Student reviewing college financial aid and loan documents at a desk

How to Get a Student Loan for College?

Most families can't write a check for four years of tuition. You're probably staring at a $30,000+ annual price tag and wondering how anyone affords this without going broke. Student loans bridge that gap—but only if you know which ones to apply for and how to avoid the traps that leave borrowers drowning in debt.

Here's what nobody tells you upfront: the order matters. Grab federal loans first (they're cheaper and more forgiving), then look at private options only when you've maxed out the government money. Mess up this sequence and you'll pay literally thousands more in interest.

I'm breaking down the entire process here—from filling out that confusing FAFSA form to signing the legal paperwork that commits you to repayment. You'll see exactly who qualifies, which applications to complete, where the money actually comes from, and what rookie mistakes cost students the most. By the end, you'll know how to borrow smart instead of just borrowing desperately.

Types of Student Loans You Can Apply For

You've got two distinct worlds when hunting for education financing: government-backed options through the Department of Education, and commercial products from financial institutions. Which one you pick determines everything from your interest rate to whether you can pause payments during a job loss.

Federal Direct Subsidized Loans represent the gold standard for undergrads who qualify based on financial need. Uncle Sam covers your interest charges while you're taking classes (at least half-time), during your six-month post-graduation grace period, and if you temporarily stop payments through approved deferment. That interest subsidy alone saves thousands compared to other borrowing types.

Federal Direct Unsubsidized Loans open up to any undergrad, grad student, or professional degree candidate—your family's bank account doesn't matter here. The catch? Interest starts piling up the day your school receives the money. You can pay it monthly while studying, or let it compound and watch your balance grow before you even finish your degree.

Direct PLUS Loans work for two specific groups: parents helping their dependent kids pay for undergrad, and graduate students funding their own advanced degrees. You'll face a credit review (they check for major red flags like bankruptcy or foreclosure, not your exact credit score). Parents who take these out own the entire debt—students have zero legal responsibility, which creates some uncomfortable family dynamics later.

Private student loans come from Wells Fargo, Discover, SoFi, local credit unions—basically any lender wanting to profit from education lending. They write their own rules for rates, approval standards, and repayment flexibility. Most require either excellent credit or someone willing to cosign who has it. You might snag competitive rates if your credit's stellar, but you're sacrificing all the federal safety nets like income-driven repayment and potential forgiveness.

The smart money exhausts every federal dollar before even glancing at private applications. Why? Those government protections become lifesavers when life throws curveballs like layoffs or medical emergencies.

Who Qualifies for Student Loans

Getting approved for federal aid requires meeting a surprisingly short checklist. You need U.S. citizenship or eligible non-citizen status, enrollment in at least six credits per semester at an accredited school, and registration in a degree or certificate program. That's it for the basics—most students clear this bar easily.

Academic standing matters more than you'd think. Fall below your school's satisfactory academic progress standards (usually around a 2.0 GPA and completing 67% of attempted credits), and you're cut off from all federal aid until you fix your transcript. I've seen students lose funding junior year because they ignored this rule.

The FAFSA sorts you into "dependent" or "independent" categories using factors like your age, marriage status, military service, and whether you're supporting children. This classification changes how much you can borrow—independent students access higher annual limits since they can't lean on parents for help.

Author: Marcus Bennett;

Source: sonicmusic.net

Credit checks don't exist for standard Direct Loans (subsidized and unsubsidized). An 18-year-old with zero credit history borrows at the same rate as everyone else. PLUS loans run an "adverse credit" screening that fails you only if you've got recent bankruptcies, default judgments, foreclosures, tax liens, or collection accounts over 90 days delinquent.

Private lenders operate in a different universe entirely. They want FICO scores above 670, steady income, and debt-to-income ratios that prove you can handle payments. Traditional college students rarely meet these standards alone, which is why 9 out of 10 private undergraduate loans include a cosigner—usually mom, dad, or a generous relative who's putting their own credit on the line.

International students can't touch federal money but might find private lenders willing to work with them if they've got a U.S. citizen cosigner. A few specialized companies will lend to international students without cosigners, though expect eye-watering interest rates.

