Young student studying loan documents on laptop with credit score graphs and financial charts displayed

How Credit Score Affects Student Loans?

Content

Content

Most students applying for loans to fund their college education don't realize that their credit profile can make or break their ability to secure financing—or at least determine what they'll pay for it. Unlike scholarships or grants, loans represent borrowed money that must be repaid, and lenders use credit scores as one way to predict whether borrowers will honor that obligation.

The relationship between credit scores and student loans works both ways. Your existing credit can determine which loans you qualify for and at what interest rate, while the student loans you take out will shape your credit profile for years to come. Understanding this dynamic before you apply can save you thousands of dollars and help you avoid common pitfalls that trap borrowers in unfavorable terms.

Do You Need a Credit Score for Student Loans?

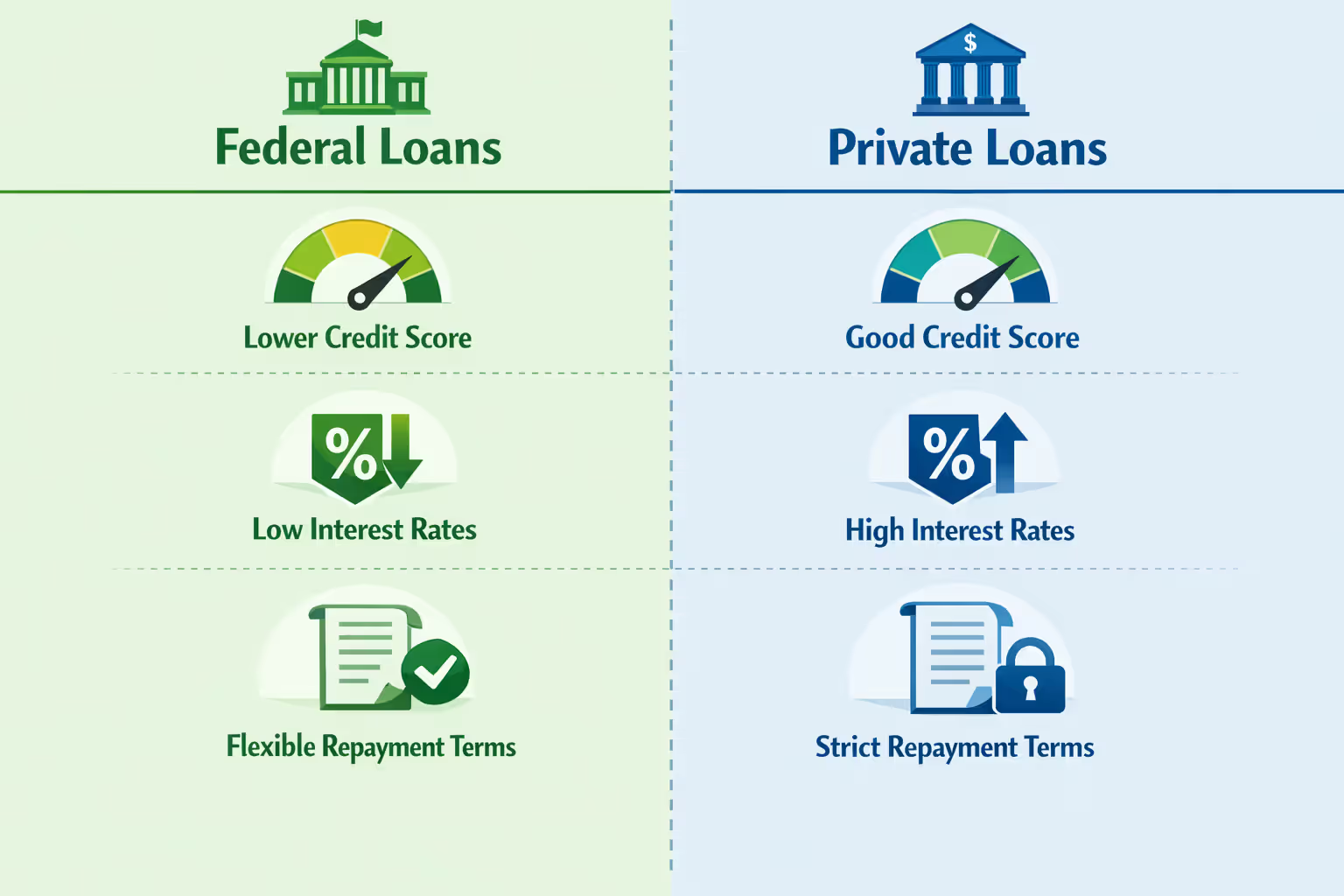

The answer depends entirely on which type of loan you're pursuing. Federal student loans and private student loans operate under completely different rules when it comes to credit score for student loans.

