Young person sitting at a desk with a laptop reviewing student loan repayment options in a bright home office with documents and calculator nearby

What Is the SAVE Plan for Student Loans?

SAVE—which stands for Saving on a Valuable Education—arrived in 2023 as the Department of Education's answer to borrower complaints about previous income-driven repayment options. Think of it as REPAYE's more generous successor, built specifically to address the balance growth and high payment issues that plagued earlier programs.

Here's what makes SAVE different: if you borrowed money for undergrad, you'll pay just 5% of your discretionary income instead of the old 10% rate. The government also changed how they define "discretionary income" in your favor, protecting more of your paycheck from payment calculations. And unlike older plans where your balance could grow even while making payments, SAVE covers unpaid interest so your debt doesn't snowball.

Since the program opened enrollment, over 8 million federal loan borrowers have switched to SAVE or enrolled directly. That uptake reflects real improvements in how payments get calculated and how quickly you can reach forgiveness.

How the SAVE Plan Works

Payment calculations under SAVE work differently than the standard 10-year plan most borrowers start with. Instead of dividing your total loan balance by 120 months, your monthly bill connects directly to what you're actually earning.

Payment Calculation Formula

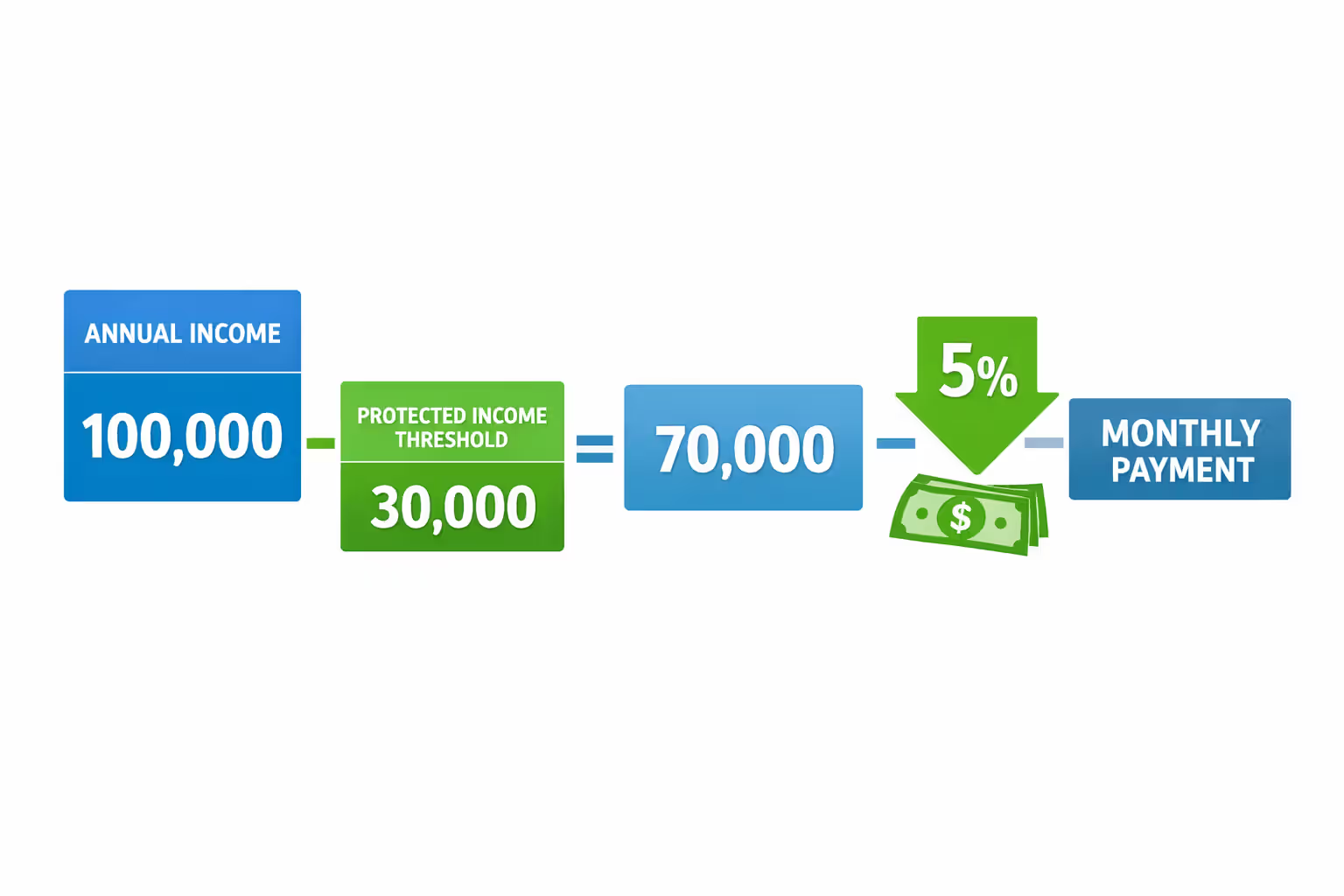

