Top-down view of a student desk with a laptop showing an interest growth chart, dollar bills, a calculator, a graduation cap, and financial documents

When Does Interest Start on Student Loans?

Content

Content

Here's something that catches most college students completely off-guard: your loans might be generating charges before you've even unpacked your dorm room. The timing changes dramatically depending on which loan you signed up for—certain federal options don't touch your balance throughout your entire undergraduate career, while others add daily charges from the moment your financial aid office processes the paperwork. Get this wrong, and you'll finish school owing significantly more than you originally borrowed, despite never missing a single payment deadline.

How Student Loan Interest Works

Student loan interest functions like a rental fee—you're paying lenders for the privilege of using their money today instead of saving up over years. Here's what catches people: lenders tally up these charges every 24 hours, not monthly.

The math behind it is pretty straightforward, though the results surprise people. Lenders take your annual percentage rate, split it across 365 days, then multiply that fraction by whatever you currently owe. Let's walk through real numbers. You've borrowed $10,000 at a 5% annual rate. Each day adds about $1.37 to what you owe ($10,000 × 0.05 ÷ 365). Seems pretty manageable, right? But stack those daily charges across four years of undergraduate courses—you're carrying an extra $2,000 on just that single loan.

Here's where the real damage happens. All those daily charges don't just sit there waiting patiently. Eventually, your lender performs what's called capitalization—they scoop up every accumulated charge and blend it into your original borrowed amount. Now you're being charged interest on top of previous interest charges. It creates a compounding effect, similar to a snowball picking up more snow as it rolls downhill. This explains why someone's $30,000 starting balance can somehow become $40,000 without them grasping what went wrong.

Author: Evan Thornton;