Steps to Get a Federal Student Loan

Federal borrowing follows a rigid sequence with specific deadlines. Skip a step or miss a date, and you're scrambling to cover bills while your classmates are already in class.

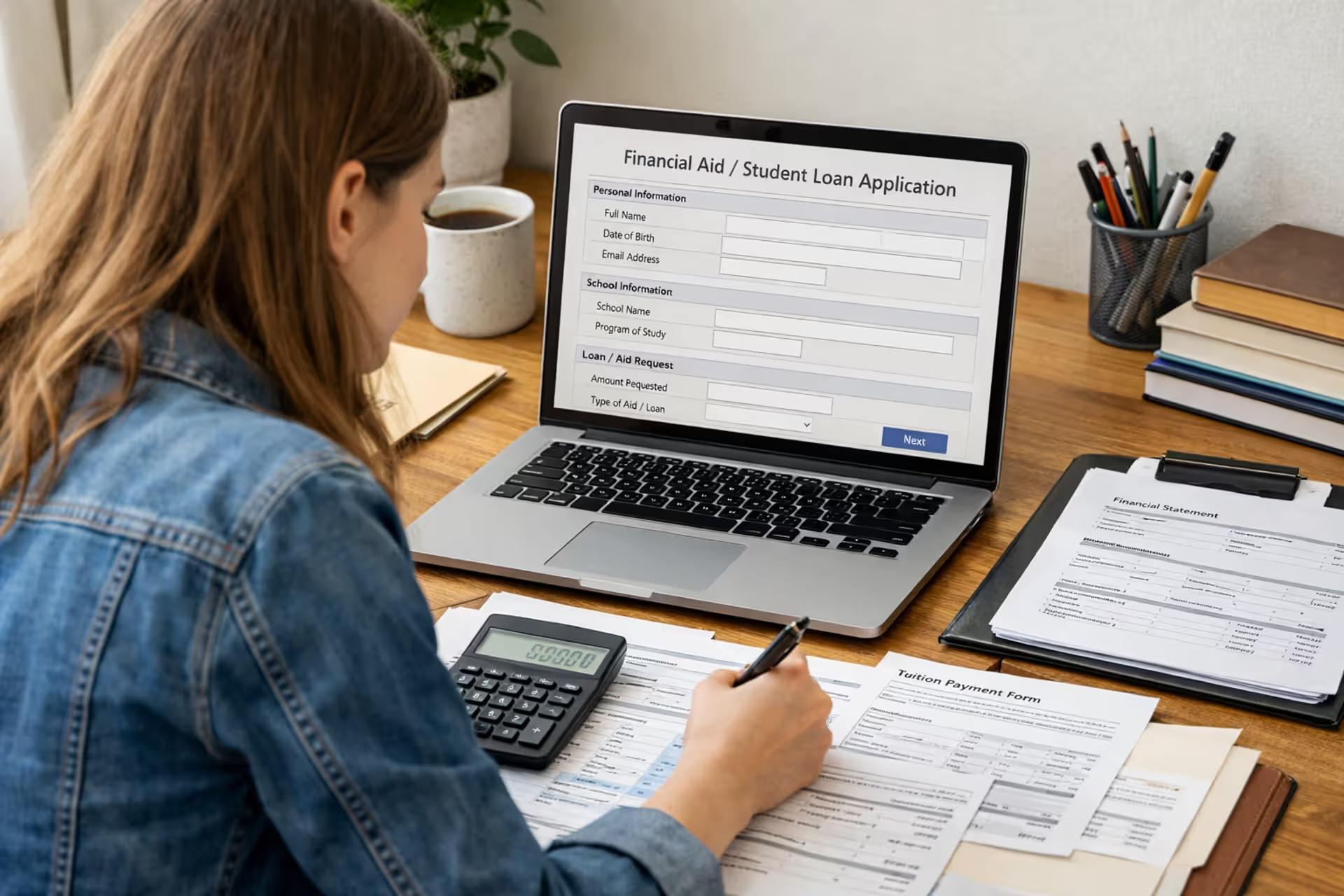

Complete the FAFSA

This single form unlocks every type of federal aid—grants that never need repayment, campus job opportunities, and yes, loans. The application goes live each October 1st for the next school year. Earlier submission matters because some aid types like subsidized loans run on a first-come, first-served basis until the money's gone.

