Person holding credit card looking at student loan bill on laptop screen with uncertain expression, money and credit symbols in background

Can You Pay Student Loans With a Credit Card?

If you've ever stared at a student loan bill and wondered whether you could just swipe a credit card to make it go away, here's the short answer: your loan servicer probably won't let you. The Department of Education banned federal loan servicers from taking credit cards years ago, and private lenders like Sallie Mae or Discover Student Loans won't process card payments either. They'll only pull money straight from your bank account.

But there's a workaround. Third-party companies will charge your Visa or Mastercard, then mail or wire the money to your loan servicer—charging you 2-3% for the privilege. Whether that makes any financial sense depends entirely on your situation. For 95% of borrowers, it's throwing money away. For the other 5% chasing credit card bonuses or juggling a cash crunch, it might be worth the hassle.

Let's break down when it works, when it doesn't, and what happens if you get it wrong.

Why Most Student Loan Servicers Don't Accept Credit Cards

Federal loan servicers—MOHELA, Aidvantage, Nelnet, EdFinancial—all operate under Department of Education mandates that explicitly forbid credit card processing. The government's reasoning? They don't want you piling 22% APR credit card debt on top of your 5% student loans. It's a borrower protection measure disguised as a policy restriction.

Transaction fees are the other sticking point. Visa and Mastercard take 2-3% of every swipe. On a $500 monthly payment, that's $10-15 vanishing into processing costs. Federal servicers won't eat those fees (taxpayers would ultimately cover them), and they won't charge borrowers extra either.

Private lenders have more freedom to set their own rules, but SoFi, Earnest, College Ave, and virtually every other major player refuse credit cards for the same reasons. Processing fees cut into their margins, and they've learned that borrowers who can't pay from a checking account are often one paycheck away from default. Why encourage risky behavior?

A handful of smaller lenders tested credit card acceptance back in 2015-2017, then quietly discontinued it after customer service costs ballooned and default rates spiked. Borrowers would max out cards to make loan payments, then default on both accounts within months.

So if you call your servicer asking to pay by card, expect a polite "no" followed by a suggestion to set up automatic bank transfers. Can i pay student loans with a credit card by calling the servicer? Not unless you've found one of the rare exceptions—and those are basically extinct now.

Author: Olivia Harrington;

Source: sonicmusic.net

Third-Party Payment Services That Allow Credit Card Payments

Several payment platforms will act as middlemen, accepting your credit card and forwarding payment to your loan servicer. They're not doing it out of charity—they charge fees that usually wipe out any rewards you'd earn.

How These Services Work

You sign up, enter your loan servicer's mailing address or ACH details, and link your credit card. The platform charges your card immediately, then either mails a physical check or initiates an electronic bank transfer to your servicer. Your servicer receives the money and credits your account like any other payment.

Timing varies wildly. Electronic transfers might post in 2-3 business days, while mailed checks can take a full week. Plan accordingly if your due date is approaching—a late fee will cost more than any rewards you're chasing.

One critical detail: some private lenders flag or outright reject third-party payments. Call your servicer first to confirm they'll accept payments from Plastiq or similar companies. Federal servicers generally accept them without issue, but you'll want written confirmation before paying a $50 transaction fee only to have the payment bounce back.

Fees and Costs to Expect

Every platform charges a percentage-based fee that starts around 2% and climbs from there. On a $1,000 payment, you're looking at $20-30 in fees before you've earned a single rewards point.