Federal student loans—those issued through the U.S. Department of Education—generally don't require a student loan credit check for undergraduate borrowers. Direct Subsidized and Direct Unsubsidized Loans are available to eligible students regardless of credit history. The government designed these programs specifically to make higher education accessible, even to young adults who haven't yet built a credit profile.

The exception within the federal system is the Direct PLUS Loan program, which includes both Parent PLUS Loans and Grad PLUS Loans. These do involve a credit review, though it's less rigorous than what private lenders require. The Department of Education checks for adverse credit history—things like accounts in collections, charge-offs, repossession, foreclosure, bankruptcy discharge within the past five years, or loan defaults. They're not looking at your three-digit score; they're checking whether you have serious derogatory marks.

Author: Danielle Pierce;

Source: sonicmusic.net

Private student loans from banks, credit unions, and online lenders operate more like traditional consumer credit products. Every private lender runs a full credit check and bases approval decisions primarily on your credit score and income. If you're a traditional college student with limited work history and no established credit, you'll almost certainly need a cosigner—typically a parent or guardian—whose credit and income the lender can evaluate instead.

This fundamental difference means that most students can access some form of student loan funding regardless of credit, but the best rates and highest borrowing limits typically go to those with strong credit profiles or creditworthy cosigners.

Minimum Credit Score Requirements by Loan Type

Understanding the specific student loan credit requirements for different loan types helps you target the right products and avoid wasting time on applications likely to be denied.

Author: Danielle Pierce;

Source: sonicmusic.net

Federal Student Loans

Direct Subsidized and Unsubsidized Loans have no minimum credit score requirement. Eligibility depends on completing the FAFSA, being enrolled at least half-time in an eligible program, and meeting citizenship or eligible noncitizen status. Annual borrowing limits range from $5,500 to $12,500 for dependent undergraduates, depending on year in school, with lifetime limits of $31,000.

Direct PLUS Loans—both Parent PLUS and Grad PLUS—require that you don't have adverse credit history as defined by the Department of Education. If you do have adverse credit, you can still qualify by obtaining an endorser (similar to a cosigner) or documenting extenuating circumstances related to the adverse credit. Interest rates for PLUS loans are higher than other federal loans, sitting at 9.08% for loans disbursed between July 2025 and July 2026.

Private Student Loans

Private lenders each set their own minimum credit score for student loans, but general patterns emerge across the industry. Most major lenders require a minimum score between 650 and 670 for approval, though some will consider applicants in the high 500s to low 600s with a strong cosigner.

The real differences show up in the interest rates offered. Borrowers with scores below 700 typically receive rates in the double digits, while those with scores above 750 can access rates starting in the 4-6% range for variable-rate loans. The spread between the best and worst rates can exceed 10 percentage points, which translates to tens of thousands of dollars over a standard 10-year repayment term.

Lenders also evaluate debt-to-income ratio, employment history, and monthly cash flow. A student working part-time while attending school rarely meets income requirements on their own, which is why approximately 90% of private student loans to undergraduate borrowers involve a cosigner.

| Loan Type | Credit Check Required | Minimum Credit Score | Cosigner Option | Typical Interest Rate Range (2026) |

| Direct Subsidized | No | None | No | 6.53% (fixed) |

| Direct Unsubsidized | No | None | No | 6.53% undergrad / 8.08% grad (fixed) |

| Direct PLUS | Yes (adverse history check) | No specific score | Yes (called "endorser") | 9.08% (fixed) |

| Private (excellent credit) | Yes | 750+ | Optional | 4.50%–7.50% variable / 5.50%–9.00% fixed |

| Private (good credit) | Yes | 670–749 | Optional | 7.00%–11.00% variable / 8.00%–12.00% fixed |

| Private (fair credit) | Yes | 600–669 | Usually required | 10.00%–14.00% variable / 11.00%–15.00% fixed |

How Student Loans Impact Your Credit Score

Taking out student loans initiates a long-term relationship with the credit bureaus. How credit score affects student loans is one question; how student loans affect your credit score is equally important.

