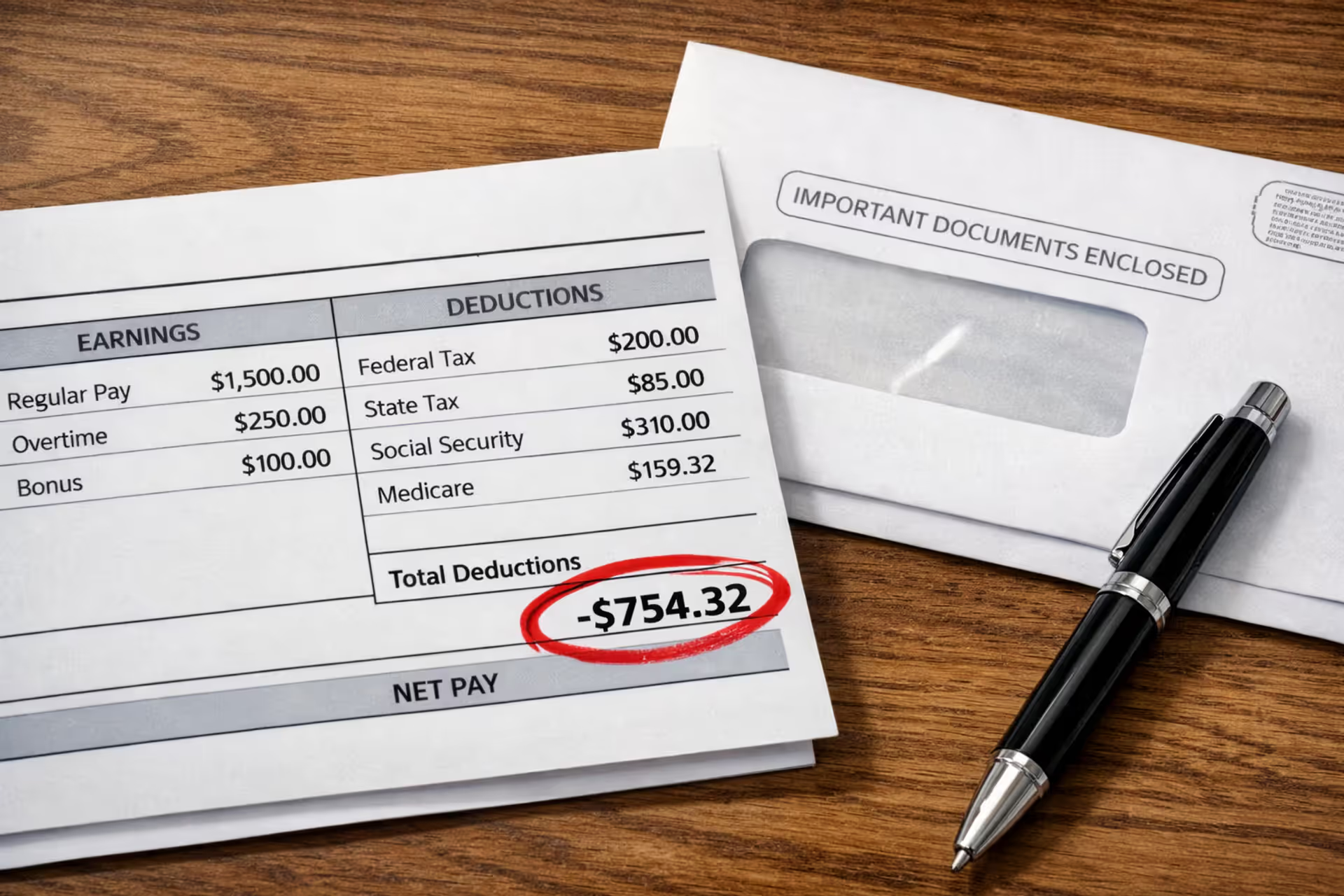

Close-up of a paycheck stub with a highlighted deduction line next to an official government letter on a wooden desk

How Wage Garnishment Works for Student Loans?

Federal student loan default triggers consequences that extend far beyond late payment notices. Among the most financially disruptive is administrative wage garnishment—a collection mechanism that allows the Department of Education to claim a portion of your earnings without filing a lawsuit or obtaining a judge's approval. Grasping how this system operates and which defensive strategies actually work can determine whether you navigate toward financial recovery or sink deeper into economic distress.

What Is Student Loan Wage Garnishment?