Source: sonicmusic.net

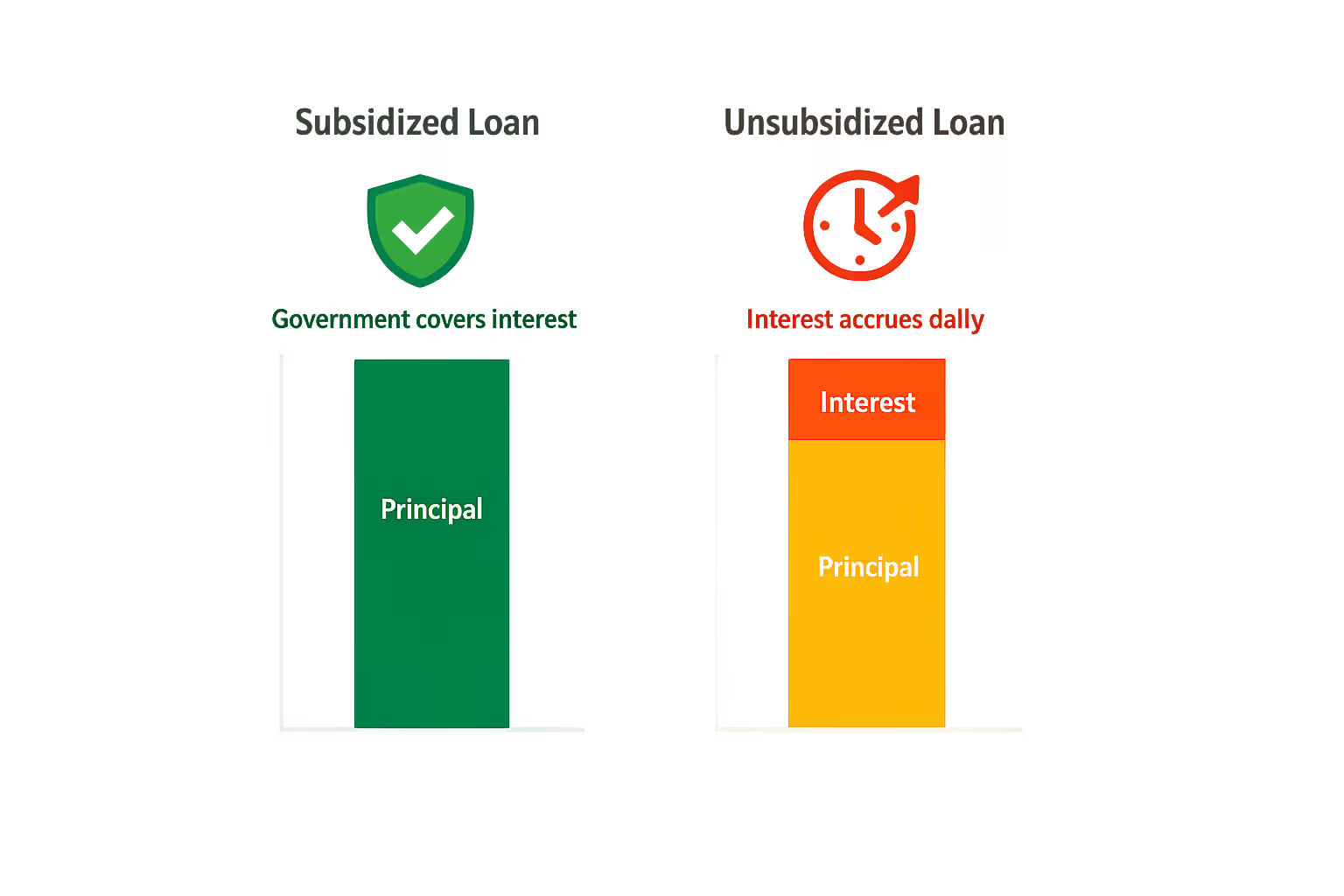

The question that actually matters isn't just about percentage rates—it's figuring out exactly when those daily calculations begin. Got federal subsidized loans? You're protected throughout your enrollment. Borrowed anything else? Those charges begin accumulating right away.

When Federal Student Loan Interest Begins

Federal student loans operate under Department of Education guidelines, but assuming they all function identically is a costly mistake. The differences are substantial.

Direct Subsidized Loans

This loan type offers you something genuinely rare in lending—government-funded protection during these specific timeframes:

- While you're taking at least six credit hours: Your balance won't budge

- Six months following your graduation or withdrawal: Still protected

- Any officially approved deferment period: Government continues paying on your behalf

Interest charges only begin once your monthly billing cycle starts. Finish your degree in May? You won't see any interest added until December rolls around, after that six-month window closes. The federal government essentially picks up your interest tab during school and immediately afterward—genuinely free borrowing during these phases.

There's a catch, naturally. Only undergraduate students demonstrating financial need through their FAFSA qualify. The annual limits run from $3,500 for first-year students up to $5,500 once you hit junior and senior years, so covering your full college costs this way isn't realistic for most people.

Direct Unsubsidized Loans

This category reverses everything. Interest begins accumulating the exact day your college receives the funds—typically a few days before your semester officially kicks off. Starting fall classes in late August? Your August disbursement already has charges piling up before you attend your first lecture or crack open a textbook.

Here's the calculation most borrowers overlook. Imagine a freshman borrows $5,500 through unsubsidized loans carrying a 5.5% rate. Don't make any payments throughout four undergraduate years? You'll accumulate roughly $1,200 in pure interest before your repayment phase even begins. That $1,200 gets capitalized, pushing your actual starting repayment balance to $6,700. You're now being charged interest on $1,200 you never actually received or spent.

There's no income requirement blocking access to unsubsidized loans—undergraduates, graduate students, doesn't matter whether your family earns $30,000 or $300,000 annually. Graduate students currently face steeper rates, hovering around 7.05% for loans disbursed during the 2025-2026 academic year.

PLUS Loans

PLUS loans—which graduate students and parents of dependent undergraduates can access—begin generating interest charges at disbursement, matching unsubsidized loan behavior. What differs is the repayment schedule:

- Parent PLUS Loans: Your first payment comes due within 60 days of receiving funds, although parents can request in-school deferment to postpone this

- Grad PLUS Loans: Graduate students receive a six-month grace window after finishing their program or dropping below half-time enrollment

Currently sitting at approximately 8.05% interest for the 2025-2026 period, plus a 4.228% origination fee deducted upfront, PLUS loans represent the most expensive federal borrowing option. Interest compounds throughout your entire degree unless you're actively submitting payments. Once any deferment period wraps up, all those accumulated charges get capitalized into a substantially larger principal balance.

