Young person sitting at kitchen table with laptop and paper bills calculating student loan payments in a small apartment

IDR Student Loan Guide for Federal Borrowers

Content

Content

Your federal student loan bill hits every month like clockwork, but your paycheck? That's the variable nobody warns you about when you're signing loan paperwork at 19. Maybe you're three years into a nonprofit job making $38,000 with $75,000 in loans. Maybe your standard payment is $863, but rent is $1,400 and you're eating ramen four nights a week.

That's where income-driven repayment enters the picture. Over 9 million Americans currently use these plans to keep their loans current without choosing between debt payments and actual necessities. But here's the thing—the four different plan types, the poverty guideline calculations, the recertification deadlines, the interest quirks? The federal websites explain the rules without helping you figure out which rules actually matter for your money.

This walkthrough covers how these plans actually function when you're the one making the payments, not just how they look on paper.

What Is an IDR Plan for Student Loans?

Think of income-driven repayment as a contract that says "your monthly payment can't exceed X% of what you earn after covering basic living expenses." Instead of owing a fixed amount determined by your total debt, your bill flexes based on two numbers that change: your income and your household size.

The Department of Education runs these programs for federal loans only. Here's the core difference from standard repayment: a fixed 10-year schedule might charge you $650 monthly whether you're earning $32,000 or $72,000. Under an IDR plan, that same loan portfolio could cost you $80 at the lower income and $420 at the higher one.

Your payment gets recalculated every 12 months. Lost your job? Next year's payment drops—potentially to zero. Got a raise? Your payment increases, but proportionally to your actual financial improvement, not some arbitrary schedule set a decade ago.

The catch: stretching payments over 20 or 25 years means interest accumulates longer. But if your current choice is between an unaffordable payment and default, that trade-off makes sense. Whatever balance remains after those two decades gets wiped away, assuming you've stayed enrolled and certified your income annually.

Private loans don't touch these programs. Neither do federal loans you refinanced into private ones. This matters more than borrowers expect—refinancing for a lower rate might save you 1.5% in interest but costs you the entire safety net of income-driven repayment. That's a permanent decision, not a test drive.

Types of IDR Plans Available

Four distinct programs exist, each with its own formula for calculating what you owe. The newest plan offers the best terms for most people, but eligibility restrictions and loan types determine whether you can actually use it.

SAVE Plan (formerly REPAYE)