Your payment gets calculated from discretionary income—everything you earn above 225% of the federal poverty guideline for your household size. That's a major shift from the 150% threshold used in IBR and PAYE, which meant those plans counted more of your income as "available" for loan payments.

Here's a concrete example: In 2026, the federal poverty guideline for a single person sits at $15,060. Multiply that by 2.25, and you get $33,885. If you're earning $45,000 per year, your discretionary income equals $11,115 ($45,000 minus $33,885). With undergraduate loans only, you'll pay 5% of that amount annually—about $556 for the year, or roughly $46 per month.

Author: Evan Thornton;

Source: sonicmusic.net

Graduate loans carry a 10% rate instead. Borrowed for both undergrad and graduate school? Your payment gets calculated proportionally based on the mix.

Interest Subsidy Protection

Here's where the save plan student loans explained gets really important: SAVE includes a complete interest subsidy that previous plans didn't offer.

Let's say you have $50,000 in federal loans at 5% interest. Each month, about $208 in interest accrues. But your income-driven payment under SAVE comes out to only $100 monthly because your income is relatively low. In older plans like IBR or PAYE, that unpaid $108 would get added to your principal balance—you'd watch your debt grow despite making payments.

SAVE eliminates that nightmare. The government covers that $108 shortfall. Your balance stays frozen at $50,000 as long as you make your required payments, even when that payment is $0 due to very low income.

