Young graduate in cap and gown holding diploma and bill envelope with a clock symbolizing countdown on a university campus background

When Does Student Loan Repayment Start?

Content

Content

Figuring out your first student loan payment date? It's trickier than marking graduation on your calendar and counting forward six months. The timeline depends on whether you borrowed through federal programs or private lenders—and your enrollment history matters way more than most borrowers realize. Most federal borrowers catch a six-month break after campus life ends, but that's not a universal guarantee. Private lenders follow their own schedules, and some will bill you while you're still taking finals. Nailing down these specifics now means you'll budget with confidence instead of panicking when the first statement arrives in your mailbox.

How Student Loan Grace Periods Work

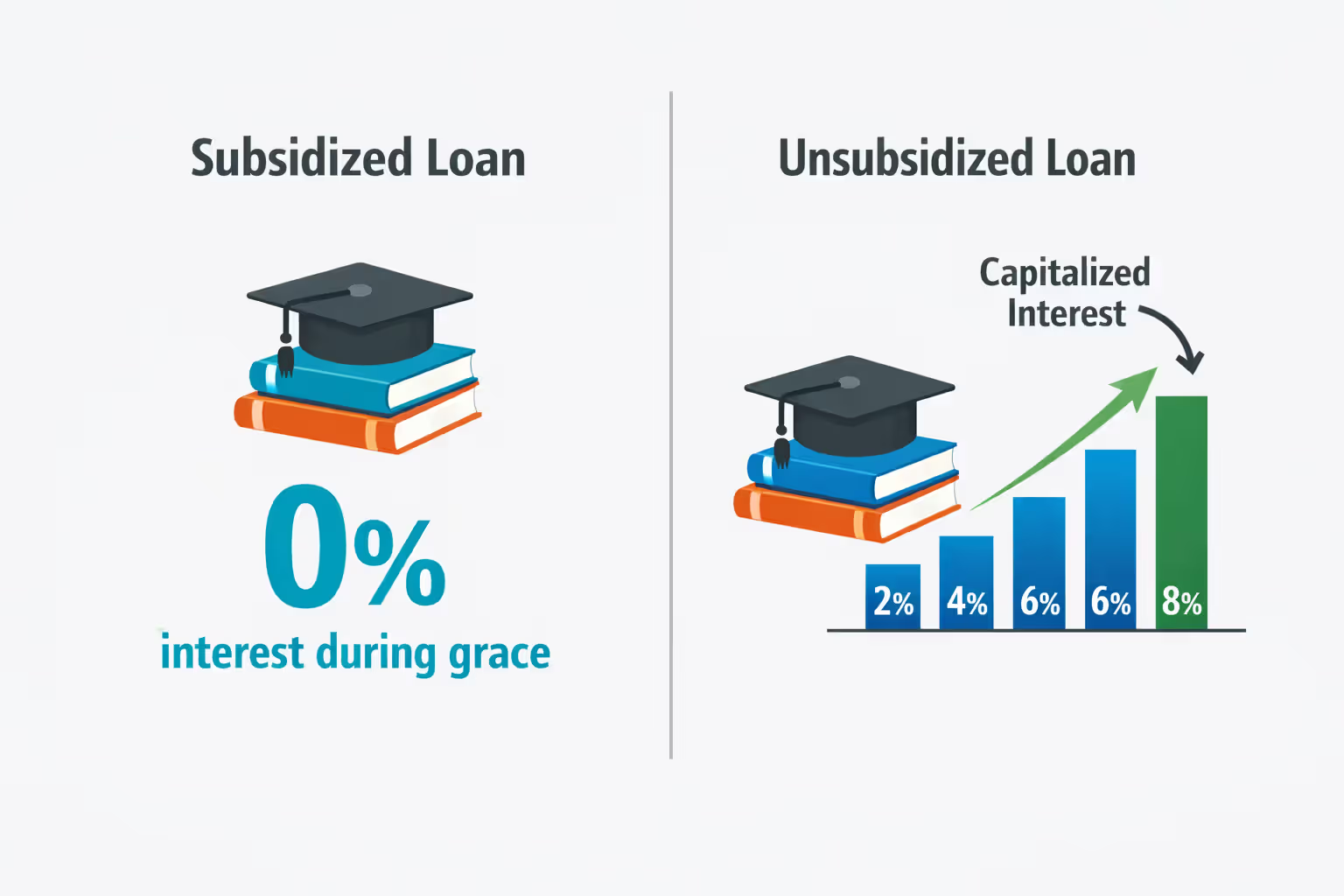

The grace period gives you financial breathing space between walking out of your last class and receiving your first payment notice. Direct Subsidized and Direct Unsubsidized federal loans come with a six-month window. You won't owe payments during this stretch, but interest might be working against you behind the scenes.

Subsidized loans offer an advantage here—the government covers interest charges throughout your grace window. You won't watch your balance climb higher during these payment-free months. Unsubsidized loans operate under different rules. Interest starts piling up from the day your first loan disbursement hits your account. Once repayment launches, that accumulated interest gets added to your principal balance through a process called capitalization. You're suddenly paying interest on top of interest, which inflates your total costs.

Private lenders? They're all over the map. Some demand payments immediately after graduation or when you drop below half-time enrollment. Others copy the federal six-month timeline. A small handful extend grace periods to nine or even twelve months, though these arrangements are harder to locate. Your original promissory note contains your specific terms—track it down or call your lender if you're drawing a blank.