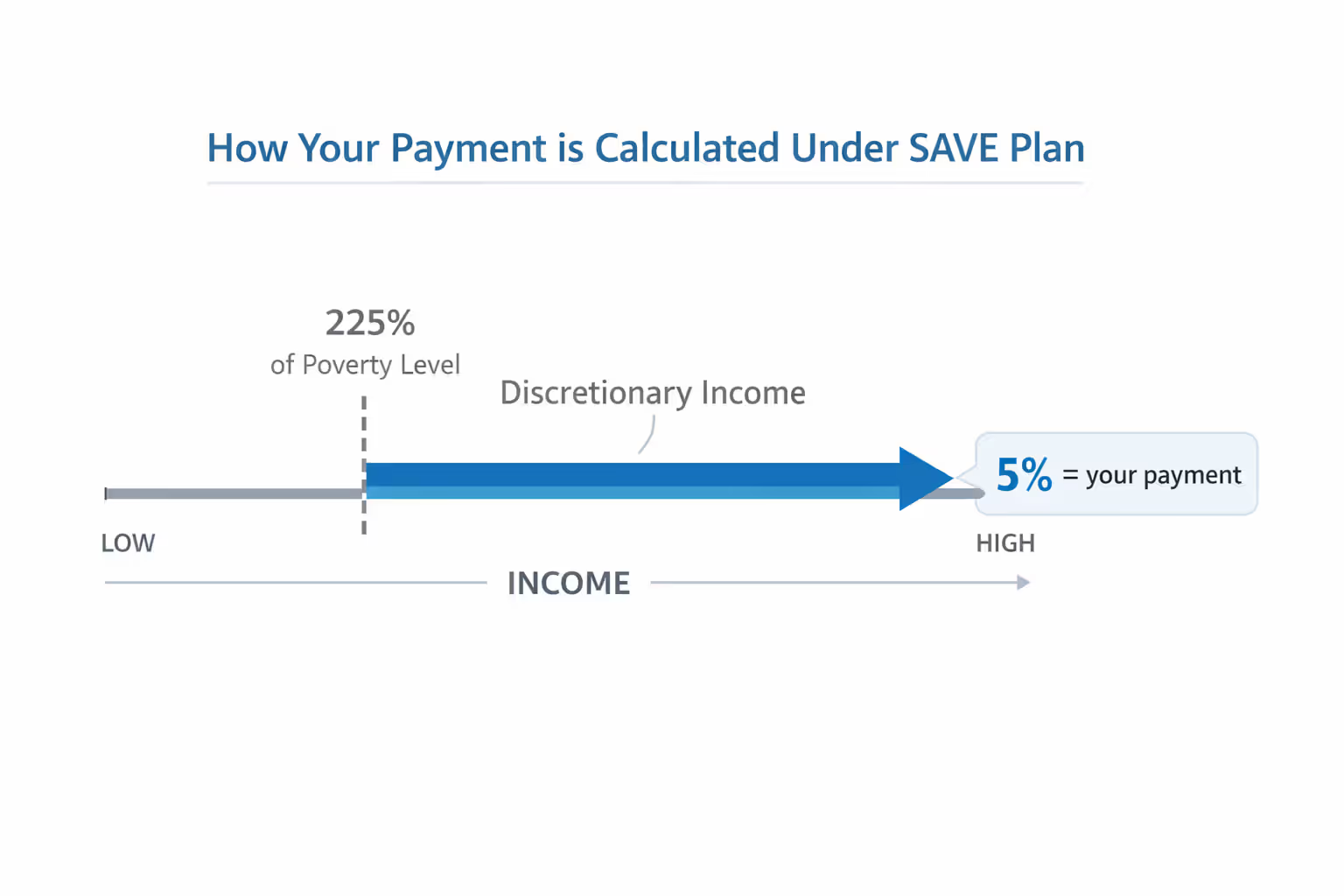

The Saving on a Valuable Education plan launched in 2023 as the successor to REPAYE, and it's structured to help undergraduate borrowers most aggressively. If all your loans funded undergrad, you'll pay 5% of discretionary income. Graduate debt bumps that to 10%. Hold both types? You'll pay a blended rate proportional to your balances.

Here's where it gets interesting: SAVE defines discretionary income as anything you earn above 225% of poverty guidelines. That's substantially higher than the 150% threshold older plans use. Translation: more of your income stays protected, which lowers your payment.

The poverty guideline for a single person in the lower 48 states sits around $15,060 in 2026. Multiply that by 2.25 and you get $33,885. Earn $40,000? Your discretionary income is $6,115, and 5% of that is $306 annually—about $25 monthly. Earn $33,000? You're below the threshold, so your payment is zero.

SAVE also blocks runaway interest. If your payment is $25 but $60 in interest accrues that month, the government covers that $35 gap. Your principal never grows beyond what you originally borrowed, even if you're making tiny payments for years.

Undergraduate-only borrowers hit forgiveness at 20 years. Anyone with graduate debt waits 25 years, regardless of how much graduate vs. undergraduate debt they carry. Married borrowers filing taxes separately can exclude their spouse's income from calculations—something older plans don't universally allow.

Author: Olivia Harrington;

Source: sonicmusic.net

Income-Based Repayment (IBR)

IBR splits into two versions based on one date: July 1, 2014. Borrowed your first loan on or after that date? You'll pay 10% of discretionary income and reach forgiveness after 20 years. Borrowed before? You're looking at 15% with a 25-year timeline.

Both versions measure discretionary income against 150% of poverty guidelines—a tougher standard than SAVE's 225%. Using the same single-person example, 150% of $15,060 equals $22,590. That $40,000 earner now has $17,410 in discretionary income. At 10%, that's $1,741 annually, or $145 monthly. Same income, much higher payment than SAVE.

This plan works with both Direct Loans and older FFEL loans, making it the go-to option for borrowers still carrying FFEL debt who haven't consolidated. Parent PLUS loans stay excluded.

IBR includes a ceiling: your payment never exceeds what you'd owe under standard 10-year repayment. So if your income skyrockets and the 10% calculation would charge you $800 monthly, but your standard payment is $620, you're capped at $620. High earners essentially revert to standard terms without formally leaving the program.

Pay As You Earn (PAYE)

PAYE mirrors the newer IBR terms—10% of income above 150% poverty guidelines, 20-year forgiveness—but gates eligibility aggressively. You qualify only if you took out your first federal loan after September 30, 2007, AND received at least one disbursement after September 30, 2011. Miss either date and you're locked out.

This narrow window exists because PAYE launched as a pilot program for recent borrowers before the government expanded access through IBR changes. If you qualify for both, they're functionally identical in payment calculations and timeline.

The standard payment cap applies here too. Married borrowers filing separately can shield spousal income from calculations, though you'll pay more in taxes for that privilege. Parent PLUS loans remain ineligible—parents get no access to PAYE regardless of their circumstances.