Forgiveness Timeline

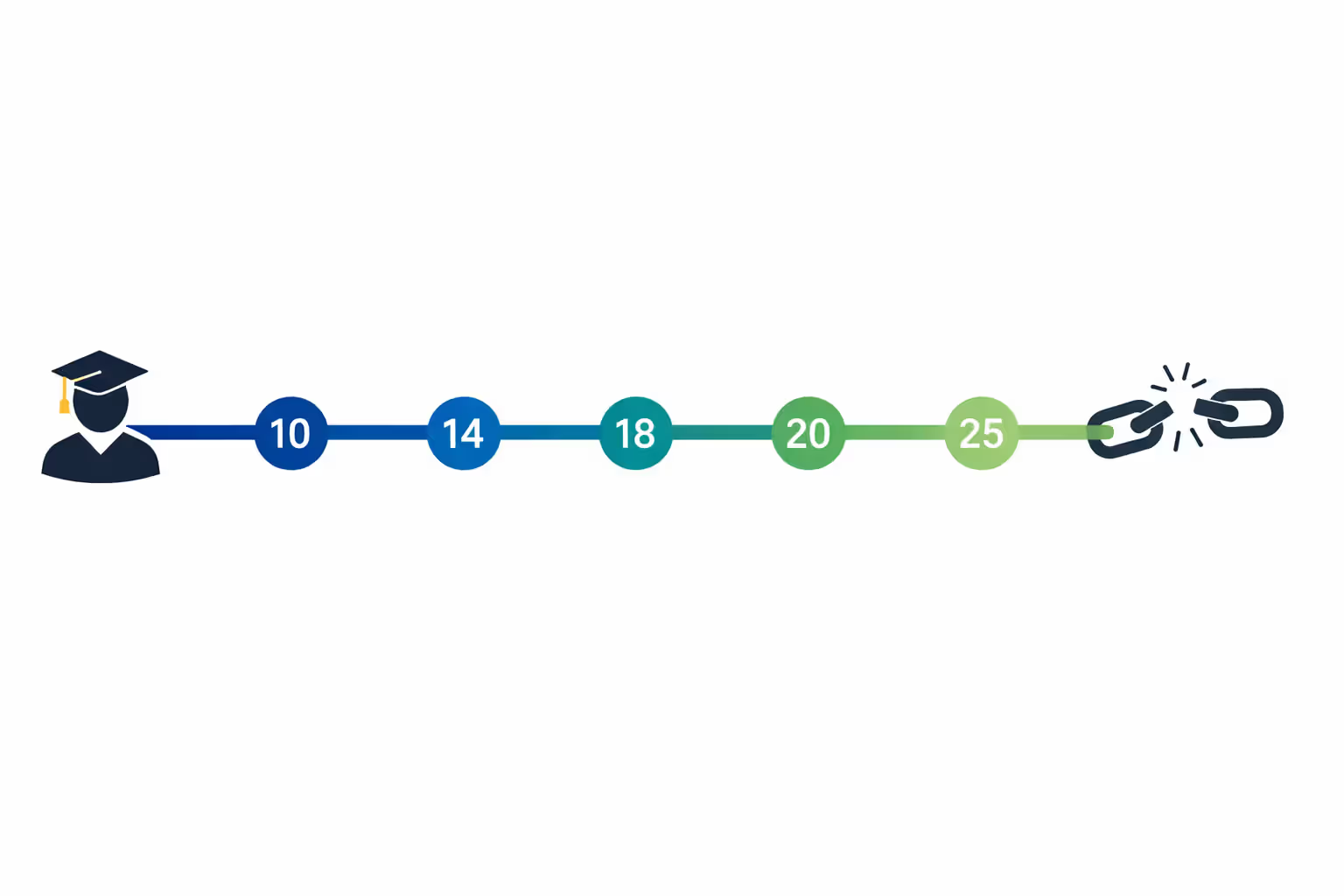

SAVE forgives remaining debt after different timelines depending on your original borrowed amount. If you initially borrowed $12,000 or less, forgiveness happens after just 10 years of qualifying payments.

For every additional $1,000 you borrowed beyond that $12,000 threshold, tack on another year—up to the maximum of 20 years for undergraduate debt or 25 years for graduate loans.

Someone who borrowed $16,000 total would reach forgiveness after 14 years (10 base years plus 4 additional years for the $4,000 over the threshold). This accelerated timeline particularly helps community college graduates, certificate program completers, and students who attended school briefly but left with debt.

Author: Evan Thornton;

Source: sonicmusic.net

Who Qualifies for the SAVE Repayment Plan

Not every education loan qualifies for SAVE. The student loan save plan exclusively covers federal Direct Loans—the lending program that's been issuing new federal loans since 2010.

Loan Types That Qualify

Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans for graduate students, and Direct Consolidation Loans all work with SAVE. The key word in all those is "Direct."

Got older loans from the FFEL (Federal Family Education Loan) program or Perkins Loans? Those don't qualify automatically. You'll need to combine them into a Direct Consolidation Loan first. Contact your servicer to start that process—it typically takes 30-60 days.

Parent PLUS loans hit a wall here. Even consolidation won't make them eligible for SAVE. Parents who borrowed for their children's education get stuck with either the Income-Contingent Repayment plan or standard repayment options. Graduate PLUS loans—borrowed by students themselves for graduate school—do qualify, though they're subject to the 10% payment rate rather than 5%.

