though tracking multiple loan servicers gets complicated quickly.

Comparing Loan Offers

Once you've identified lenders willing to work with cosigners for borrowers lacking credit history, compare offers systematically. Build a spreadsheet tracking interest rates (fixed versus variable), origination fees, application fees, repayment terms, monthly payment estimates, total repayment amounts, and special features (unemployment forbearance, rate reductions for autopay, cosigner release criteria).

Use prequalification tools whenever lenders offer them. Prequalification involves soft credit pulls that estimate your likely rates without affecting credit scores. This lets you shop five or six lenders without accumulating hard inquiries on your cosigner's credit report (each hard inquiry can temporarily lower scores by 3-5 points). Multiple hard inquiries within 30 days typically count as a single inquiry when rate-shopping, but soft pulls avoid the issue entirely.

Calculate total repayment amounts, not just monthly payments. A loan charging 7% over 10 years costs considerably less than one charging 9% over 15 years, even though monthly payments look more manageable on the longer term. Run scenarios through online calculators to visualize these differences. A $25,000 loan at 7% for 10 years equals $290 monthly payments and $34,800 total repaid. That same loan at 9% for 15 years drops to $254 monthly but balloons to $45,720 total—nearly $11,000 extra.

Read borrower reviews focusing specifically on customer service during repayment. You'll interact with your loan servicer for a decade or more. Responsive service matters enormously when you need to adjust payment plans, request forbearance, or resolve billing errors. A lender offering 6.5% interest but terrible customer service might cause more headaches than one charging 7% with helpful support staff.

Building Credit While in School

Establishing credit during your college years positions you for financial opportunities after graduation. You'll qualify for better rates on auto loans and mortgages, rent apartments without massive security deposits, and potentially improve job prospects (about 25% of employers check credit reports during hiring processes).

Secured credit cards offer your easiest entry point into credit building. You deposit $200, $300, or $500 with a card issuer as collateral. They issue you a credit card with a limit matching your deposit. Use it for one or two small recurring expenses—Spotify subscription, Netflix, monthly transit pass. Pay the full statement balance every single month to avoid interest charges. After 8-12 months of consistent on-time payments, many issuers convert you to an unsecured card and mail back your deposit. Your credit report now shows a year of positive payment history.

Student credit cards were designed specifically for people in your situation. Issuers expect limited credit histories and adjust approval algorithms accordingly. Discover it® Student Chrome, Capital One Journey Student Rewards, and Bank of America® Travel Rewards for Students typically approve applicants with no prior credit. Look for cards charging zero annual fees—paying $35 to $95 yearly makes no sense when you're building credit. Modest rewards programs (1% cash back, travel points) provide nice bonuses but aren't the primary goal at this stage.

Becoming an authorized user on a parent's or relative's credit card can instantly boost your credit profile—if they maintain excellent payment habits. Their complete account history appears on your credit report, potentially adding years of positive payment data overnight. Critical caveat: their late payments damage your credit too. Only pursue this strategy with someone who pays balances in full and on time consistently. Also, confirm the card issuer reports authorized user activity to all three credit bureaus (Experian, Equifax, TransUnion). Some don't, making the exercise pointless.

Making on-time student loan payments builds credit once repayment starts post-graduation. Federal and private student loan servicers report payment activity monthly to credit bureaus. Consistent payments over multiple years demonstrate reliability to future lenders. Set up automatic payments through your loan servicer's website—this prevents missed due dates and many lenders reduce interest rates by 0.25% for enrolling in autopay.

Monitor your credit through free services like Credit Karma, CreditWise from Capital One, or AnnualCreditReport.com (the official site for free annual reports from all three bureaus). Watch for errors—wrong addresses, accounts you didn't open, incorrect payment statuses. Dispute mistakes immediately through the credit bureau's website. Understanding which factors affect your score helps you make better financial decisions. Building credit requires patience—expect 8-12 months of responsible behavior before seeing meaningful score improvements, typically reaching the 650-700 range after one year of consistent positive activity.

Author: Evan Thornton;

Source: sonicmusic.net

Federal vs. Private Student Loans for No-Credit Borrowers

| Loan Type | Credit Check Required | Cosigner Needed | Interest Rates (2025-26) | Annual Borrowing Limits | Repayment Terms |

| Direct Subsidized | None | Not required | 6.53% (fixed rate) | $3,500-$5,500 depending on year in school | 10-25 years with multiple repayment plans including income-driven options |

| Direct Unsubsidized | None | Not required | 6.53% undergrad / 8.08% graduate (fixed rates) | Up to $20,500 for independent students | 10-25 years with multiple repayment plans including income-driven options |

| Parent PLUS | Yes (adverse credit review only) | Not applicable (parent is primary borrower) | 9.08% (fixed rate) | Full cost of attendance minus other aid received | 10-25 years with limited income-driven options |

| Private Student Loans | Yes (comprehensive credit review) | Nearly always required when applicant has no credit | 4.99%-14.99% (variable or fixed depending on creditworthiness) | Full cost of attendance minus other aid received | 5-20 years with minimal flexibility or hardship options |

Common Mistakes When Getting Student Loans with No Credit

New borrowers frequently make expensive mistakes that create unnecessary financial stress for years after graduation.