Gather your Social Security number, driver's license number, tax returns (yours and your parents' if you're dependent), W-2 forms, and records of untaxed income. The IRS Data Retrieval Tool pulls your tax info automatically, which speeds things up and cuts down on errors that delay processing. Create your FSA ID first—this username and password combo becomes your legal signature on all federal aid documents. Dependent students need one parent to create a separate FSA ID too.

The form crunches your financial data to calculate your Student Aid Index (previously called Expected Family Contribution). This number estimates what your household can supposedly afford toward college costs. Schools use your SAI to determine which need-based aid you qualify for, including those valuable subsidized loans.

Author: Marcus Bennett;

Source: sonicmusic.net

Review Your Financial Aid Offer

Colleges mail or email award letters usually 2-4 weeks after you're admitted. These documents list everything you're eligible for: Pell Grants, institutional scholarships, work-study earnings potential, and loan options. Be warned—award letter formats vary wildly. Some schools clearly separate free money from borrowed money. Others lump everything together as "awards," making loans look like prizes instead of debt.

Compare what's offered against your actual costs. Add up tuition, mandatory fees, housing, meal plans, books, transportation, and personal expenses. Subtract any grants and scholarships. That remaining gap shows what you'll cover through family help, your own savings, work income, and loans.

You're never required to accept the full loan amount they offer. Borrow only what you genuinely need. Taking an extra $2,000 "just in case" costs you about $2,500 with interest over a standard 10-year repayment.

Accept Your Loan and Complete Entrance Counseling

Once you've decided which loans to take, log into your school's financial aid portal and accept the specific amounts you want. First-time federal borrowers must complete entrance counseling before receiving any money—a 30-minute online session explaining how loans work, what repayment looks like, and what happens if you default.

You'll learn about interest accrual, different repayment plans, when you can pause payments, and how default wrecks your credit and future finances. The session includes quiz questions checking your comprehension. Can't proceed until you pass.

This counseling exists because too many students sign loan documents without grasping they're making legally binding commitments to repay real money with interest. Default isn't just an inconvenience—it triggers wage garnishment and tax refund seizure.

Sign the Master Promissory Note

The MPN is your legal promise to repay what you borrow plus interest and fees. One MPN covers federal loans for up to 10 years, so you'll sign it once and then receive future year loans without new promissory notes (though you still complete annual loan acceptance and counseling).

The note spells out your interest rate, when payments start, how to postpone payments if needed, and what constitutes default. Read it carefully—student loan debt survives bankruptcy in most situations.

Sign electronically at StudentAid.gov using your FSA ID. The whole process takes 15-30 minutes including extra disclosure screens about your obligations.

How to Apply for Private Student Loans

Turn to private loans only after you've claimed every federal dollar, scholarship, and family contribution available. Commercial loans cost more long-term and offer zero federal safety features, but sometimes they're the only way to close a funding gap.

When private loans make sense: You've already borrowed your maximum federal loan limits for your grade level and still owe the school money. Maybe you're enrolled in a program that doesn't qualify for federal aid. Some borrowers refinance their loans after graduation to grab lower interest rates, though this eliminates all federal benefits permanently.

Shopping for lenders: Rates, fees, repayment lengths, cosigner release rules, and hardship forbearance options vary dramatically across lenders. Traditional banks, credit unions, and online-only lenders all want your business. Credit unions often beat others on rates if you're a member. Online lenders sometimes offer more flexible terms for borrowers with unique situations.

Get rate quotes from at least three companies. Most provide prequalification estimates using soft credit pulls that don't ding your credit score. Compare APRs instead of just interest rates—APR includes fees and shows true borrowing costs.

Fixed rates keep your payment consistent for the entire loan term. Variable rates fluctuate with market benchmarks like SOFR, often starting lower but potentially climbing substantially during a decade of repayment. If you hate financial uncertainty, pay a bit extra for fixed-rate stability.