Student Loan Interest Start Times by Loan Type

| Loan Type | Interest Begins | Who Handles Charges During Enrollment | What Happens During Grace Period |

| Direct Subsidized | When repayment phase starts | Federal government pays | Federal government continues paying |

| Direct Unsubsidized | When funds hit your school | Borrower responsible (or it compounds) | Borrower responsible (or it compounds) |

| Direct PLUS (Parent) | When funds hit your school | Borrower responsible (or it compounds) | Borrower responsible (or it compounds) |

| Direct PLUS (Grad) | When funds hit your school | Borrower responsible (or it compounds) | Borrower responsible (or it compounds) |

| Private Loans | Varies by lender (usually at disbursement) | Usually borrower's responsibility | Usually borrower's responsibility |

When Private Student Loan Interest Starts Accruing

Private lenders operate outside federal oversight, giving each financial institution freedom to write its own playbook. That said, the overwhelming majority of private student loans start generating interest charges immediately when they transfer funds to your educational institution.

Most lenders present you with three approaches for managing payments during your enrollment:

Immediate full repayment: You tackle both principal and interest starting day one. This costs you the least over the loan's lifetime, but it's tough when you're balancing coursework, extracurriculars, and maybe a weekend shift at the campus bookstore.

Interest-only payments: You cover just the daily accumulating interest each month, which prevents capitalization without draining your bank account. Someone carrying $20,000 in private loans at 7% would face roughly $117 monthly—doable for students with consistent part-time income.

Complete deferral: You skip every payment while completing your degree. Maximum convenience, absolutely, but interest continues compounding nonstop. This approach tacks thousands onto your final bill.

A handful of lenders offer a hybrid fourth option: modest fixed payments around $25 monthly. These don't fully cover your accumulating interest but they slow down the damage considerably.

Federal loans carry standardized rates that Congress sets annually for everyone. Private loan rates work completely differently—they depend on your credit history and financial profile. Rates range from roughly 4% for borrowers with pristine credit histories up to 14% or beyond for applicants lenders consider risky. Variable rates can climb over your repayment period, making your ultimate cost difficult to predict accurately.

Most private lenders include a six-month grace window after you leave school, but interest charges continue accumulating unless you're actively submitting payments. Read through your promissory note carefully—some lenders capitalize quarterly during your enrollment rather than waiting until your repayment phase starts.

Author: Evan Thornton;

Source: sonicmusic.net

Interest During Grace Periods and Deferment

That six-month grace period following graduation confuses nearly everyone. For subsidized federal loans, the government keeps covering your interest charges throughout those months. For literally every other loan category, interest continues piling up during the entire six-month span.

Here's a concrete scenario: You graduate carrying $30,000 in unsubsidized loans at 6%. Throughout your grace period, approximately $900 in interest builds up. Choose not to pay it? That $900 gets capitalized when your first official payment arrives, bumping your principal to $30,900. Your monthly payment just jumped by roughly $10 for the next ten years.

Deferment allows you to temporarily suspend payments—maybe you're facing unemployment, dealing with economic hardship, or you've returned to school for an advanced degree. But do interest charges pause alongside your payments? It depends completely on which loan type you're carrying:

- Subsidized loans: The government continues covering those charges

- Unsubsidized loans, PLUS loans, and private loans: Interest keeps calculating daily

Author: Evan Thornton;

Source: sonicmusic.net

Forbearance similarly pauses your payment requirement but offers zero interest protection on any loan type whatsoever. Take a 12-month forbearance period on $40,000 at 6.5%? You've just added $2,600 to your outstanding balance.

The single costliest assumption borrowers make is thinking forbearance or deferment "freezes" their entire loan. Only your payment obligation stops—interest calculations continue running daily on most loan types. String together multiple forbearance periods over the years and watch your balance swell beyond recognition.