PAYE's main value proposition in 2026: borrowers in that 2007-2011 window who don't qualify for SAVE due to loan type restrictions might find this their best available option.

Income-Contingent Repayment (ICR)

ICR, launched in 1995, uses the harshest formula: 20% of discretionary income (measured against 100% of poverty guidelines, not 150% or 225%) OR what you'd pay on a 12-year fixed schedule adjusted by income—whichever costs less. Forgiveness arrives after 25 years.

That $40,000 earner from earlier examples would face $25,000 in discretionary income ($40,000 minus 100% of the $15,060 poverty guideline). Twenty percent of $25,000 is $5,000 annually—$417 monthly. That's nearly 17 times the SAVE payment for the same person.

Why does ICR still exist? Parent PLUS loans. Parents can't use SAVE, IBR, or PAYE. But consolidate a Parent PLUS loan into a Direct Consolidation Loan, and suddenly ICR becomes available. For a parent earning $55,000 with $40,000 in Parent PLUS debt, ICR might be the only path to avoid default beyond standard repayment or extended repayment plans.

Most direct borrowers (students borrowing for their own education) find ICR obsolete—it consistently produces higher payments than SAVE or IBR. But for that specific Parent PLUS scenario, it remains relevant.

How IDR Plans Calculate Your Monthly Payment

Start with your adjusted gross income from last year's tax return—the number on line 11 of your 1040. Your servicer looks up the federal poverty guideline for your state and family size, multiplies it by the plan's threshold percentage (100%, 150%, or 225% depending on plan), then subtracts that from your AGI. What's left is "discretionary income."

Take that discretionary income, multiply it by your plan's payment percentage, divide by 12, and you've got your monthly bill.

Real example: You're in Texas, married, with one kid. Your AGI is $62,000. The three-person poverty guideline is roughly $25,820. Under SAVE's 225% threshold, your protected income is $58,095. Your discretionary income: $62,000 - $58,095 = $3,905. You have only undergraduate loans, so you'll pay 5% of that amount annually: $195.25, which breaks down to about $16 monthly.

Now rerun that under IBR at 150% and 10%. Protected income drops to $38,730. Discretionary income jumps to $23,270. Ten percent of that is $2,327 annually—$194 monthly. Same family, same income, twelve times the payment just from plan mechanics.

Family size hits these calculations hard. That couple adds a second child? Their three-person household becomes four. The poverty guideline rises to roughly $31,200. Under SAVE, 225% of that is $70,200—higher than their $62,000 income. Discretionary income becomes zero. Payment becomes zero.

Married borrowers face a puzzle. File jointly and both incomes get counted (except under ICR, which counts spousal income regardless). File separately under SAVE or PAYE and only your income matters, but you'll lose tax benefits like the $27,700 standard deduction for joint filers, instead taking two $13,850 single deductions. Sometimes the payment savings justify the tax cost. Sometimes they don't. You need to run both scenarios with actual numbers, not guess.

Your servicer recalculates this entire formula when you recertify annually. Your income probably changed. Maybe your family size changed. Your payment adjusts accordingly—up, down, or straight to zero if life went sideways.