Student loan wage garnishment represents a collection authority that permits the federal government to recover defaulted education debt by taking money directly from your paychecks. After your federal student loan enters default status (generally following 270 consecutive days without payment), the Department of Education or its contracted guaranty agency can direct your employer to redirect up to 15% of your disposable earnings straight to the loan holder.

The term "administrative wage garnishment" distinguishes this from conventional court-ordered wage attachments because it operates entirely outside judicial oversight. Federal statutes grant the Department of Education collection capabilities that regular creditors cannot access. Credit card issuers must file suit and secure a judgment before touching your wages. Student loan agencies skip that step entirely.

Private student loans follow traditional legal channels. Private lenders must pursue lawsuits and win judgments before initiating paycheck deductions, giving borrowers additional time to mount a defense or reach settlements. Yet once a private lender secures that court order, they can typically claim up to 25% of disposable earnings—substantially more than federal programs take.

The 15% limitation applies to disposable earnings, not your full paycheck. Disposable earnings represent what's left after subtracting mandatory tax withholdings and payroll deductions required by law: federal income tax, state income tax, Social Security contributions, Medicare payments, and state unemployment insurance premiums. Elective deductions—health insurance, 401(k) contributions, union dues, or charitable giving—don't shield income from garnishment calculations.

Default thresholds vary slightly across loan categories, but federal loans generally enter default after 270 days of consecutive nonpayment. Crossing that threshold makes your entire outstanding balance immediately due, opening the door to aggressive collection tactics including paycheck seizures.

The Student Loan Wage Garnishment Process

The journey from default to automatic paycheck deductions follows a regulated sequence prescribed by federal law. Recognizing each phase creates opportunities to interrupt the process.