Borrowing maximum approved amounts without calculating actual needs traps students in excessive debt. Lenders might approve $18,000 annually, but do you actually need that much? Calculate your real costs: tuition and fees (check your school's exact amounts), required textbooks and course materials (buy used or rent when possible), housing (consider living at home or sharing apartments), food (cooking costs far less than meal plans), transportation, and minimal entertainment. Work 10-15 hours weekly, apply for every relevant scholarship, and cut unnecessary expenses before borrowing. Remember: every dollar borrowed today costs roughly $1.35 to $1.50 repaid over 10 years once interest accumulates. Borrowing an extra $5,000 annually across four years equals $20,000 principal plus $6,000-$8,000 in interest—nearly $28,000 total for money you didn't truly need.

Skipping federal loans in favor of private options makes zero financial sense yet happens surprisingly often. Some students feel embarrassed about government assistance (don't be—federal aid isn't welfare, it's standard educational financing). Others assume private loans offer better terms because banks have slicker marketing. Federal loans provide income-driven repayment plans that cap payments at 10% of discretionary income, potential loan forgiveness after 20-25 years in income-driven plans or 10 years in public service, generous deferment and forbearance options during unemployment or economic hardship, and no prepayment penalties. Private loans provide essentially none of these protections. Exhaust your federal Direct Loan eligibility completely before considering private alternatives.

Misunderstanding cosigner release requirements creates family tensions and credit complications that last for years. Students assume they can remove cosigners shortly after graduation, but reality differs dramatically. Typical release requirements include 24-48 consecutive on-time payments (two to four years of perfect payment history), proof of income meeting lender thresholds—often 2-3 times your monthly loan payment, meaning you need $60,000-$75,000 annual income for a $400 monthly payment—credit scores above 650-700, and sometimes graduation verification or degree completion. Even meeting all criteria doesn't guarantee approval. Some lenders approve fewer than 15% of cosigner release applications. If keeping your cosigner's credit clear matters to your family, prioritize lenders with transparent release criteria and published approval rates above 50%.

Author: Evan Thornton;

Source: sonicmusic.net

Ignoring interest rate differences costs thousands over loan lifetimes yet gets overlooked when students focus solely on approval. A 2-percentage-point rate difference on $35,000 borrowed equals roughly $7,000 additional interest over 10 years. Students stressed about getting approved at all sometimes grab the first offer without shopping around. Even with zero personal credit, cosigner strength significantly impacts rates—a cosigner with a 790 credit score might secure 5.5% while one with 680 gets quoted 8.5%, creating a $10,000+ difference in total interest on $40,000 borrowed.

Failing to understand interest capitalization increases total debt substantially but rarely gets explained clearly during applications. Unsubsidized federal loans and virtually all private loans accrue interest from the day funds disburse. If you don't pay interest as it accumulates during your four years in school, it capitalizes—gets added to your principal balance—when repayment begins. A $22,000 loan accumulating $4,400 in interest during four years becomes a $26,400 loan, and future interest calculates on that higher amount. Paying even $40-$60 monthly toward interest while enrolled reduces long-term costs by several thousand dollars. Many students can cover this from part-time work without difficulty.

Students without established credit should max out federal Direct Loans before touching private options. Federal loans offer repayment flexibility that becomes absolutely critical if you face unemployment, medical emergencies, or other financial hardships after graduation—protections you simply cannot find with private lenders, regardless of their advertised interest rates or approval processes

— Michael Torres

FAQ

Securing funding for college without credit history requires understanding which doors open easily and which require additional keys. Federal Direct Loans provide accessible, fixed-rate financing with zero credit requirements, making them your logical starting point regardless of your financial situation. These programs were deliberately built for borrowers in exactly your position—leverage them fully before exploring alternatives.

Private loans demand strategic planning when your credit report is blank. Cosigners create bridges between your current financial profile and private lender requirements, but these arrangements carry meaningful responsibilities for everyone involved. Select cosigners thoughtfully, understand release policies completely, and commit to protecting their credit through consistent on-time payments throughout repayment.

Building credit during your college years transforms your financial opportunities well beyond graduation. Small deliberate steps—opening a secured credit card, becoming an authorized user, managing loan payments responsibly—compound into strong credit profiles that unlock better rates on future borrowing and reduce costs throughout your adult life.

Sidestep common pitfalls by borrowing only what genuinely covers your needs, exhausting federal options before touching private loans, and comparing offers systematically rather than accepting the first approval letter. The borrowing decisions you make now reverberate through 10+ years of repayment. Approach student loans strategically, understand your complete range of options, and prioritize loan products offering meaningful flexibility alongside competitive rates.

Your lack of credit history creates temporary obstacles, not permanent roadblocks. With the right approach and accurate information, you'll secure necessary educational funding while simultaneously building the financial foundation that supports your success long after graduation.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.