Who Qualifies for IDR Student Loans

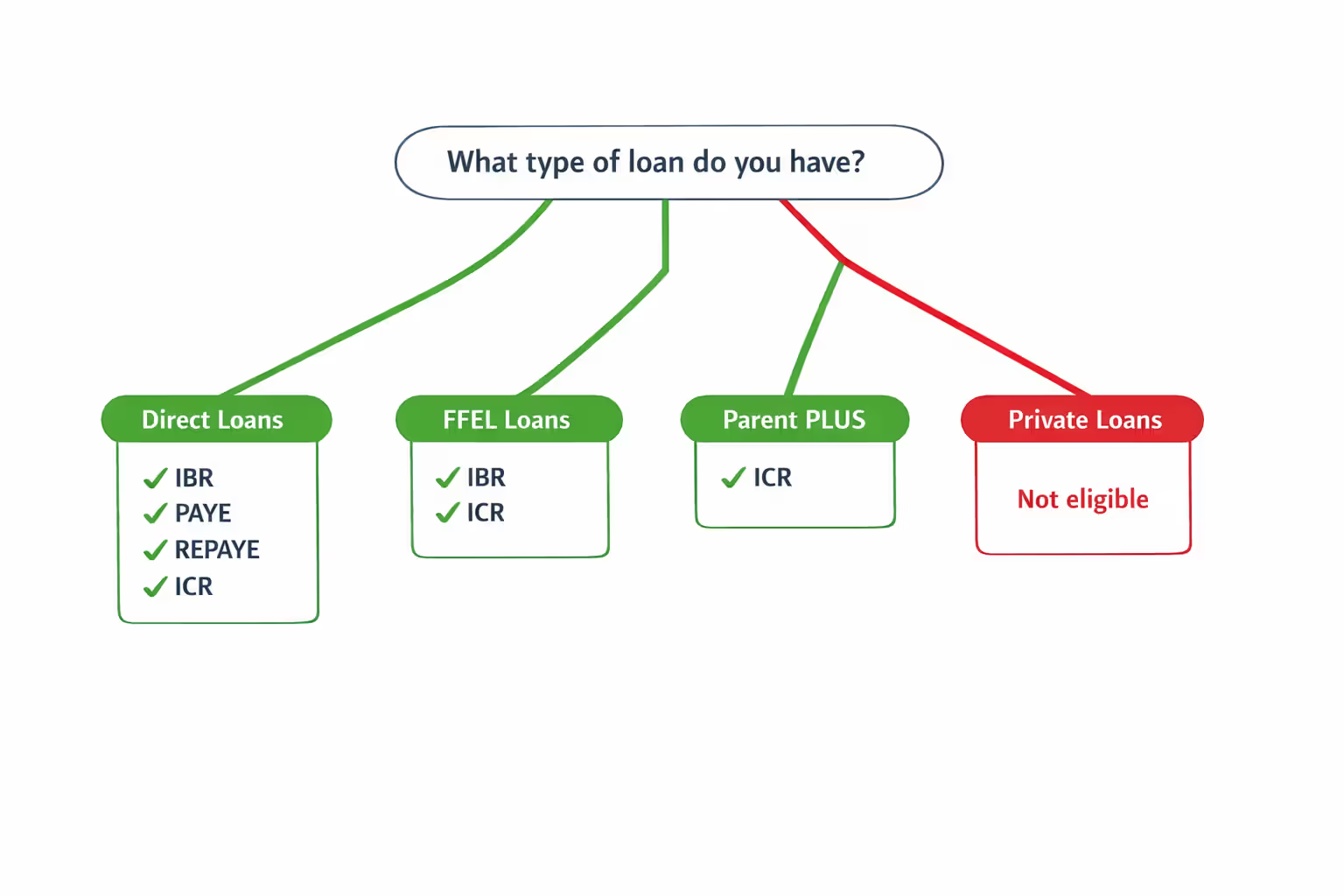

Direct Loans from the federal government automatically qualify for all plans based on when you borrowed. Direct Subsidized, Direct Unsubsidized, Direct PLUS for graduate students, Direct Consolidation Loans—they're all in, though specific plans exclude specific loan types.

Older FFEL loans (Federal Family Education Loans) work with IBR and ICR but not SAVE or PAYE. Millions of borrowers still carry FFEL debt from before the 2010 switch to Direct Lending. You can consolidate FFEL loans into a Direct Consolidation Loan to unlock all four plans, but consolidation restarts your forgiveness clock at year zero. If you've already made eight years of payments, you're trading those eight years of progress for access to better terms going forward.

Parent PLUS loans live in their own restrictive category. SAVE, IBR, and PAYE won't touch them. Parents must consolidate into a Direct Consolidation Loan first, which then qualifies for ICR only. That's it—that's the entire income-driven universe for parent borrowers.

Perkins Loans need consolidation too. They existed as a separate program and don't qualify for IDR as-is.

Private loans never qualify, period. You borrowed from Discover, SoFi, Sallie Mae, a credit union? Those lenders operate outside federal programs entirely. Refinancing federal loans with private lenders to chase lower interest rates permanently exits you from IDR eligibility. That's a one-way door—you can't refinance back into federal status.

Defaulted loans need rehabilitation before any IDR application processes. Nine months of consecutive on-time payments under a rehabilitation agreement brings them current. Then you can apply for income-driven repayment.