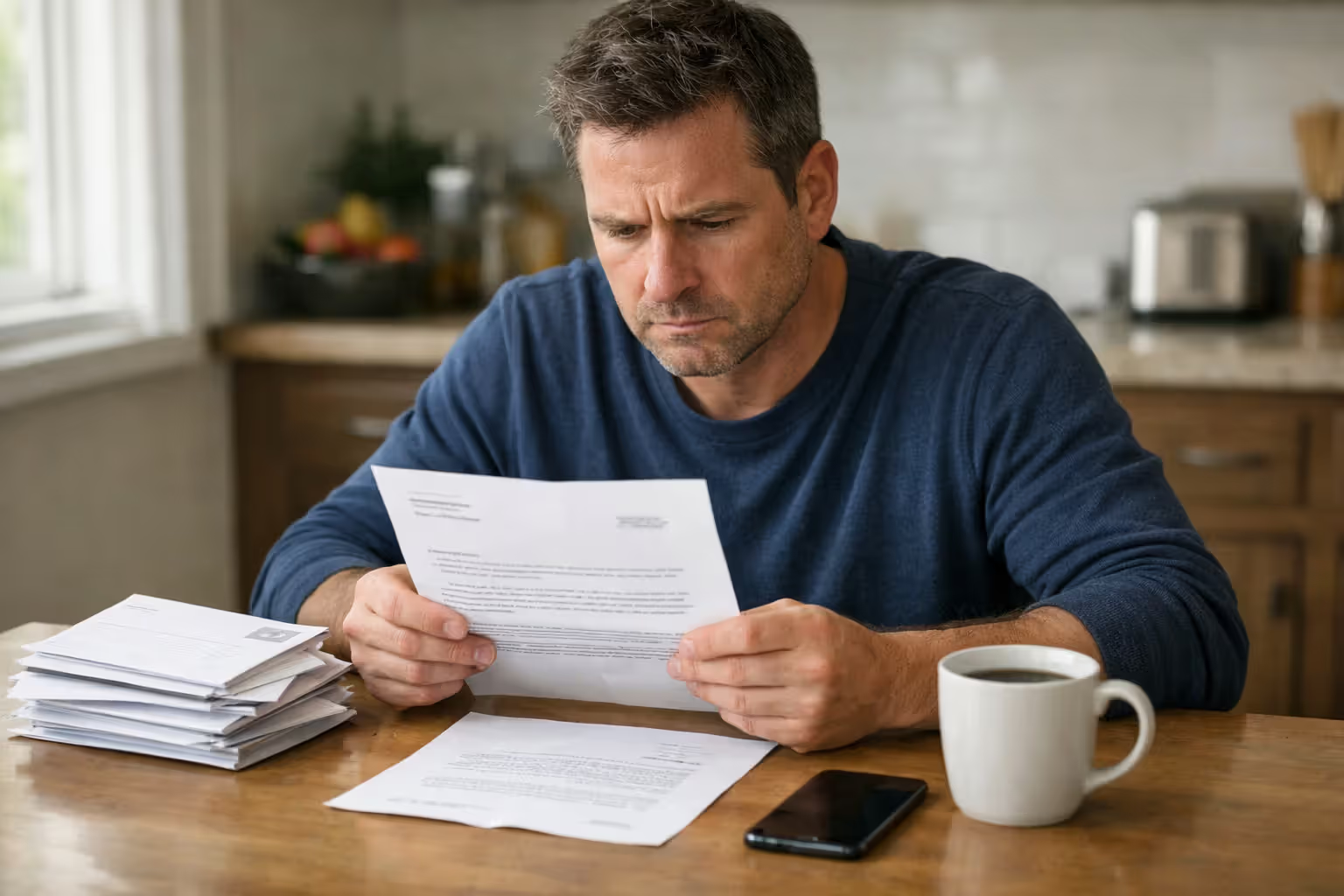

Following your loan's default designation, the Department of Education or its guaranty agency must mail you written notification at least 30 days before initiating paycheck deductions. This letter details your outstanding debt, explains your right to examine loan documentation, outlines hearing request procedures, and describes available repayment alternatives.

Author: Olivia Harrington;

Source: sonicmusic.net

Countless borrowers never see this critical notice—or they receive it at an outdated address and remain uninformed until their employer alerts them. If you've relocated without notifying your loan servicer, the law still treats you as properly notified when correspondence reaches your last registered address.

Within that 30-day notification period, you may demand a hearing. These proceedings occur via telephone or written correspondence; in-person appearances aren't required. During your hearing, you can introduce evidence documenting financial hardship, challenge whether the debt legitimately belongs to you, or demonstrate that garnishment would make basic living expenses unaffordable.

Without a hearing request or following an unfavorable hearing outcome, the agency transmits a garnishment directive to your employer. Employers possess no discretionary authority to ignore these orders—federal law mandates compliance. Your employer must begin withholding funds during the initial pay cycle occurring at least 30 days after receiving the directive.

Employers notify affected workers upon receiving garnishment orders, but by that stage the withholding machinery is already engaged. The garnishment persists until you've satisfied the full debt, negotiated alternative arrangements, or successfully contested the garnishment's validity.

Guaranty agencies and the Department of Education orchestrate this process, frequently enlisting third-party collection firms. These contracted collectors earn commissions on recovered amounts, creating financial incentives to avoid mentioning rehabilitation programs or other options that would terminate garnishment.

How Much Can Be Garnished From Your Paycheck?

Federal student loan garnishments cap at 15% of your net disposable earnings. While generally less severe than other garnishment types, this still creates meaningful monthly reductions in household income.

Determining disposable earnings requires identifying which deductions count as legally mandated. Begin with your gross wages, then remove:

- Withheld federal income taxes

- Withheld state and local income taxes

- Social Security contributions (FICA)

- Medicare withholdings

- State unemployment insurance deductions

What remains constitutes your disposable earnings. Multiply that figure by 0.15 to calculate the maximum garnishment per pay period.

Consider this scenario: You earn $3,000 gross biweekly, with $600 withheld for mandatory taxes and payroll obligations. Your disposable earnings equal $2,400. The garnishment would claim $360 from each paycheck, totaling $720 monthly.

State-level protections occasionally exceed federal standards, though these rarely apply to student loan garnishments. Most state wage attachment limits govern judgment creditors pursuing traditional court orders, not federal administrative garnishments.

The 15% maximum applies to each individual employer. Working multiple jobs theoretically exposes you to 15% garnishment from each paycheck, though practically the Department of Education usually targets only your primary income source.

Wage Garnishment Limits by Debt Type

| Debt Category | Maximum Withholding | Lawsuit Required? | Additional Details |

| Federal Student Loans | 15% of net disposable pay | No | Administrative authority; court proceedings unnecessary |

| Credit Cards / Unsecured Loans | 25% of net disposable pay | Yes | Requires judgment; state variations apply |

| Child Support Obligations | 50-65% of net disposable pay | Yes | 50% with dependent support; 60-65% without |

| IRS Tax Debts | Variable by exemption table | No | Calculated using filing status and dependents; may exceed 25% |

Child support withholdings receive priority over student loan garnishments. Existing child support deductions reduce your disposable income before calculating student loan garnishment amounts.