When you first take out a student loan, the lender reports the new account to the three major credit bureaus—Experian, Equifax, and TransUnion. This immediately impacts several factors in your credit score calculation.

Payment history carries the most weight in credit scoring models, accounting for roughly 35% of your FICO score. Student loans offer an opportunity to build positive payment history over many years. Even while you're in school and making no payments (during the in-school deferment period), the loan appears on your report as current. Once repayment begins, each on-time monthly payment strengthens your credit profile. A single 30-day late payment, however, can drop your score by 60-110 points depending on your starting score.

Credit mix represents about 10% of your score. Having both revolving credit (credit cards) and installment loans (student loans, auto loans, mortgages) demonstrates you can manage different types of credit responsibly. For young adults whose only other credit might be a single credit card, adding student loans diversifies their credit profile.

Credit age factors into 15% of your score calculation. Student loans taken out at age 18 or 19 become some of your oldest accounts, which helps your score as they age—assuming you keep them in good standing.

New credit inquiries cause a small, temporary dip. Each hard inquiry from a loan application can lower your score by roughly 5-10 points. The impact fades within a few months and disappears entirely after 12 months, though the inquiry remains visible on your report for two years.

Credit utilization doesn't directly apply to student loans since they're installment loans rather than revolving credit. However, student loans do affect your overall debt load, which lenders consider when evaluating new credit applications.

The negative impacts typically come from missed payments, defaulting, or taking on more debt than you can realistically repay. Federal student loans enter default after 270 days of non-payment, while private loans typically default after 90-120 days. Default devastates your credit score, often dropping it 200+ points, and remains on your report for seven years.

Author: Danielle Pierce;

Source: sonicmusic.net

What Happens If You Have Bad Credit or No Credit History

Students with poor credit or no credit history at all still have multiple paths to securing student loan funding, though the options and terms vary significantly.