Author: Olivia Harrington;

Source: sonicmusic.net

How to Apply for an IDR Plan

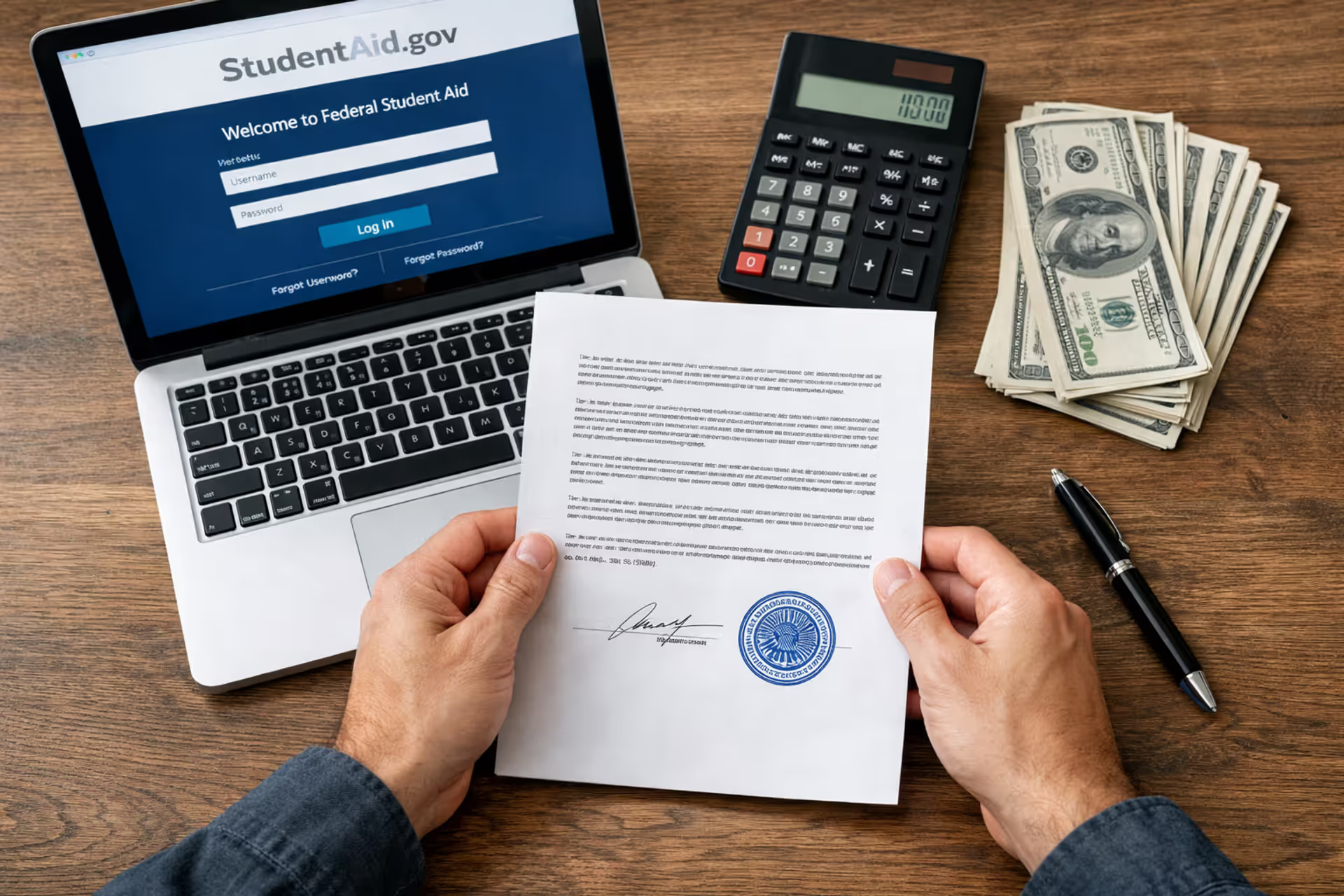

Head to StudentAid.gov and log in with your FSA ID (the username and password you created when filing your FAFSA). Navigate to the loan repayment section and select "Apply for an Income-Driven Repayment Plan." The application pulls your loan data automatically from federal databases, so you'll see your current balances and loan types pre-populated.

You'll answer questions about family size—that's you, your spouse if married, and any children or dependents you support. Next comes income. The system offers IRS Data Retrieval, where you authorize direct access to your tax return. This is fastest—approval in 4-6 weeks typically. You can instead upload your tax return PDF, but that triggers manual review and adds processing time.

Current income significantly below your tax return? Maybe you lost your job six months ago, or you're on parental leave. You can submit alternative documentation—recent pay stubs, a termination letter, proof of unemployment benefits. This slows processing but prevents you from being stuck with payments calculated on income you're not earning anymore.

Choose your preferred plan from the list of options your loans qualify for. Not sure which one? The Loan Simulator tool (separate section on StudentAid.gov) runs projections showing estimated payments and forgiveness timelines under each plan based on your actual loan portfolio.

Submit the application. Your servicer gets notified, reviews your documentation, calculates your payment, and mails (or emails) a confirmation showing your new payment amount and first due date. Processing averages 4-6 weeks but can stretch to 8-10 weeks during high-volume periods—like when policy changes flood the system with applications.