How to Minimize Interest Accumulation on Student Loans

Savvy borrowers treat interest buildup as something preventable rather than inevitable. These approaches can slash your total interest costs substantially:

Pay interest throughout enrollment: Even modest monthly contributions on unsubsidized or private loans stop capitalization cold. Contributing just $50 monthly on a $5,000 loan at 6% throughout four undergraduate years saves approximately $800 in capitalized interest you'd otherwise carry.

Eliminate grace period accumulation: Those six months between graduation and your first required payment? That's prime real estate for wiping out accumulated interest before it gets permanently added to your principal. Eliminating that $900 we discussed earlier stops it from becoming part of your permanent balance.

Choose your repayment strategy carefully: Federal income-driven plans can dramatically reduce monthly payments but stretch repayment across 20-25 years, massively inflating your total interest costs. A $30,000 loan at 6% generates roughly $10,000 in interest charges over standard 10-year repayment. That same loan under 25-year income-driven repayment? You'll pay over $23,000 in interest.

Consider refinancing strategically: Private refinancing might lower your interest rate if you've built strong credit and secured stable employment. Reducing your rate by 2 percentage points on $50,000 saves around $6,000 across a 10-year timeline. But refinancing federal loans into private ones permanently eliminates income-driven repayment access, forbearance protections, and any possibility of forgiveness programs.

Prevent capitalization triggers: Interest gets capitalized at specific moments—grace period endings, exiting deferment, switching repayment plans, or defaulting. Whenever feasible, pay off accumulated interest right before hitting these trigger events.

Specify extra payment allocation: When submitting additional payments beyond your minimum, explicitly direct your servicer to apply them toward principal instead of simply advancing your next due date. Reducing principal shrinks the base amount your daily interest calculations use.

Students assume all federal loans work identically, which couldn't be further from reality. I regularly meet borrowers whose $25,000 unsubsidized loan balance became $30,000 by graduation purely through capitalization. Here's what's wild—even $25 monthly payments during college would've prevented most of that damage. Students just don't realize the meter's running

— Sarah Martinez

Common Mistakes That Increase Student Loan Interest Costs

Assuming federal loans all work the same: Many students think "federal loan" automatically means "subsidized loan." They don't verify their actual loan types, avoid making any payments during school, then discover four years' worth of capitalized interest waiting at graduation.

Misunderstanding grace periods: That six-month window isn't an interest-free vacation for most borrowers. People treat it like a complete break from loan responsibilities while interest quietly compounds and prepares to capitalize.

Creating unnecessary capitalization events: Some borrowers switch repayment plans repeatedly, each transition triggering capitalization. Every capitalization event permanently inflates principal and lifetime interest charges.

Prioritizing subsidized loan payments: When you're juggling both loan types on a tight budget, focus on knocking down unsubsidized balances first. They're accumulating interest faster since subsidized loans only generate charges during active repayment.

Treating forbearance as free: Forbearance solves immediate cash flow problems but creates long-term balance inflation. A single year of forbearance can add thousands to your final repayment total.

Overlooking private loan details: Private lenders differ dramatically on grace period terms, capitalization frequency, and in-school payment options. Assuming your private loan mirrors federal loan features leads to expensive surprises.

Forgetting disbursement timing: Interest calculations begin when money reaches your school's financial aid office, not when your semester calendar starts. Fall loans disbursed in mid-August start accumulating interest immediately, even if classes don't begin until early September.

Author: Evan Thornton;

Source: sonicmusic.net

Frequently Asked Questions About Student Loan Interest

When your student loans begin generating interest charges depends on which type you borrowed, but the financial consequences stay constant—understanding the timing protects your wallet. Subsidized federal loans provide the unusual advantage of government-covered interest during school and grace periods. Unsubsidized loans, PLUS loans, and private loans? They begin charging interest the moment funds get disbursed.

The financial gap between actively managing interest accumulation versus ignoring it represents thousands of dollars across your repayment timeline. Small strategic moves—covering interest-only payments during school, eliminating accrued interest before it capitalizes, selecting repayment plans carefully—compound into substantial savings.

Verify your specific loan types through your servicer's online portal or the National Student Loan Data System for federal borrowing. Calculate your current daily interest using your balance and rate. Even modest monthly contributions during school or grace periods stop the capitalization snowball that transforms manageable debt into a decade-long financial burden.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.