Author: Evan Thornton;

Source: sonicmusic.net

Here's something many borrowers overlook: making payments during your grace period is absolutely allowed, and there's no prepayment penalty. Targeting the interest on unsubsidized loans prevents capitalization from inflating what you owe. Even small payments can trim hundreds off your eventual total. Savvy borrowers spend these months hunting for jobs, building emergency funds, and getting familiar with their servicer's payment portal.

The student loan grace period before repayment eases your shift from student life to career mode, but it has quirks. If you re-enroll at half-time status or higher, the grace period clock stops ticking. Leave school again later, and you'll only have whatever time you didn't already use. Burned through two grace months before returning to campus? You'd have four months remaining after your next departure.

When Federal Student Loan Payments Begin

Direct Subsidized and Unsubsidized loans follow that six-month grace timeline. Your payment clock starts ticking roughly six months after you graduate, leave school entirely, or slip below half-time enrollment. The exact date depends on when your servicer processes your status change. Graduated on May 15th? Grace wraps up November 15th, and your first bill typically shows up around December 15th—servicers usually add a month-long billing cycle after grace ends.

Parent PLUS and Grad PLUS loans split into different categories. Parents borrowing PLUS loans technically enter repayment once the money's fully disbursed, but they can request deferment while their kid maintains half-time enrollment (plus six months afterward). Graduate students taking out Grad PLUS loans receive the standard six-month grace period after finishing their programs.

Perkins Loans—schools stopped issuing these in 2017, but some borrowers still carry them—include a nine-month grace period. If you're still paying off Perkins debt, repayment waits nine months after graduation or dropping below half-time. Your school or its designated servicer manages these loans, not the Department of Education's main servicers.