While processing, you're still responsible for current payments unless you're in grace, deferment, or forbearance. If you can't afford current payments while waiting, contact your servicer about temporary forbearance. Interest still accrues, but you won't be marked late.

Once approved, mark your calendar for one year from now. That's your recertification deadline—non-negotiable. Your servicer will mail reminders starting 60 days out. Missing that deadline reverts your payment to the standard 10-year amount and capitalizes unpaid interest.

Switching plans later? Just submit a new application selecting the different plan. Payments already made count toward forgiveness under your new plan's rules.

Pros and Cons of Enrolling in an IDR Plan

The upside: payments you can actually afford without choosing between your loans and your rent. A $735 standard payment becomes $90 under SAVE for someone earning $45,000 with undergraduate debt. That's $645 monthly breathing room.

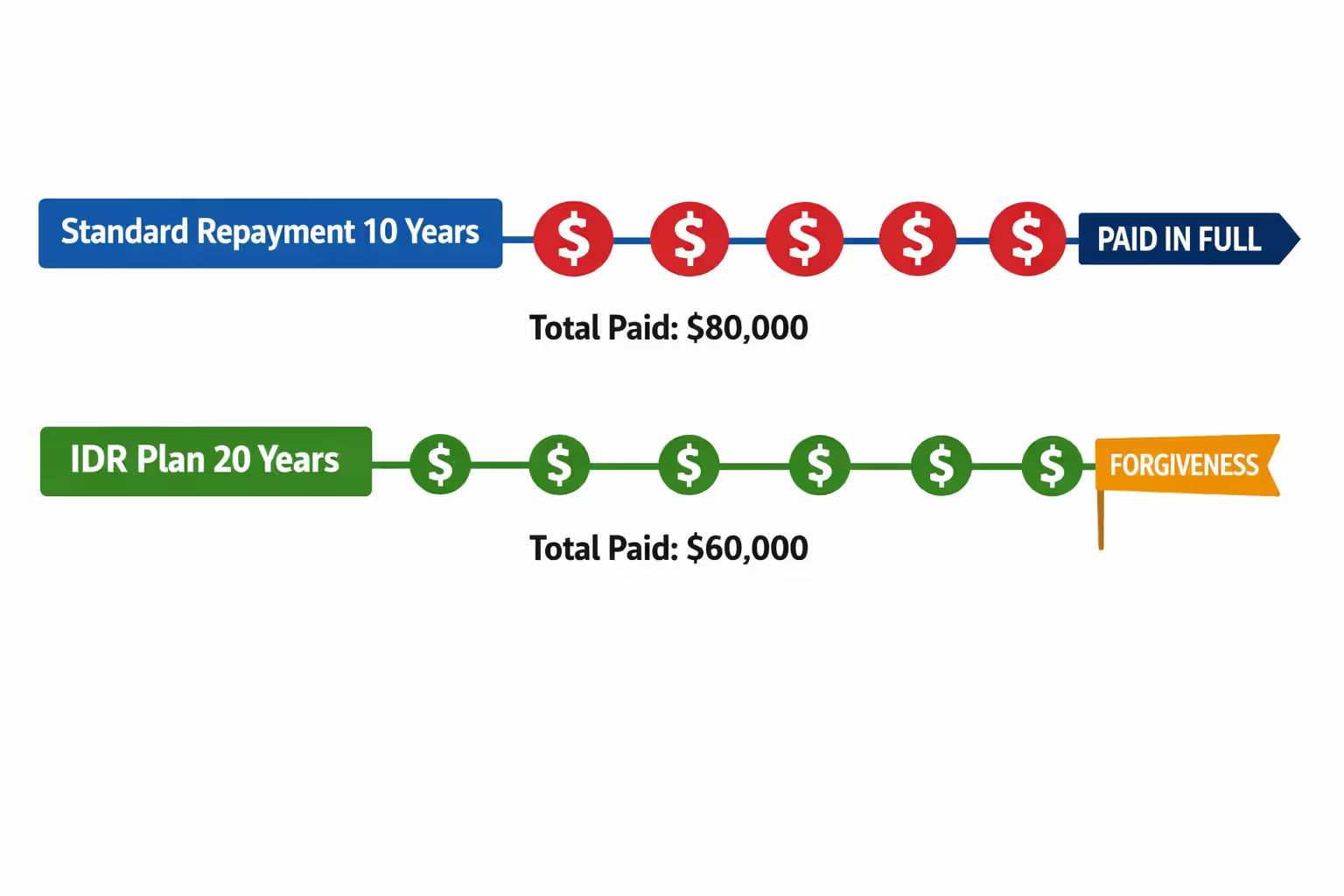

Forgiveness becomes realistic for borrowers who'd never pay off their balances otherwise. You borrowed $120,000 for a social work degree. You're earning $47,000. Standard repayment costs $1,383 monthly—literally more than your take-home pay. Under SAVE, you'd pay roughly $150 monthly for 20 years, totaling $36,000 in payments, with the remaining $84,000 (plus accumulated interest) forgiven. Without IDR, your only options are forbearance, default, or a career change.