Income Requirements

There's no income cutoff preventing you from using SAVE. Earn $20,000? You qualify. Earn $200,000? You still qualify, though your payment will be substantially higher and you might not benefit from the program.

SAVE adjusts to whatever you're earning. Payments recalculate annually when you submit updated income information. Someone earning $30,000 with $60,000 in debt sees dramatic payment reduction. A high earner might actually pay more than the standard 10-year plan amount—but they're never required to pay more than they would under standard repayment.

Your updated income gets reported through tax return data you authorize the IRS to share, or through alternative documentation like pay stubs if your income dropped recently or you don't file tax returns.

Family Size Considerations

Every person in your household reduces your discretionary income calculation because poverty guidelines increase with household size. The difference is substantial.

A single borrower earning $40,000 has one poverty guideline threshold. Add a spouse and two kids to that same $40,000 income, and the protected income threshold jumps significantly—potentially reducing the monthly payment by $150 or more.

Count yourself, your spouse if married, and any children you support financially—whether or not they live with you full-time. Don't count parents you live with unless you're actually providing more than half their financial support. Don't count roommates.

You can update family size at your annual recertification or whenever you have a qualifying change: marriage, divorce, birth, adoption, or a dependent leaving your household.

SAVE Plan vs Other Income-Driven Repayment Plans

Three other income-driven plans still exist, though the Department of Education stopped accepting new REPAYE and PAYE enrollments when SAVE launched. Comparing these programs shows why the save repayment plan became the preferred option for most borrowers.

| Plan | How Payments Get Calculated | Forgiveness Timing | Interest Coverage | How Spousal Income Gets Treated |

| SAVE | Undergraduate: 5% of discretionary income Graduate: 10% of discretionary income | Undergraduate: 10-20 years Graduate: 10-25 years | Government covers 100% of interest your payment doesn't | Excluded when filing separately |

| REPAYE | 10% of discretionary income across all loan types | Undergraduate: 20 years Graduate: 25 years | Government covers 50% of unpaid interest on subsidized loans, 50% on unsubsidized | Always included no matter how you file taxes |

| IBR | 10% or 15% of discretionary income (depends on when you first borrowed) | 20-25 years depending on loan origination date | No coverage—unpaid interest gets added to balance | Excluded when filing separately |

| PAYE | 10% of discretionary income | 20 years across all loan types | No coverage except subsidized loans for first 3 years | Excluded when filing separately |

SAVE's advantages jump out in this comparison. The 5% undergraduate rate cuts payments in half compared to every other plan. Complete interest coverage prevents balance growth. Faster forgiveness for smaller balances helps borrowers who attended school briefly or went to community college.

One consideration for married borrowers: SAVE counts spousal income when you file jointly, similar to how REPAYE operated. Filing separately excludes spousal income but usually increases your combined tax bill. Calculate both scenarios—your SAVE payment plus taxes when filing jointly versus filing separately—before committing to a filing status.

How to Apply for the SAVE Program Student Loans

Enrolling in the save program student loans takes about 10 minutes if you have your information ready. You'll handle everything through the Federal Student Aid website rather than calling your loan servicer.

Step-by-Step Application Process

Start by gathering what you'll need: your FSA ID and password, Social Security number, email address and phone number, current family size, and your most recent tax return information. If your income dropped significantly since your last tax filing—layoff, reduced hours, career change, extended medical leave—grab recent pay stubs instead.

Head to StudentAid.gov and sign in using your FSA ID. Navigate to "Manage Loans" and look for the repayment plan section. Select "Apply for Income-Driven Repayment" and choose SAVE from the plan options.

Author: Evan Thornton;

Source: sonicmusic.net

Enter your family size carefully—this number directly impacts your payment. Include yourself, your spouse (if married), children you support, and other dependents you claim on taxes. Roommates don't count. Parents you live with don't count unless you're supporting them financially.