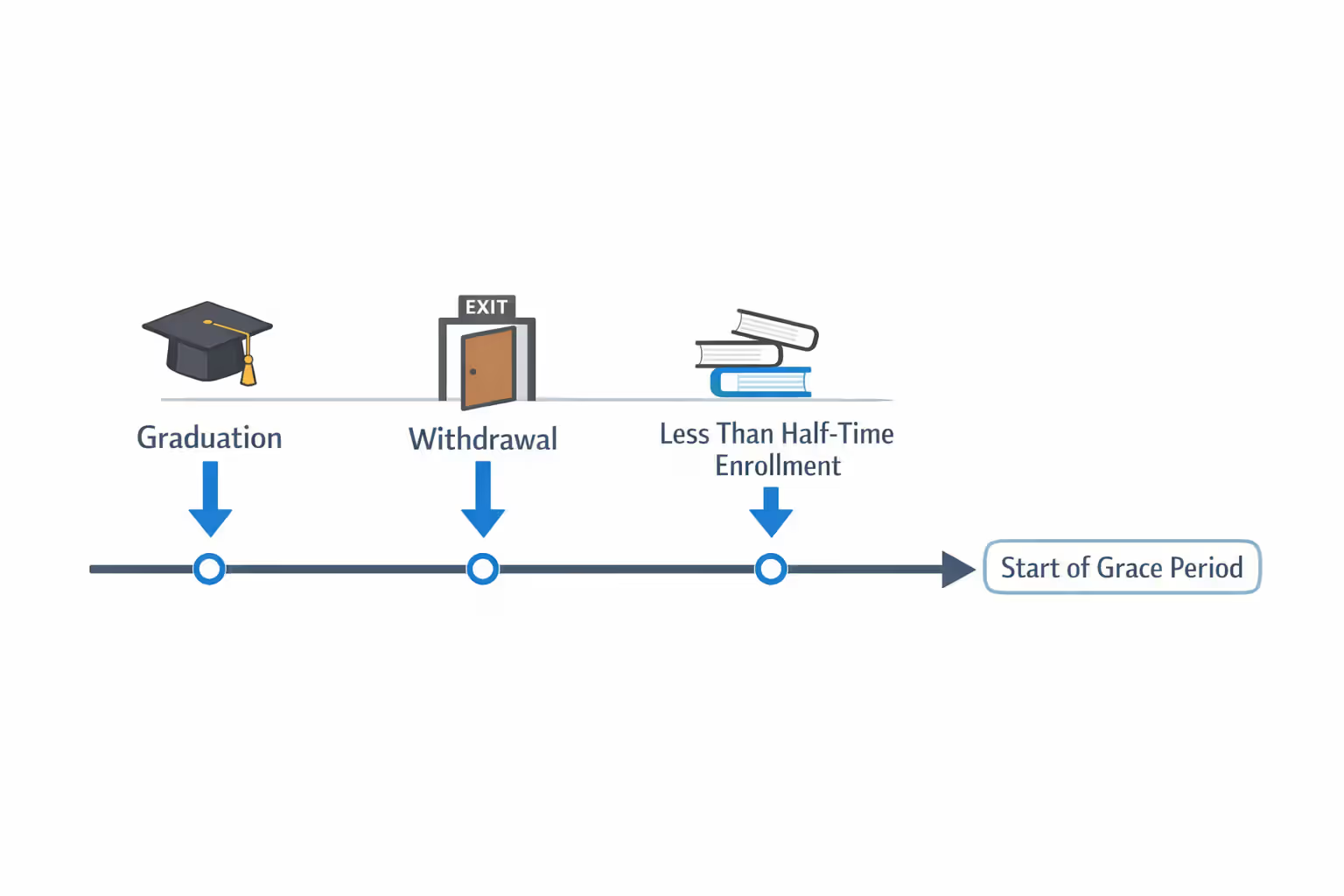

When does repayment begin for student loans? Specific events trigger it. Withdrawing mid-semester kicks off your grace period immediately, whether or not you plan to return. Graduating in December versus May shifts your first payment by six months. Dropping from full-time to part-time while staying above half-time enrollment? Grace stays dormant. Fall even one credit below half-time, and the countdown launches.

Consolidating federal loans during grace kills that payment-free window immediately. Your grace period vanishes the moment consolidation funds get disbursed. Thinking about consolidation? Weigh whether the benefits justify losing those remaining grace months.

When Private Student Loan Repayment Starts

Private lenders create their own policies, which produces massive variation across the market. Some require full principal-and-interest payments while you're still attending classes. Others let you pay interest only during school, then shift to full payments after you leave. Many provide deferred structures similar to federal options—you owe nothing until you exit campus.

When do you start paying student loans from banks and credit unions? Your promissory note locked in your answer when you first borrowed. Common setups include:

Immediate repayment: You start making full principal and interest payments shortly after the loan money arrives, potentially while you're mid-semester. Lenders typically charge lower interest rates for immediate repayment, but you need cash flow while studying.