Your Rights During Wage Garnishment

Federal regulations establish borrower protections, but these safeguards activate only when you assert them. The system awards no automatic relief.

You possess the right to demand a hearing within 30 days following garnishment notification. Hearings evaluate four core issues:

- Whether the claimed debt legitimately exists and the stated amount is accurate

- Whether you're currently fulfilling an established payment agreement

- Whether you've already satisfied the debt

- Whether garnishment would inflict severe financial hardship

Financial hardship claims represent the most frequently invoked defense, though the evidentiary threshold is substantial. You must prove garnishment would make meeting fundamental living costs impossible—housing, utilities, food, and necessary medical care. Demonstrating mere inconvenience or budgetary tightness won't suffice.

Head of household protections exist in select states, permitting primary earners supporting dependents to claim garnishment immunity. This represents state-level legislation that doesn't automatically override federal student loan garnishments, but investigating these protections makes sense if you financially support children or other dependents.

When garnishment appears erroneous—perhaps the debt isn't yours, or default never actually occurred—you can challenge it through documented evidence. Common scenarios include identity theft, loan discharge following school closure or fraud, or administrative mistakes incorrectly showing default status.

Borrowers' biggest misstep is treating garnishment notices like junk mail. That 30-day response window represents your strongest leverage point for preventing garnishment before it starts. Once withholding begins, reversing it becomes exponentially harder, and you've already lost income that's gone forever

— Jennifer Martinez

Requesting hearings doesn't automatically pause garnishment, but frequently delays implementation while your case undergoes review. Exploit this interval to compile financial documentation and investigate rehabilitation possibilities.

How to Stop Wage Garnishment for Student Loans

Active garnishment isn't a permanent condition. Multiple strategies can halt withholding and rebuild financial stability, though each carries distinct advantages and limitations.

Loan Rehabilitation Explained

Rehabilitation offers the most powerful method for terminating garnishment while simultaneously erasing default from your credit history. The program demands nine qualifying payments made voluntarily and on schedule across ten consecutive months. Payment amounts typically equal 15% of your discretionary income, calculated through formulas resembling those used for income-driven repayment programs.

Author: Olivia Harrington;

Source: sonicmusic.net

Significantly, rehabilitation payments can drop to just $5 monthly when income falls sufficiently low. The Department of Education must calculate a "reasonable and affordable" payment reflecting your actual financial circumstances. You'll submit income verification—recent pay stubs, filed tax returns, or public assistance documentation.

After completing your ninth qualifying payment, garnishment ceases, default notations disappear from credit reports, and your loan transfers back to standard servicing. You'll then select either a conventional repayment schedule or an income-driven plan moving forward.

Rehabilitation works only once per loan. Defaulting again after successful rehabilitation permits garnishment to resume without another rehabilitation opportunity.

Rehabilitation doesn't forgive debt or shrink your balance. Collection costs reaching 16% of outstanding principal and interest may attach to your loan balance even after completing rehabilitation.

Federal Loan Consolidation

Creating a new Direct Consolidation Loan that absorbs your defaulted loans immediately terminates wage garnishment. Consolidation remains available during default, but requires either three consecutive voluntary payments on defaulted loans first, or commitment to repaying your new consolidation loan through an income-driven plan.

Consolidation won't erase default from credit reports—rehabilitation alone accomplishes that. However, consolidation restores access to deferment, forbearance, and income-driven repayment options that default status blocks.

The tradeoff involves interest capitalization, which incorporates unpaid interest into principal and increases your total repayment obligation. Borrowers nearing forgiveness under existing repayment schedules may reset their progress through consolidation.

Strategic borrowers sometimes consolidate for immediate garnishment relief, then pursue consistent payments to gradually rebuild credit. This approach works best when you need urgent relief and accept that default notations will persist on credit reports for seven years.

Direct payment agreements negotiated with the Department of Education can halt garnishment, though these arrangements lack the formal structure of rehabilitation or consolidation. You'll need documented financial hardship and a sustainable payment proposal. Success varies case-by-case without guarantees.

Settlement negotiations rarely succeed with federal student loans. The Department of Education possesses extensive collection authority and limited incentive to accept reduced payoff amounts. Private student loans prove more amenable to settlements, particularly when debts have aged or lenders doubt your repayment capacity.

Bankruptcy seldom discharges student loan obligations. You must establish "undue hardship" through adversary proceedings, demonstrating that repayment would prevent maintaining minimal living standards, that this hardship will endure throughout most of the repayment term, and that you've made genuine repayment attempts. Few borrowers satisfy these stringent criteria, though recent Department of Justice guidance has marginally improved discharge accessibility.