For income documentation, authorize the IRS to share your tax data automatically if possible. This speeds up processing and reduces errors. The system pulls your most recent return and populates the income fields. Can't use automatic import? You can manually enter income information or upload your tax return.

The application shows an estimated payment before you submit. This isn't your final payment—your servicer calculates that officially—but it's typically accurate within $5-10.

Required Documentation

Most borrowers complete the entire application using IRS data retrieval without uploading anything. The exception: if your financial situation changed dramatically since your last tax return.

Lost your job three months ago? Provide a termination letter and recent pay stubs from any new employment (or a statement that you're currently unemployed). Took a lower-paying job? Recent pay stubs showing your new income level work.

Self-employed? Your most recent tax return works, but if you're newly self-employed or income fluctuates dramatically, you might provide a signed statement projecting your expected annual income based on year-to-date earnings.

Recertification Requirements

Every single year, you must recertify—submit updated income and family size information. Your servicer emails reminders starting about 90 days before your deadline, then again at 60 days, 30 days, and right before the deadline.

Miss this deadline and two bad things happen immediately: your payment jumps to whatever you'd pay under standard 10-year repayment (often $300-500+ more per month), and all unpaid interest capitalizes—gets permanently added to your principal balance.

Set a phone reminder for 60 days before your annual recertification date. The actual recertification takes about five minutes when you use IRS data retrieval for updated income.

Timeline

Applications typically process within 2-4 weeks, occasionally faster. While your application is processing, you'll stay in whatever repayment plan you're currently using. Your servicer will send a notification once SAVE is approved, showing your new payment amount and the date your first SAVE payment is due.

Switching from another income-driven plan to SAVE happens seamlessly—all your previous qualifying payments count toward forgiveness. If you're currently in forbearance or standard repayment, expect your first SAVE payment within 30-45 days after approval.

Benefits and Drawbacks of the SAVE Student Loan Plan

Every save plan student loans guide should lay out both sides. SAVE offers genuine improvements over older plans, but it's not perfect for everyone.

Key Benefits

Lower Monthly Payments

The 5% rate for undergraduate loans represents a 50% payment reduction compared to older 10% plans. Take someone earning $35,000 annually with a family size of one. Under SAVE, they'd owe roughly $46 monthly. Under IBR or PAYE at 10%? Around $92 monthly.

That $46 difference doesn't sound enormous until you multiply it out over years. Over a 20-year repayment period, that's an extra $11,040 in your pocket rather than going to loan payments.

The 225% poverty guideline threshold amplifies this benefit. More of your income gets protected from payment calculations. In 2026, single borrowers earning up to $33,885 owe $0 monthly—they stay in repayment but don't pay anything, and the government covers all their accruing interest.

Balance Protection

The complete interest subsidy solves the single most demoralizing problem with older income-driven plans: watching your balance grow despite making payments.

Under IBR or PAYE, borrowers regularly saw their $40,000 in loans grow to $50,000, then $60,000 over years of consistent payments. Why? Their income-driven payment didn't cover monthly interest accrual, and that unpaid interest got added to the principal.

SAVE eliminates that entirely. Make your required payment—even if that payment is $0—and the government covers whatever interest your payment doesn't. Your balance stays frozen or decreases. You won't be in worse shape after five years of payments than when you started.

Author: Evan Thornton;

Source: sonicmusic.net

Faster Forgiveness for Smaller Balances

The 10-year forgiveness timeline for original balances of $12,000 or less specifically helps community college students, certificate program graduates, and people who started degrees but didn't finish.

Someone who attended community college for two years, borrowed $10,000, and then entered the workforce can reach forgiveness in just 10 years. Compare that to 20-25 years under other income-driven plans.

Even borrowers with slightly higher balances benefit: $15,000 borrowed gets forgiveness after 13 years. $20,000 borrowed means 18 years. The sliding scale timeline beats the flat 20-25 year requirement of older plans.