What lenders want to see: Your credit score, current income, work history, debt-to-income ratio, and proof that you're enrolled and how much school costs. You'll complete an online application, have your school certify your enrollment and expenses, and authorize credit checks.

Processing takes anywhere from two to six weeks depending on the lender and whether cosigner coordination slows things down. Apply way before your tuition deadline to avoid late payment penalties or dropped classes.

The cosigner reality: About 90% of private undergrad loans require cosigners because traditional students lack the credit history and income lenders demand. Your cosigner's strong credit and stable income dramatically improve approval odds and lower your rate. But they're equally responsible for repayment—your missed payments trash both credit reports.

Some lenders release cosigners after you've made 24-48 consecutive on-time payments and meet specific income and credit benchmarks. This option frees them from obligation, though the qualification standards can be tough. Nail down cosigner release terms before signing anything.

Author: Marcus Bennett;

Source: sonicmusic.net

What Happens After Your Loan Is Approved

Approval doesn't put cash in your pocket. Both federal and private lenders follow specific disbursement procedures synced with your school's billing calendar.

How disbursement works: Lenders wire funds directly to your school's bursar's office, typically 10 days before the semester starts. The school immediately applies that money toward your tuition bill, mandatory fees, and campus housing/meal plan charges. Only after covering these institutional costs does any excess come to you.

First-time borrowers at a particular school face a mandatory 30-day waiting period before that initial disbursement hits. This cooling-off period protects students from borrowing impulsively for their very first semester.

Federal loans split into at least two payments—one per semester if you borrowed for the full academic year. Borrow $5,500 annually and you'll receive $2,750 in fall, $2,750 in spring. Private lenders might disburse per semester or in one lump sum based on their policies.

Author: Marcus Bennett;

Source: sonicmusic.net

Getting your refund: When your loan exceeds direct charges to the school, they refund the difference. Expect this money via direct deposit, paper check, or loaded onto a school-branded debit card within 14 days of disbursement.

Spend refunds wisely on legitimate education expenses: textbooks, course supplies, laptop, commuting costs, rent and groceries if you live off-campus. Some students blow refunds on spring break trips or new phones, racking up debt for things unrelated to their education.

Understanding grace periods: Federal loans include a six-month buffer after you graduate, withdraw, or drop below half-time status before payments begin. You don't owe anything during grace, though interest keeps accumulating on unsubsidized and PLUS loans.

Use these six months to land a job, set up your budget, and choose a repayment plan. Configure autopay during grace to never risk a missed payment once repayment starts.

Private loan grace periods vary by lender. Some match the federal six-month standard. Others demand immediate repayment or give you just 90 days. Know your specific timeline or you'll get hit with unexpected bills right after graduation.

Federal vs. Private Student Loans: Key Differences

| Feature | Federal Student Loans | Private Student Loans |

| Interest Rates | Congress sets fixed rates annually (currently ranging from 5.50% to 8.05% based on loan type) | Rates from 3% to 14%+ based on credit; can be fixed or variable |

| Credit Requirements | Direct Loans require no credit check; PLUS loans screen for adverse credit only | Requires good credit (typically 670+ FICO) or creditworthy cosigner |

| Borrowing Limits | Specific annual and lifetime caps based on grade level and dependency status | Generally up to school's cost of attendance; actual amount depends on credit profile |

| Repayment Terms | Standard 10-year plan available; multiple income-driven options extending 20-25 years | Typically 5 to 20 years depending on lender; fewer flexible options |

| Forgiveness Options | Public Service Loan Forgiveness, Teacher Loan Forgiveness, income-driven plan forgiveness after 20-25 years | Generally none available; refinancing federal loans eliminates forgiveness eligibility |

| Payment Flexibility | Extensive deferment and forbearance for unemployment, hardship, returning to school | Limited forbearance policies that vary significantly by lender |

Common Mistakes When Getting Student Loans

Smart borrowing means sidestepping traps that inflate costs and create unnecessary stress. Watch for these frequent screwups:

Borrowing more than necessary: Students routinely accept the maximum loan offered without calculating actual need. Every extra dollar borrowed collects interest. Accept an unnecessary $3,000 yearly for four years and you've added $12,000 in principal plus several thousand more in interest over repayment.