Interest-only payments: You cover just the accumulating interest during enrollment, which stops your balance from growing. Full payments begin after leaving school, frequently without any grace period.

Partial interest payments: Fixed monthly amounts (often around $25) during school, which won't cover all the interest that's accumulating. Whatever you don't pay gets added to your principal when full repayment starts.

Full deferment: Zero payments while enrolled, with or without post-graduation grace. Interest keeps piling up and eventually capitalizes, creating the highest total cost but maximum cash flow flexibility now.

Private lenders don't agree on what "leaving school" means. Some start collection when you drop below full-time status, completely ignoring the half-time threshold that federal loans use. Others tolerate part-time enrollment without demanding payments. Taking a semester off but planning to return? Call your lender right away—you might need to request formal deferment or forbearance to stay current.

Grace periods for private loans range from nonexistent to nine months. Sallie Mae and Discover both offer six-month grace on many products. Citizens Bank provides nine months to some borrowers. College Ave and Ascent Financial vary depending on which specific product you borrowed and when you originally took out the loan.

Refinancing your private loans can wipe out or reset your grace period based on your new lender's policies. Approaching graduation while considering refinancing? Time your application carefully to keep your payment-free window intact.

What Triggers Your First Student Loan Payment

Specific documented events activate your first payment on student loans. For federal loans, the Department of Education tracks your enrollment through the National Student Clearinghouse—schools feed updates into this database regularly. When your status changes (graduation, withdrawal, enrollment below half-time), your servicer gets notified and calculates when grace ends.

Graduation has more nuance than you'd expect. Your grace period starts the day after your school officially confers your degree, which isn't necessarily your commencement ceremony date. School confers degrees May 20th but holds the ceremony May 15th? Grace begins May 21st.

Author: Evan Thornton;

Source: sonicmusic.net

Dropping below half-time kicks off repayment even if you're still enrolled in classes. For most undergrads, half-time status means six credit hours per semester. Graduate programs sometimes set different thresholds. Drop from seven to five credit hours partway through the term? Your grace period ignites immediately, and your school reports this within 30 days.

Withdrawing from school—whether formally or informally—launches your grace countdown. Informal withdrawal happens when you stop attending without completing official withdrawal paperwork. Your school determines your last attendance date and starts grace from there, which creates confusion for borrowers who thought they had more time.

When student loan payments start also depends on any deferment or forbearance you've used. You don't get a fresh grace period when postponement wraps up. Your payment typically lands 30 to 45 days after deferment or forbearance ends. Servicers mail billing statements at least three weeks before the payment arrives.

Loan consolidation instantly eliminates whatever grace period you have left. Consolidate three months into your grace window? You forfeit the remaining three months. Your new consolidation loan's first payment comes due within 60 days of disbursement.

Servicers calculate your first due date by adding your grace period to the triggering event, then generally tacking on one billing cycle. Graduate May 15th with six-month grace? Grace ends November 15th, and payment lands December 15th. That extra month gives servicers time to generate your first bill and lets you arrange payment logistics.