Student loan debt is the only form of consumer debt that has continued to rise through the Great Recession. It's crushing the ability of young people to buy homes, start businesses, and save for retirement

— Mark Cuban

Default protection keeps your credit score intact and prevents wage garnishment or tax refund seizure. Fall behind on payments and your servicer can eventually take 15% of your paycheck directly. Stay in IDR—even at $0 payments during low-income periods—and your loans stay current.

Now the downsides. Extended timelines mean interest compounds for two decades instead of one. Let's say you start SAVE at age 25 earning $38,000. You're paying minimally for years while interest accrues. You get promoted at 35 and start earning $75,000. Your payment increases to $350 monthly—still affordable, but now you're paying mostly toward that accumulated interest instead of making progress on principal. You might pay $90,000 total over 20 years on a $60,000 original balance and still have $30,000 forgiven. Compare that to standard repayment: $72,000 total with no forgiveness needed.

That math flips if your income never rises substantially. It also flips if you value cash flow now over total interest paid later. For most people in helping professions, education, nonprofits, or anything paying $40,000-$60,000 long-term, IDR saves money. For people expecting income growth into six figures, it might not.

Interest capitalization happens when you leave IDR or miss recertification. That unpaid interest—say $15,000 accumulated over years—gets added to your principal. Now you owe $75,000 instead of $60,000, and future interest calculates on that higher amount. SAVE prevents this during enrollment through its interest subsidy, but IBR, PAYE, and ICR don't. Borrowers in older plans sometimes see balances grow despite making every payment.

Author: Olivia Harrington;

Source: sonicmusic.net

Forgiveness tax treatment remains uncertain. Federal law exempted forgiven student debt from income taxes through 2025 under the American Rescue Plan. Congress keeps debating whether to extend this, eliminate it, or make the exemption permanent. As of mid-2026, no final decision exists. You might reach forgiveness in 2038 and face a $30,000 tax bill on your forgiven balance, or Congress might have permanently eliminated the tax by then. Plan for the possibility, but don't assume either outcome.

Administrative burden: you're signing up for 20 years of annual paperwork. Recertify every year, update your address when you move, respond to servicer requests, track your payment count. Some people handle this easily. Others forget deadlines and face payment spikes that wreck their budget.

IDR Plan Comparison Table

| Feature | SAVE | IBR (Newer Borrowers) | IBR (Earlier Borrowers) | PAYE | ICR |

| Payment Percentage | Undergrad: 5% Graduate: 10% | 10% of discretionary income | 15% of discretionary income | 10% of discretionary income | 20% of discretionary income OR 12-year adjusted amount |

| Income Protection Level | Anything below 225% of poverty line | Anything below 150% of poverty line | Anything below 150% of poverty line | Anything below 150% of poverty line | Anything below 100% of poverty line |

| Years Until Forgiveness | 20 years (undergrad debt only) 25 years (any graduate debt) | 20 years of payments | 25 years of payments | 20 years of payments | 25 years of payments |

| Loan Types That Work | Direct Loans (excludes Parent PLUS) | Direct and FFEL Loans (excludes Parent PLUS) | Direct and FFEL Loans (excludes Parent PLUS) | Direct Loans only (excludes Parent PLUS) | Direct Loans and consolidated Parent PLUS |

| Spouse's Income Counted? (if filing separately) | No | No | No | No | Yes, always counted |

| Maximum Monthly Payment | No limit—scales with income | Capped at standard 10-year amount | Capped at standard 10-year amount | Capped at standard 10-year amount | No cap |

| Interest Protection | Government covers gap if payment doesn't cover monthly interest | Covers interest on subsidized loans for 36 months | Covers interest on subsidized loans for 36 months | Covers interest on subsidized loans for 36 months | No coverage |

| Ideal For | Most Direct Loan borrowers seeking lowest payments | FFEL loan holders or borrowers who don't qualify for SAVE | Borrowers who took first loan before July 2014 | Borrowers in 2007-2011 window | Parents who consolidated PLUS loans |

Common Mistakes Borrowers Make with IDR Plans

The annual recertification deadline catches more borrowers than anything else. Your servicer sends email reminders 60 days out, 30 days out, and at the deadline. But you moved apartments and forgot to update your address. Or the email went to spam. Or you saw it and thought "I'll do that this weekend" for six consecutive weekends. Your deadline passes. The next month, your $73 payment becomes $486. The unpaid interest that was sitting separately—maybe $8,000—capitalizes onto your principal. You now owe $68,000 instead of $60,000, permanently.