Preventing Wage Garnishment Before It Starts

Optimal strategy involves avoiding default altogether. Once you've accumulated 270 days of delinquency, available options narrow dramatically.

Income-driven repayment plans recalculate monthly obligations based on household size and earnings. Four programs remain available as of 2026: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR). Monthly payments can reach $0 when income falls below 150% of federal poverty guidelines.

Author: Olivia Harrington;

Source: sonicmusic.net

Enrolling in income-driven plans before default prevents garnishment while maintaining good standing. Even with existing delinquency, catching up and enrolling can stop the default countdown.

Deferment and forbearance create temporary payment pauses. Deferment applies during unemployment, economic hardship, school enrollment, or active military service. Subsidized loans may avoid interest accrual during deferment. Forbearance offers greater flexibility but less favorable terms—interest accumulates on all loan types, expanding balances.

Neither deferment nor forbearance harms credit standing, and both prevent default. Deploy them strategically during legitimate financial emergencies, but avoid long-term reliance. Interest capitalization can dramatically inflate debt over extended periods.

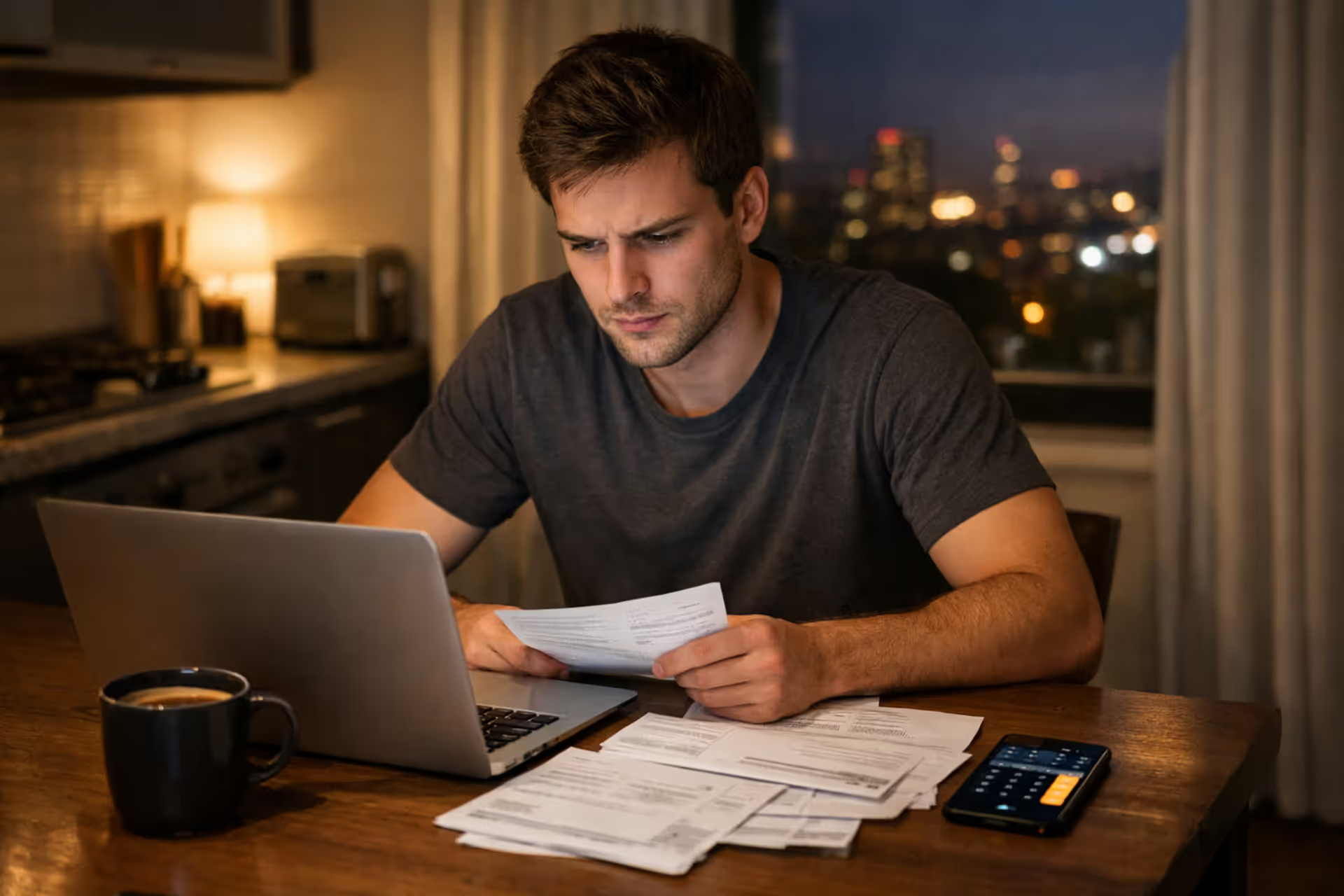

Maintaining servicer contact deserves more attention than it receives. When payment difficulties emerge, contact your servicer before missing payments. Servicers can arrange short-term accommodations, adjust payment due dates, or facilitate income-driven repayment applications. Ignoring problems guarantees worse outcomes.

Default prevention also requires updating contact information with each address change, monitoring loan status through Federal Student Aid portals, and enabling automatic payments to eliminate missed deadline risks.

Common Mistakes That Make Garnishment Worse

Borrowers confronting garnishment repeatedly commit predictable errors that amplify their difficulties.

Discarding garnishment notices inflicts maximum damage. The 30-day hearing request window represents your most potent defensive tool. Once that window closes, you've surrendered your right to challenge garnishment before it begins. Even doubtful cases benefit from hearing requests—they create delay and force agencies to justify their actions.

Author: Olivia Harrington;

Source: sonicmusic.net

Skipping hearing requests also means forfeiting opportunities to present financial hardship documentation. Many borrowers assume they won't qualify for relief, but hearing processes prove more accessible than commonly believed. Attorneys aren't required, and agencies bear the burden of proving garnishment appropriateness.

Overlooking rehabilitation represents another expensive mistake. Some borrowers believe garnishment becomes permanent once initiated. Rehabilitation provides a documented exit path, yet many borrowers never learn about it because collection agencies avoid promoting options that terminate their commission stream.