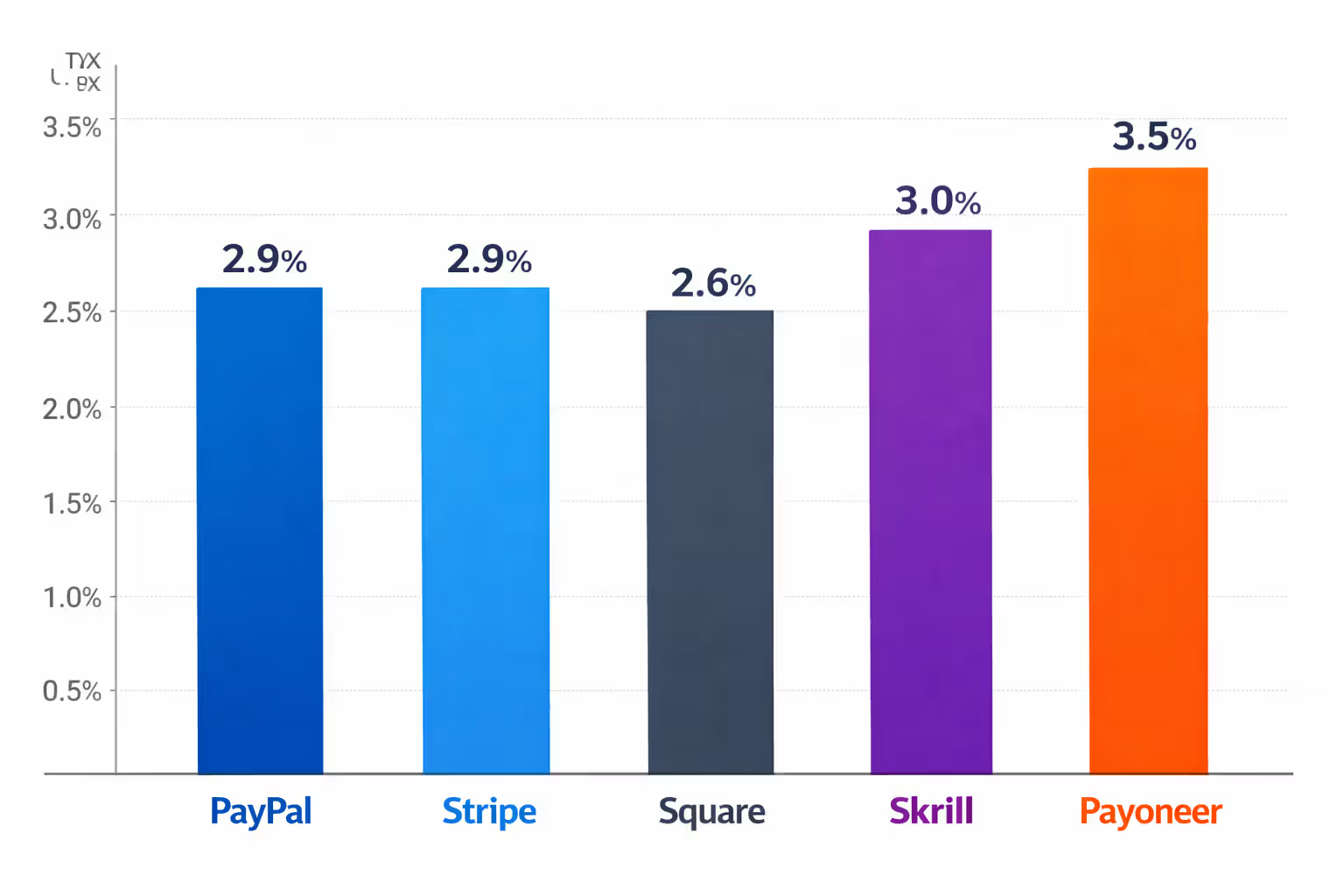

Here's what the major services currently charge:

| Platform | Fee Percentage | Accepted Cards | Payment Speed | Minimum | Maximum |

| Plastiq | 2.85% | Visa, MC, Amex, Discover | 3-5 days (ACH) or 5-8 days (check) | $100 | $200,000 |

| PayPal Key | 2.99% | Virtual MC generated by PayPal | 1-3 days | $10 | Depends on account limits |

| Melio | 2.9% | Visa, MC, Amex | 5-7 days via check | $50 | $100,000 |

| Venmo (business profiles) | 2.99% | Visa, MC, Amex, Discover | 1-3 days | $1 | $4,999.99 per transaction |

Plastiq occasionally drops fees to 1.5-2% during promotional periods for new accounts. If you spot one of these promos and you're using a card earning 2% or better, the math might actually work in your favor. Otherwise, you're paying $28.50 per thousand just to use your credit card.

Pay student loans with credit card services sound convenient until you calculate the real cost. That convenience fee doesn't count toward your loan principal—it's pure profit for the payment processor.

Author: Olivia Harrington;

Source: sonicmusic.net

Pros and Cons of Paying Student Loans With a Credit Card

This strategy has a terrible success rate, but it's not completely useless. You just need to know exactly what you're doing and why.

The potential upsides:

Credit card rewards: A card earning 2-3% back can theoretically offset transaction fees. If you're putting $5,000 on a card with 2.5% cash back, you'll get $125 back. Pay a 2.85% fee ($142.50) and you're down $17.50—but some premium travel cards earn 3x or 5x points in specific bonus categories, which changes the equation.