Set a recurring annual reminder in your phone calendar independent of servicer notices. Treat it like your car registration renewal—something you do proactively, not reactively.

Income changes mid-year throw people off. You recertified in March 2025 based on your 2024 tax return showing $42,000 income. You got promoted in June 2025 to $58,000. Your payment stays based on $42,000 until March 2026, then suddenly jumps to reflect the $58,000. Some borrowers get blindsided by this increase. You can request early recalculation anytime using recent pay stubs, which recalculates immediately but also resets your annual deadline to that new month.

Author: Olivia Harrington;

Source: sonicmusic.net

Choosing the wrong plan costs real money. Borrower with $50,000 in undergraduate Direct Loans enrolls in IBR (10%) instead of SAVE (5%) because they didn't understand the difference. Same income, same family size, double the payment. That's $80 monthly they didn't need to spend, or $960 annually.

Parents often don't realize Parent PLUS loans require consolidation first. They apply for SAVE, get denied, give up. They needed to consolidate into a Direct Consolidation Loan first, then apply for ICR. Servicers should explain this, but many don't volunteer information—you have to know to ask.

Filing taxes wrong tanks your payment calculation. Married couple files jointly because their tax software defaults to that. Both spouses earn $50,000—combined $100,000 AGI. Their IDR payment calculates on $100,000. Next year they file separately after learning about the strategy. Now the borrower's payment calculates only on their $50,000, potentially cutting their payment in half. But filing separately cost them $2,300 in additional taxes. They saved $1,800 in loan payments, so they're net negative $500. They should have run both scenarios before choosing.

Tax software doesn't understand IDR implications. H&R Block, TurboTax, your CPA—none of them automatically flag "hey, filing separately might lower your student loan payment." You need to explicitly run calculations both ways.

Consolidating loans to access better plans without understanding you're resetting forgiveness timelines. Borrower made six years of IBR payments, consolidates to access SAVE. They now have zero years of forgiveness credit—they're starting fresh on the 20-year clock. Whether that trade-off makes sense depends on the payment savings and how many years you're resetting. Three years of credit lost to cut your payment by $150 monthly? Probably worth it. Twelve years lost for $30 monthly savings? Questionable.

Frequently Asked Questions About IDR Student Loans

Income-driven repayment transforms your federal student loans from a fixed monthly crisis into something that flexes with your actual financial reality. The right plan depends on when you borrowed, which loan types you're carrying, what you earn now, and whether you're married. For most people holding Direct Loans in 2026, SAVE offers the lowest payments and strongest interest protections. Borrowers still carrying FFEL loans might benefit from consolidating to access it. Parents face more constraints but can still reach manageable payments through ICR after consolidating their Parent PLUS loans.

You're signing up for ongoing administrative work—annual recertification isn't optional, and missing that deadline costs you hundreds of dollars immediately and potentially thousands in capitalized interest. Borrowers who stay organized, track deadlines proactively, and communicate with servicers when situations change navigate these programs successfully. Those who enroll once and forget about it usually face problems.

Calculate your potential payments before enrolling. The federal Loan Simulator at StudentAid.gov uses your actual loan data and projects payments under different plans at various income levels. Compare what you'd pay if your income stays flat, increases 3% annually, or jumps significantly. Look at total payments over the full timeline, not just the monthly amount.

These plans work best for borrowers whose debt-to-income ratio makes standard repayment mathematically impossible, people in careers that pay modestly relative to their debt, or anyone facing income uncertainty. Someone earning $85,000 with $35,000 in loans might actually pay less total interest under standard repayment, though IDR still provides valuable insurance if their income drops unexpectedly.

Watch for legislative changes. IDR rules evolved significantly over the past three years—REPAYE became SAVE, forgiveness tax treatment changed temporarily, payment formulas got adjusted. Staying informed helps you optimize your approach as policies shift.

Your student loan repayment timeline rarely goes according to plan. Careers change, incomes fluctuate, life interrupts the trajectory you imagined at graduation. Income-driven plans acknowledge that reality and provide structure that adjusts rather than breaks when circumstances change. Understanding how these programs actually operate, which one fits your current situation, and what commitments you're making puts you in control of debt that otherwise controls you.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.