Simplified Spousal Income Treatment

Unlike REPAYE—which always counted spousal income regardless of how you filed taxes—SAVE excludes spousal income when you file separately. This gives married borrowers actual control over whether their spouse's earnings affect their payment.

Filing separately does usually increase your combined tax bill, but at least you can run both scenarios and choose whichever saves you more money overall.

Potential Disadvantages

Longer Repayment for Large Balances

If you borrowed more than $12,000, you're looking at potentially 20-25 years of payments before reaching forgiveness. That's a significant chunk of your adult life dealing with loan recertification, income documentation, and servicer communication.

Some borrowers with stable incomes and the ability to pay more each month might save money in total interest by paying loans off in 5-10 years under standard repayment rather than stretching payments over two decades.

Tax Implications of Forgiveness

Through 2025, student loan forgiveness under federal programs isn't taxed as income. The American Rescue Plan Act created that exemption. But Congress hasn't extended it past 2025.

Starting in 2026—under current law—forgiven student debt counts as taxable income. If you reach forgiveness with $60,000 remaining and you're in the 22% federal tax bracket, you'll owe roughly $13,200 in federal taxes that year. State taxes could add another $2,000-4,000 depending where you live.

That tax bomb isn't necessarily worse than paying off the debt, but you need to plan for it. Set aside money in a high-yield savings account as you approach forgiveness so you're not caught off guard.

Annual Recertification Burden

Remembering to recertify every single year for 20+ years adds administrative hassle. Miss your deadline once and you'll face dramatically higher payments plus interest capitalization.

For borrowers who move frequently, change jobs often, or simply struggle with administrative tasks, the annual requirement creates ongoing stress. Set calendar reminders, bookmark the StudentAid.gov recertification page, and update your contact information with your servicer whenever you move.

Payment Increases with Income Growth

Your payment adjusts upward as your income rises. Early-career professionals might pay $50-75 monthly, but after several promotions or career advancement, that same borrower could see payments of $250-400 monthly.

While the payment reflects your ability to pay, it can feel frustrating when salary increases get eaten up by higher loan payments. A $10,000 raise with the 5% rate means roughly $42 more per month in loan payments ($10,000 × 5% ÷ 12 months). With the 10% graduate rate, that same raise costs you $83 more monthly.

The SAVE plan represents the most borrower-friendly income-driven repayment option the federal government has ever offered. The combination of lower payments, interest subsidies, and accelerated forgiveness for smaller balances addresses the most common complaints about earlier programs. However, borrowers should carefully consider whether pursuing forgiveness over 20-25 years makes financial sense compared to aggressive repayment, especially given uncertainty around the tax treatment of forgiven balances

— Mark Kantrowitz

Common Questions About the SAVE Plan

SAVE offers federal student loan borrowers the most favorable repayment terms available in 2026. The 5% undergraduate payment rate, complete interest coverage preventing balance growth, and forgiveness timelines starting at just 10 years for smaller balances address major weaknesses in previous income-driven plans.

Whether SAVE makes sense for you depends on your specific situation—income level, total debt, household size, and long-term financial plans. Borrowers earning less relative to their debt get the most benefit from reduced payments and balance protection. Higher earners or those with smaller balances might pay less total interest by aggressively paying off loans in 5-10 years instead.

The application process through StudentAid.gov is straightforward, and borrowers switching from another income-driven plan keep all their progress toward forgiveness. Just don't forget the annual recertification requirement—that single missed deadline can trigger higher payments and interest capitalization that undoes months of planning.

Before enrolling, calculate your projected SAVE payment and compare it to what you'd pay under standard repayment. Think about how long you'll be making payments and whether potential future tax liability on forgiven balances outweighs the benefit of lower monthly payments. For many borrowers, SAVE provides a realistic path to managing federal student debt without sacrificing other financial priorities like emergency savings, retirement contributions, or homeownership.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.