How to Find Your First Payment Due Date

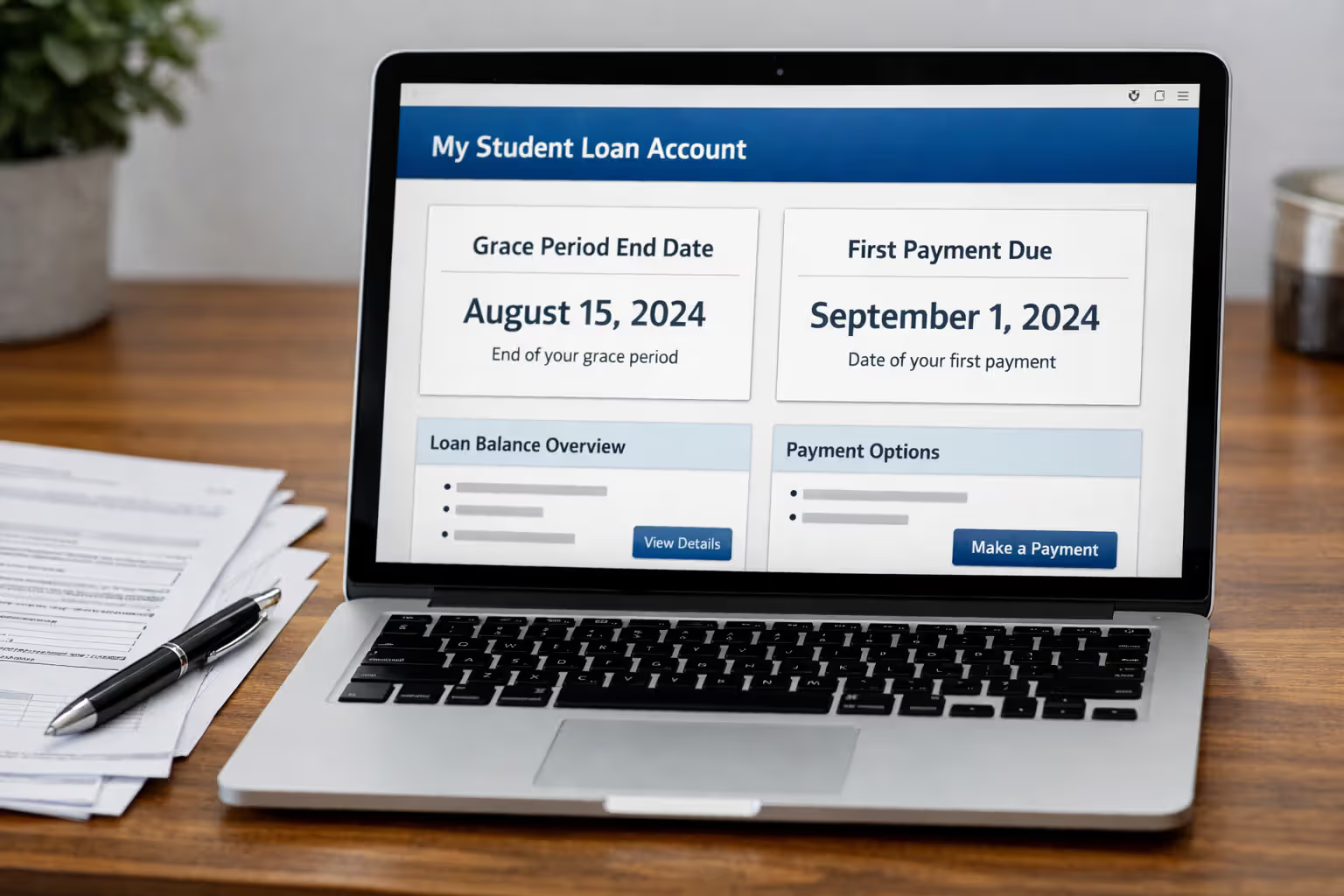

Don't guess at your payment deadline—track down the precise date. Begin by logging into your federal loan servicer's online portal. Your dashboard shows your current status, when grace ends, and your first payment deadline once it's been calculated. Federal servicers currently include MOHELA, EdFinancial, and Aidvantage, among others. Not sure who services your federal loans? Visit StudentAid.gov after signing in with your FSA ID.

Your loan disclosure statement—issued when you originally borrowed—spells out repayment terms including grace period length. Lost that paperwork? Request a replacement from your servicer. They're legally obligated to provide it upon request.

Author: Evan Thornton;

Source: sonicmusic.net

Contact your servicer directly if the online information looks incomplete or confusing. Call the customer service number printed on billing statements or their website. Ask specifically: "When does my grace period end, and what date is my first payment due?" Request written confirmation through email or their secure messaging system if possible.

For private loans, access your lender's borrower portal. Private lenders typically send payment reminders 30 to 45 days before your first payment hits. Haven't gotten any communication and graduation is only months away? Reach out immediately. Lenders sometimes hold outdated contact details, but communication breakdowns don't excuse missed payments.