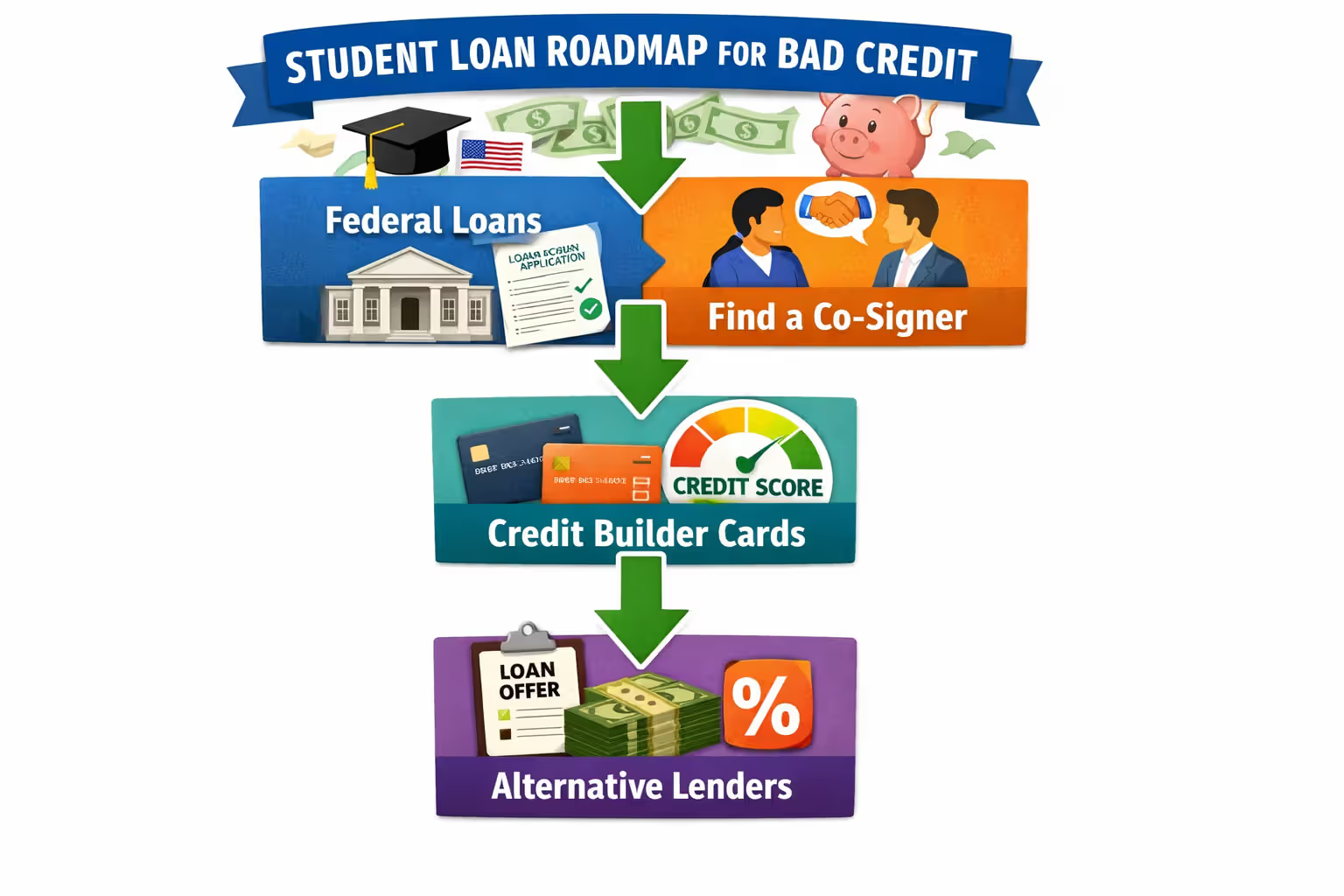

Start with federal student loans. Since Direct Subsidized and Unsubsidized Loans don't consider student loan credit requirements at all, they're available regardless of your credit situation. Max out these options first—they offer fixed rates, income-driven repayment plans, deferment and forbearance options, and potential loan forgiveness programs that private loans can't match.

If federal loans don't cover your full cost of attendance, consider these strategies:

Cosigner approach: Finding a cosigner with good credit (typically 670+) and stable income opens the door to private student loans with competitive rates. Parents, grandparents, aunts, uncles, or even family friends can serve as cosigners. The cosigner is equally responsible for the debt, so this is a serious commitment. Some lenders offer cosigner release after 24-36 consecutive on-time payments, allowing you to remove the cosigner once you've proven your reliability.

Credit-builder loans: Before applying for student loans, some students benefit from taking out a small credit-builder loan from a credit union. These loans—typically $300-$1,000—are deposited into a savings account you can't access until you've made all payments. The lender reports your payment history, helping you build credit over 6-12 months. This strategy works best if you have at least a year before you need student loan funding.

Secured credit cards: Opening a secured credit card requires a deposit (usually $200-$500) that becomes your credit limit. Use it for small purchases and pay the balance in full each month. After six months of responsible use, your score can improve enough to qualify for better loan terms.

Alternative lenders: A handful of private lenders specifically target students with limited credit history by considering factors beyond credit scores, such as your major, expected graduation date, and school's graduation rates. These lenders may offer approval where traditional banks won't, though rates are typically higher.

One common mistake: students with no credit sometimes avoid taking any loans, even subsidized federal loans, thinking they're protecting their future. In reality, responsibly managing a small student loan while in school can build credit that helps you qualify for an apartment lease, car loan, or credit card after graduation.

Author: Danielle Pierce;

Source: sonicmusic.net

How to Improve Your Credit Score Before Applying

If you have time before you need student loans—ideally 6-12 months—you can take concrete steps to improve your credit score for student loans and potentially save thousands in interest.

Check your credit reports for errors. Visit AnnualCreditReport.com to pull your reports from all three bureaus. About 20% of consumers have errors on their credit reports, including accounts that don't belong to them, incorrect late payment marks, or outdated information. Dispute any errors through the bureau's website; corrections typically take 30-45 days.

Pay down existing credit card balances. If you carry balances on credit cards, reducing your utilization ratio below 30%—and ideally below 10%—can boost your score by 20-50 points relatively quickly. If you have a $1,000 limit, keep your balance below $300 at all times, including before your statement closes.

Become an authorized user. Ask a parent or family member with excellent credit and a long-standing credit card to add you as an authorized user. The card's entire payment history may appear on your credit report, instantly adding positive history. You don't even need access to the physical card to benefit.

Pay all bills on time for six months straight. Recent payment history matters more than old mistakes. Six consecutive months of on-time payments across all accounts demonstrates improving reliability to lenders.

Avoid applying for new credit. Each application triggers a hard inquiry. If you're planning to apply for student loans in the next 3-6 months, avoid opening new credit cards or applying for other loans.