Sign-up bonuses: The real opportunity is hitting minimum spend requirements for new card bonuses. Cards like the Chase Sapphire Preferred require $4,000 spent in three months to earn 60,000 points (worth $600-900 depending on redemption). If you normally spend $2,000 monthly, a $3,000 student loan payment via Plastiq gets you there fast. Pay $85.50 in fees, earn rewards worth $600+, and you're ahead by $500+.

Emergency cash flow: You're between paychecks, your loan is due tomorrow, and overdrafting your checking account would cost $35. Charging the payment to a card buys you 21-25 days until your card bill is due. This only works if you'll definitely have cash by then—otherwise you're just delaying the problem.

0% APR opportunities: Some borrowers pay their loan with a card, then immediately transfer that balance to a different card offering 0% APR for 12-18 months. More on this below.

The very real downsides:

Guaranteed fee losses: Transaction fees are certain. Rewards are only valuable if you actually redeem them and they exceed the fees. Most casual cardholders don't optimize redemptions and end up losing money.

Credit card interest destroys the math: Carry a balance past your grace period and you're paying 18-25% APR on money that was costing you 5-7% in student loan interest. That's moving backward at high speed.

Credit utilization spikes: Drop $3,000 on a card with a $5,000 limit and your utilization jumps to 60%, which can knock 20-50 points off your credit score temporarily. Bad timing if you're applying for a mortgage next month.

Debt shell game: You haven't reduced what you owe—you've just moved it from one account to another. Now you're tracking two payment due dates, two interest rates, and two sets of late fees if something goes wrong.

Can you use a credit card for student loans without losing money? Only if you're methodically chasing a specific bonus, you pay the card off immediately, and you've done the math on paper first. Anything else is financial self-sabotage.

Author: Olivia Harrington;

Source: sonicmusic.net

Balance Transfers as an Alternative Strategy

Here's a smarter version of the same concept: pay your student loan with a credit card, then instantly transfer that balance to a different card offering 0% APR for 12-21 months. You'll pay a one-time balance transfer fee (usually 3-5%), then have over a year to pay off the balance interest-free.

Compare that to keeping money on your student loan at 6% interest. A $6,000 balance at 6% costs you about $540 in interest over 18 months. A balance transfer with a 3% fee costs $180 upfront. Pay off the card within the promotional window and you save $360.

Sounds perfect, right? Here are the catches that trip people up:

Credit limits cap your transfer amount: New credit cards typically come with $5,000-15,000 limits. You can't transfer a $30,000 loan balance even if you wanted to. This strategy only works for manageable chunks you can realistically pay off in 12-18 months.

You need strong credit: Cards offering 0% APR for 15+ months require credit scores above 700, usually closer to 740+. If your score is lower, you won't qualify for the offers that make this worthwhile.

One missed payment ruins everything: Most 0% APR cards include language letting them revoke the promotional rate if you pay late even once. Miss a due date and you're suddenly paying 24.99% APR retroactively or going forward, depending on the card terms.

You must pay it off before the promo ends: Transfer $8,000 with 18 months of 0% APR, then only pay $4,000 before the deadline. The remaining $4,000 starts accruing interest at the standard rate (20%+), and you've accomplished nothing except paying a 3% fee for the privilege.

This works beautifully for disciplined borrowers with small balances and concrete repayment plans. Transfer $4,000, set up automatic $230 monthly payments, and you'll clear the balance in 17 months with money to spare. Do it casually without a payment schedule and you'll still be carrying the balance three years later at 23% interest.

What Happens If You Miss Student Loan Payments

Using credit cards to cover student loans backfires spectacularly when borrowers who couldn't afford the loan payments suddenly can't afford the card payments either. Now you've got two debts spiraling instead of one.