Study your billing cycle carefully. Your first payment due date establishes your monthly deadline going forward. First payment due on the 15th? Future payments will generally land on the 15th every month. Some servicers let you change your due date after repayment begins if a different date lines up better with when you get paid.

Set up automatic payments as soon as you've confirmed your first deadline. Federal servicers reduce your interest rate by 0.25% when you enroll in auto-pay. Many private lenders offer similar discounts, usually between 0.25% and 0.50%. Beyond rate cuts, auto-pay prevents missed payments from simple forgetfulness.

This when does student loan repayment start guide approach—confirming dates early and setting up payment systems before your first deadline—prevents costly slip-ups and gives you room to correct any problems.

What Happens If You Miss Your First Payment

Missing your inaugural payment creates the same consequences as missing any later payment, but it's particularly damaging since servicers immediately flag you as a potential default risk.

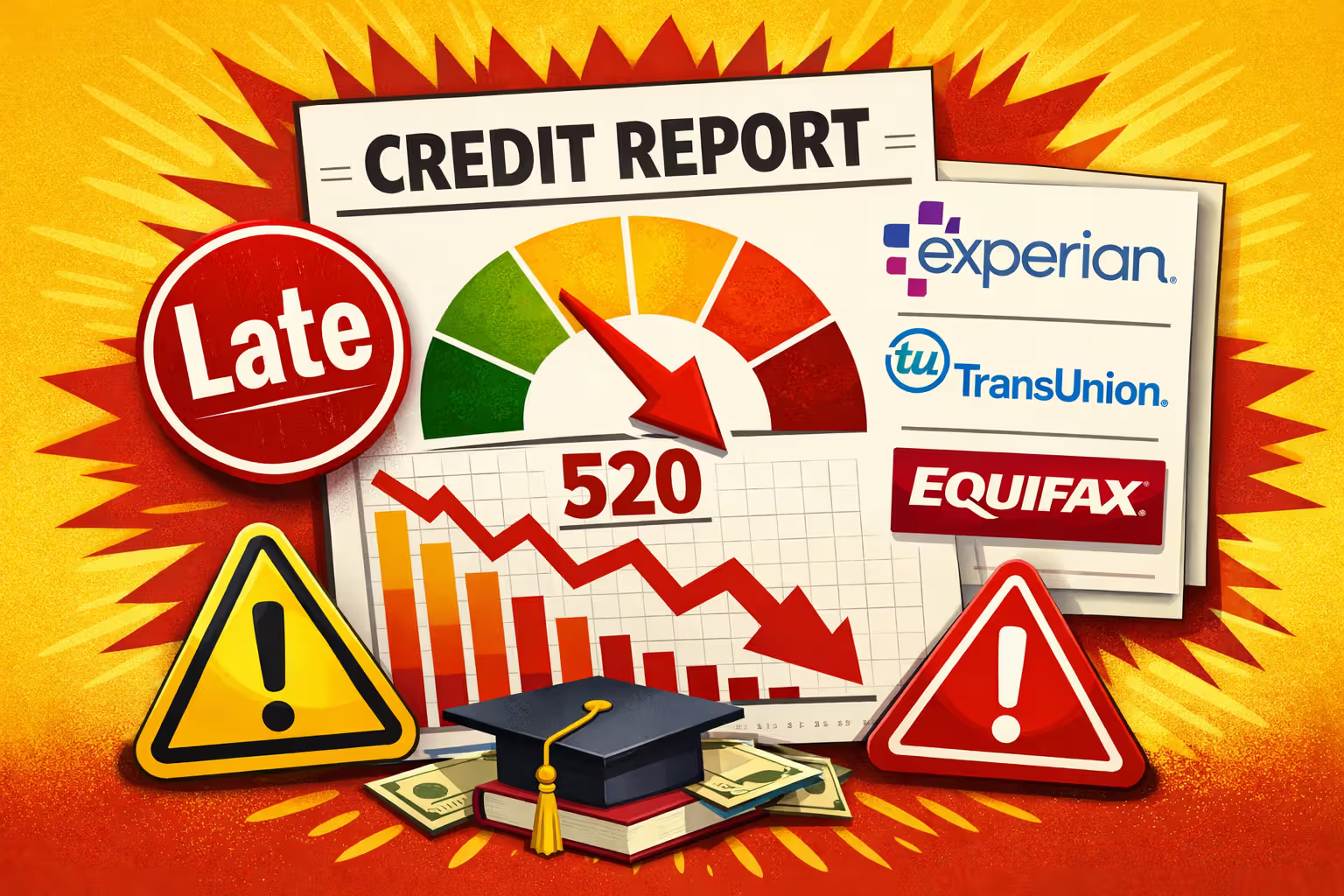

Federal loans become delinquent the day after you miss a payment. Your servicer will contact you through phone calls, emails, and postal mail demanding the overdue amount. You'll owe the missed payment plus late fees, typically 6% of the payment amount or $10—whichever is larger. Late fees cap at a maximum and only get charged once per missed payment.

Author: Evan Thornton;

Source: sonicmusic.net

After 30 days of delinquency, your servicer reports the late payment to all three major credit bureaus—Equifax, Experian, and TransUnion. This negative mark sticks on your credit report for seven years and can tank your credit score by 50 to 100+ points, depending on what else is in your credit history.

At 90 days delinquent, the late payment shows as a serious negative mark that severely damages your credit. Federal loans enter default at 270 days (nine months) of delinquency. Default consequences are devastating: your entire balance becomes immediately due, you lose access to deferment and forbearance, the government can garnish your wages without going to court, seize tax refunds, and withhold Social Security payments. Collection fees up to 16% of your principal and interest get added to what you owe.

Private loans generally default after 120 days of delinquency, though policies vary between lenders. Private lenders can file lawsuits for the full balance, secure judgments against you, and pursue aggressive collection methods. They'll also pursue co-signers, destroying their credit at the same time.