Don't close old accounts. Even if you're not using an old credit card, keeping it open (with a small recurring charge like a streaming service, paid automatically) helps your credit age and keeps your total available credit higher.

The timeline matters. Credit score improvements from paying down debt can appear within 30-60 days—whenever your creditors report to the bureaus. Improvements from payment history take longer to accumulate, typically 3-6 months of consistent behavior.

One trap to avoid: credit repair companies that promise to "fix" your credit quickly. Legitimate negative information can't be removed, and these companies often charge hundreds of dollars for services you can do yourself for free.

Student Loan Credit Check Process Explained

When you apply for a private student loan, the student loan credit check involves more than just pulling your three-digit score. Understanding what happens behind the scenes helps you prepare more effectively and avoid surprises.

Hard inquiry basics: When you submit an application, the lender performs a hard inquiry (also called a hard pull) that appears on your credit report. This inquiry remains visible for two years but only affects your score for about 12 months, with the most significant impact in the first few months.

Rate shopping window: Credit scoring models recognize that consumers shop around for the best loan rates. FICO scores group all student loan inquiries within a 14-45 day period (depending on the scoring model version) as a single inquiry for scoring purposes. This means you can apply to multiple lenders within a two-week window without multiplying the damage to your score. Plan your applications strategically—research lenders first, narrow down to 3-5 strong candidates, then submit all applications within a two-week span.

Beyond the score: Lenders pull your full credit report, not just your score. They review: - Payment history on all accounts (looking for late payments, collections, charge-offs) - Total debt load and monthly obligations - Recent inquiries (too many suggest financial stress) - Public records (bankruptcies, tax liens, judgments) - Account ages and types

Income verification: Private lenders require proof of income—recent pay stubs, tax returns, or offer letters for new jobs. For students with minimal income, the cosigner's income becomes the primary factor. Lenders typically want to see that monthly debt payments (including the new student loan) don't exceed 35-43% of gross monthly income.

School certification: Unlike credit cards or personal loans, student loans go through a school certification process. After preliminary approval, the lender contacts your school's financial aid office to verify your enrollment, cost of attendance, and other aid you're receiving. The loan amount may be adjusted based on this information.

Soft inquiry option: Some lenders offer prequalification with a soft inquiry that doesn't affect your credit score. This gives you a preliminary rate estimate before committing to a full application. Use these tools to compare offers before submitting formal applications.

The entire process—from application to disbursement—typically takes 2-6 weeks, though it can be faster or slower depending on how quickly you provide documentation and your school processes the certification.

Many students mistakenly believe that student loans will damage their credit, but the opposite is often true. When managed responsibly, student loans provide young adults with an opportunity to build a strong credit foundation that benefits them for decades. The key is understanding the terms before borrowing and treating every payment as an investment in your financial future

— Jennifer Martinez

Frequently Asked Questions About Student Loans and Credit Scores

The intersection of credit scores and student loans represents one of the first major financial decisions many young adults face. Unlike consumer purchases that provide immediate gratification, student loans fund an investment in your future earning potential—making the terms you secure today particularly consequential.

Federal student loans should form the foundation of most students' borrowing strategy. The lack of credit requirements for Direct Subsidized and Unsubsidized Loans levels the playing field, while built-in protections like income-driven repayment and potential forgiveness provide safety nets that private loans can't match. Exhaust these options before turning to private lenders.

When private loans become necessary, your credit profile—or your cosigner's—directly determines what you'll pay. A student with excellent credit borrowing $30,000 at 6% pays roughly $8,000 in interest over 10 years, while the same loan at 12% costs nearly $17,000 in interest. That $9,000 difference represents real money that could fund a car down payment, emergency fund, or retirement contributions in your twenties.

The relationship works in reverse too. Student loans you take out today will shape your credit profile for the next decade or more. Responsible management—on-time payments, avoiding default, staying in communication with servicers when problems arise—builds credit that opens doors to better rates on mortgages, auto loans, and credit cards throughout your adult life.

Start by checking your credit score and report before you need to borrow. Complete the FAFSA to access federal loans. If private loans are necessary, research lenders carefully, compare offers during a condensed timeframe to minimize credit inquiries, and understand every term before signing. Consider whether a cosigner makes sense, and if so, discuss expectations clearly with that person.

Your credit score doesn't have to be perfect to access student loans, but understanding how the system works gives you leverage to secure better terms and avoid costly mistakes that follow borrowers for years. Take the time to educate yourself before borrowing—your future self will thank you.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.