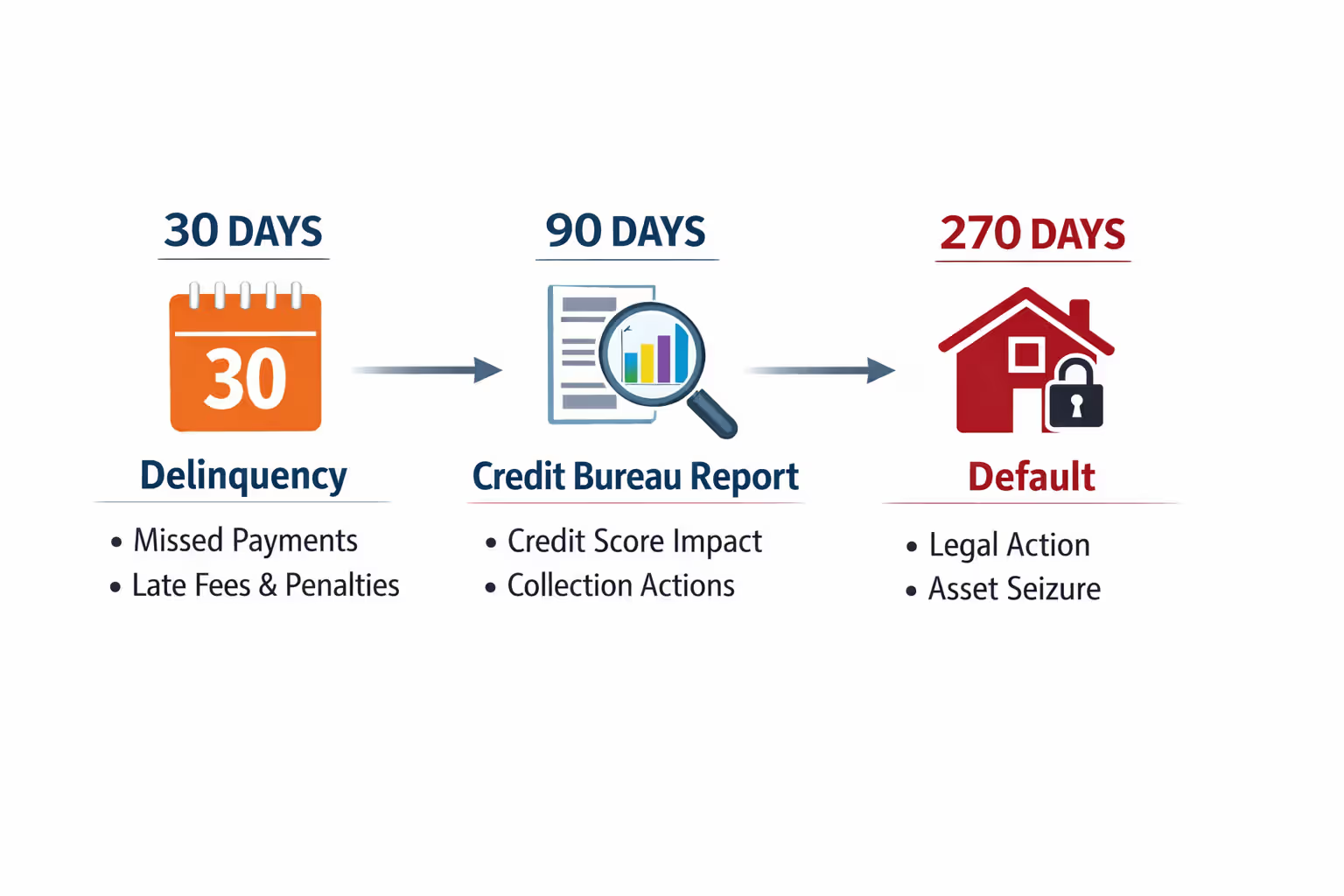

Federal loans have a 270-day fuse before default:

Your loan becomes delinquent after 30 days late, gets reported to credit bureaus at 90 days, and officially defaults at 270 days. Once you default, the government can garnish up to 15% of your wages without suing you, intercept tax refunds, and offset Social Security payments. Your credit score drops 100+ points, and that default sits on your report for seven years.

Federal loans also offer safety valves like income-driven repayment (payments as low as $0 if your income is low enough), deferment, and forbearance. If you bypass those options by paying with a credit card instead, you lose access to them when things get worse.

Private loans move faster:

Most private servicers report 30-day delinquencies to credit bureaus immediately and send accounts to collections after 90-120 days. Unlike federal loans, they have to sue you to garnish wages, but they will. Co-signers get dragged down with you—their credit tanks just as hard as yours.

Credit card debt compounds differently:

Miss a credit card payment and you'll face a $30-40 late fee, plus a penalty APR jumping to 29.99% on some cards. Credit card companies can't garnish wages without suing first, but they're faster to file lawsuits than federal loan servicers.