Can't afford your first payment by the deadline? Contact your servicer before the due date passes if possible. Federal servicers provide several options:

Switching repayment plans: Income-driven plans calculate your payment from your earnings and family size. Currently unemployed or earning very little? Your monthly payment might fall to $0 while keeping your loan in good standing.

Requesting deferment or forbearance: Facing unemployment, financial hardship, or medical emergencies? You might qualify to temporarily suspend payments.

Adjusting your due date: Shifting when payment is due each month to match your payday schedule can make payments easier to handle.

Private lenders offer fewer flexible alternatives but might grant short-term forbearance or modified payment arrangements. Some allow temporary interest-only payments or extend your loan term to lower monthly amounts.

Never ignore a missed payment. The faster you address it, the more solutions remain available and the less damage hits your credit and financial standing.

The grace period is your financial runway—use it to prepare for takeoff, not to ignore what's coming. Borrowers who engage with their servicers early and understand their repayment start date are significantly less likely to default in their first year of repayment

— Mark Kantrowitz

Frequently Asked Questions About Student Loan Repayment Start Dates

Pinpointing exactly when your student loan repayment begins hands you control over your financial shift from campus to career. Federal loans typically include six-month grace, while private lenders create varied terms that require individual verification. Your first payment date pivots on when you leave school, your enrollment status, and which specific loan types you hold.

Mark your grace period end date on your calendar the moment you leave school. Set up your servicer portal login, activate automatic payments, and consider making voluntary payments during grace to cut interest costs. If your financial picture changes before your first payment arrives, reach out to your servicer right away to explore alternatives like income-driven plans or temporary deferment.

The consequences of missed payments are severe and long-lasting, but they're completely avoidable with proper preparation. Use your grace period to build a budget, find employment, and establish payment systems that keep your loans current from day one.

Your student loan repayment journey starts with knowing precisely when that first payment arrives. With the information in this when does student loan repayment start explained resource, you're equipped to navigate the transition confidently and protect both your credit and your financial future.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.