Quitting jobs to escape garnishment generates more complications than solutions. Garnishment follows you between employers—the Department of Education simply issues fresh garnishment orders after identifying your new workplace. Meanwhile, you've sacrificed income and potentially damaged your employment record.

Some borrowers mistakenly believe garnishment satisfies their entire payment obligation. Garnishment represents just one collection mechanism among several. Interest continues accumulating, and the government can simultaneously seize tax refunds, Social Security benefits (up to 15%), and other federal payments.

Another fallacy suggests garnishment permanently destroys credit. While default severely damages credit scores, rehabilitation completely removes default notations. Credit recovery remains achievable, but only through deliberate action.

Finally, some borrowers attempt negotiating reduced withholding directly with employers. Employers lack authority to modify garnishment amounts. Orders originate from the Department of Education, and only the Department can adjust or cancel them.

FAQ About Student Loan Wage Garnishment

Wage garnishment for student loans feels punishing, but it doesn't constitute a permanent financial sentence. The federal framework provides multiple escape routes—rehabilitation, consolidation, and income-calibrated repayment plans—that can restore financial equilibrium and even repair credit damage.

Critical success depends on rapid response when receiving initial garnishment notices. The 30-day pre-garnishment window represents your highest-value opportunity. Demand your hearing, investigate rehabilitation eligibility, and document your financial circumstances thoroughly. Even after garnishment begins, rehabilitation can terminate it within months while erasing default from credit histories.

Shame and anxiety shouldn't prevent addressing these problems. Millions of borrowers have experienced default and garnishment, and most who respond deliberately eventually recover. The Department of Education benefits from returning you to sustainable repayment—they ultimately collect more revenue from borrowers making steady payments than from those trapped in default status.

If you're currently experiencing garnishment, contact your loan servicer or the Department of Education's Default Resolution Group immediately. Specifically request rehabilitation information, and refuse vague promises that "arrangements can be made." Obtain concrete terms in writing, confirm exact payment amounts, and initiate those nine qualifying payments without delay.

Prevention remains superior to remediation. If you're struggling with student loan payments but haven't yet defaulted, enroll in an income-driven repayment plan immediately. Following job loss or income reduction, apply for deferment or forbearance. These programs exist specifically to prevent default and subsequent garnishment.

Wage garnishment creates serious consequences, but solutions exist. Understanding your legal protections, responding within mandated timeframes, and selecting the rehabilitation or consolidation pathway matching your circumstances can terminate garnishment and establish a route toward eventual payoff or loan forgiveness.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.