Here's the nightmare scenario: You charge $2,000 to a credit card to cover your student loan payment because you're short on cash. Next month you're even shorter because now you owe your loan servicer AND your credit card company. You cover the loan again with the card. By month three, you're carrying $6,000 in credit card debt at 22% APR, still owe your full student loan balance, and you're one paycheck away from defaulting on everything.

Author: Olivia Harrington;

Source: sonicmusic.net

Better Alternatives to Using Credit Cards for Student Loans

Instead of moving debt around, here are strategies that actually reduce what you owe or make payments more manageable.

Refinancing cuts your interest rate: If your credit's improved since you took out your loans, refinancing can drop your rate from 7% to 4% or lower. SoFi, Earnest, and Laurel Road all offer refinancing for federal and private loans. You'll lose federal protections like income-driven repayment and loan forgiveness eligibility, so refinance federal loans only if you're certain you won't need those safety nets.

Income-driven repayment slashes monthly payments: Federal loans offer four IDR plans capping payments at 10-20% of discretionary income. If you're earning $35,000 with $60,000 in loans, your payment might drop from $600 to $150 monthly. After 20-25 years, remaining balances get forgiven (currently taxable as income, but tax-free through 2025).

Employer repayment assistance is free money: The CARES Act lets employers contribute up to $5,250 yearly toward employee student loans tax-free through 2025. Companies like Fidelity, Aetna, and PwC offer this benefit. Ask your HR department whether your employer participates—you might be leaving money on the table.

Extra payments shrink total interest: Even $25-50 extra monthly makes a measurable dent over time. On a $20,000 loan at 6% with a standard 10-year term, adding $50 monthly saves you $1,700 in interest and pays the loan off 18 months early. Critical detail: tell your servicer to apply extra payments to principal, or they'll automatically advance your due date instead, which doesn't save you a penny in interest.

Temporary forbearance prevents default: Federal loans let you pause payments for up to 12 months via forbearance or deferment during financial hardship. Interest keeps accruing (except on subsidized loans during deferment), but you avoid default and credit damage. It's a bridge option, not a solution, but it beats derailing your entire financial life.

Nonprofit credit counseling is actually helpful: Organizations accredited by the National Foundation for Credit Counseling offer free debt counseling. They'll review your budget, explain your options, and help you spot predatory solutions. They're not selling you anything—they genuinely help people avoid debt traps.

These approaches address the actual problem: either you can't afford your payments or you're paying too much interest. Can you pay student loans with a credit card guide advice should always start with these options before even mentioning credit cards.

Using a credit card to pay student loans only makes sense if you can pay off the balance immediately and earn rewards that exceed the processing fees. For most borrowers, it's a financial trap disguised as a convenience

— Michael Chen

Frequently Asked Questions

Yes, you can technically pay student loans with a credit card by routing payments through third-party services. Should you? Almost certainly not—unless you fit one of the very specific scenarios where the math actually works in your favor.

Federal servicers block credit cards by design, and private lenders follow suit voluntarily. The workaround costs you 2-3% in transaction fees every single time, which immediately cancels out typical credit card rewards. For the strategy to make financial sense, you need exceptional circumstances: chasing a valuable sign-up bonus, accessing a lengthy 0% APR period you'll fully utilize, or earning outsized rewards you'll actually redeem.

Most borrowers considering this route are facing cash flow problems that credit card debt will only multiply. Trading 5% student loan interest for 22% credit card interest isn't problem-solving—it's problem multiplication. Your loan balance doesn't shrink when you pay it with a credit card; you're just creating a second debt with worse terms and shorter time horizons.

Look at alternatives first: refinancing to lower your rate, switching to income-driven repayment to drop your monthly payment, finding employer assistance, or simply making extra principal payments when you can afford them. These strategies reduce your actual debt burden instead of shuffling it between accounts.

If you're still convinced paying with a credit card makes sense, put your plan on paper: calculate exact fees, confirm your servicer accepts third-party payments, know precisely when and how you'll pay off the card balance, and have a backup plan if your income gets disrupted. If your plan depends on everything going perfectly for 12-18 months straight, it's not a plan—it's a hope.

Debt management is about reducing total interest paid and maintaining flexibility when life throws curveballs. Credit card payments for student loans might sound clever, but the math rarely cooperates. Focus on strategies that actually move you toward being debt-free, not just reorganizing which accounts show balances.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.