Build a real budget. Track what you actually spend on books (buying used or renting often cuts costs 60%), supplies, food, and housing. Most students overestimate expenses, especially textbook costs that seem outrageous until you find alternatives.

Jumping to private loans too quickly: Commercial loans exclude you from income-driven repayment, Public Service Loan Forgiveness, and generous postponement options. Students who skip straight to private borrowing because the amounts seem higher or the process appears simpler end up regretting lost protections when financial hardship hits.

Submit the FAFSA regardless of whether you think you'll qualify for need-based aid. Unsubsidized loans don't require demonstrated need, but you can't access them without a FAFSA on file.

Ignoring the fine print: Loan agreements contain critical details about rates, fees, repayment schedules, and penalties. Students who skim past the details miss crucial information about when interest capitalizes (adds to your principal balance), how often variable rates adjust, and what triggers default.

Check specifically whether interest capitalizes when repayment starts or only during default. Capitalization substantially inflates total repayment on large balances.

Treating all interest rates equally: A 2% rate difference sounds trivial until you do the math. On $30,000 over 10 years, 5% interest costs roughly $8,000 in total interest while 7% costs about $12,000—that's $4,000 more for the same education.

Federal rates are set annually by Congress and identical for all borrowers within each loan category. Private rates vary based on credit. Even small rate reductions through a creditworthy cosigner or shopping different lenders add up to major savings.

Forgetting about loan fees: Federal Direct Loans charge origination fees subtracted from what your school receives. For loans disbursed October 2025 through October 2026, fees run approximately 1.057% for subsidized and unsubsidized loans. Borrow $5,000 and the school gets around $4,947 after the fee, but you're repaying the full $5,000 plus interest.

Private loans might charge origination fees, application fees, or prepayment penalties. Calculate total costs including every fee, not just the advertised rate.

Federal loans should be your absolute first stop after exhausting scholarships and grants.We see students every year who grabbed private loans first because they heard back faster or thought the process seemed simpler, and they're kicking themselves later when they realize what they gave up. Federal borrowers get income-driven repayment that caps payments at 10% of discretionary income—that's literally saved people from default during the 2020 recession and the job market chaos we saw in 2023. Private lenders just don't offer that kind of flexibility. My rule is simple: max out federal options completely before you even start comparing private lenders

— Jennifer Martinez

Frequently Asked Questions About Getting Student Loans

Borrowing for college means balancing today's tuition bills against your financial reality for the next 10-20 years. The process starts with understanding which loan types match your situation, confirming you meet eligibility standards, and following proper application procedures for federal or private options.

Build your borrowing strategy on federal loans as the foundation. Complete the FAFSA every single year, accept subsidized loans before anything else, then take unsubsidized loans, and consider PLUS or private loans only when federal sources can't cover remaining costs. This priority order ensures you're accessing the lowest available rates and strongest borrower protections.

Private loans fill legitimate funding gaps but force trade-offs you need to understand. Shop at least three lenders, understand how fixed versus variable rates affect your long-term costs, and read every term before signing. If you need a cosigner, have honest conversations about expectations—they're assuming genuine financial risk for you.

Borrow conservatively. Every dollar you skip borrowing is a dollar you won't repay with accumulated interest. Create realistic expense budgets, cut unnecessary spending, and consider part-time work to reduce loan dependence. Students who borrow thoughtfully graduate with debt loads that don't sabotage their financial futures.

Monitor your loans throughout college. Know your total borrowed amounts, current interest rates, and which servicers handle your accounts. This awareness prevents graduation-day shocks when you discover you've accumulated way more debt than you realized. Check the National Student Loan Data System (NSLDS) regularly to track federal loans and keep all private loan paperwork organized in one place.

The mechanics of getting a student loan are straightforward, but the choices you make during borrowing affect your finances for decades. Treat student loans as serious financial commitments, not just administrative paperwork blocking your path to classes. With deliberate planning and informed decisions, student loans become useful investments in your education instead of sources of lasting financial regret.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.