Young professional reviewing student loan documents at desk with calculator and financial charts

Average Student Loan Debt Guide

If you've borrowed money for college, you've probably wondered: is everyone else drowning in debt too, or is it just me?

Here's the reality—millions of Americans carry education debt, but the numbers swing wildly. What you owe for a bachelor's degree looks nothing like what someone with a medical degree faces. Parents who borrowed for their kids' education deal with entirely different loan terms than recent graduates. Even the type of school you attended—public university versus private college—creates dramatically different financial situations.

Let's break down what borrowers actually owe across the country and what these figures mean for your wallet.

What Is the Average Student Loan Debt in 2026?

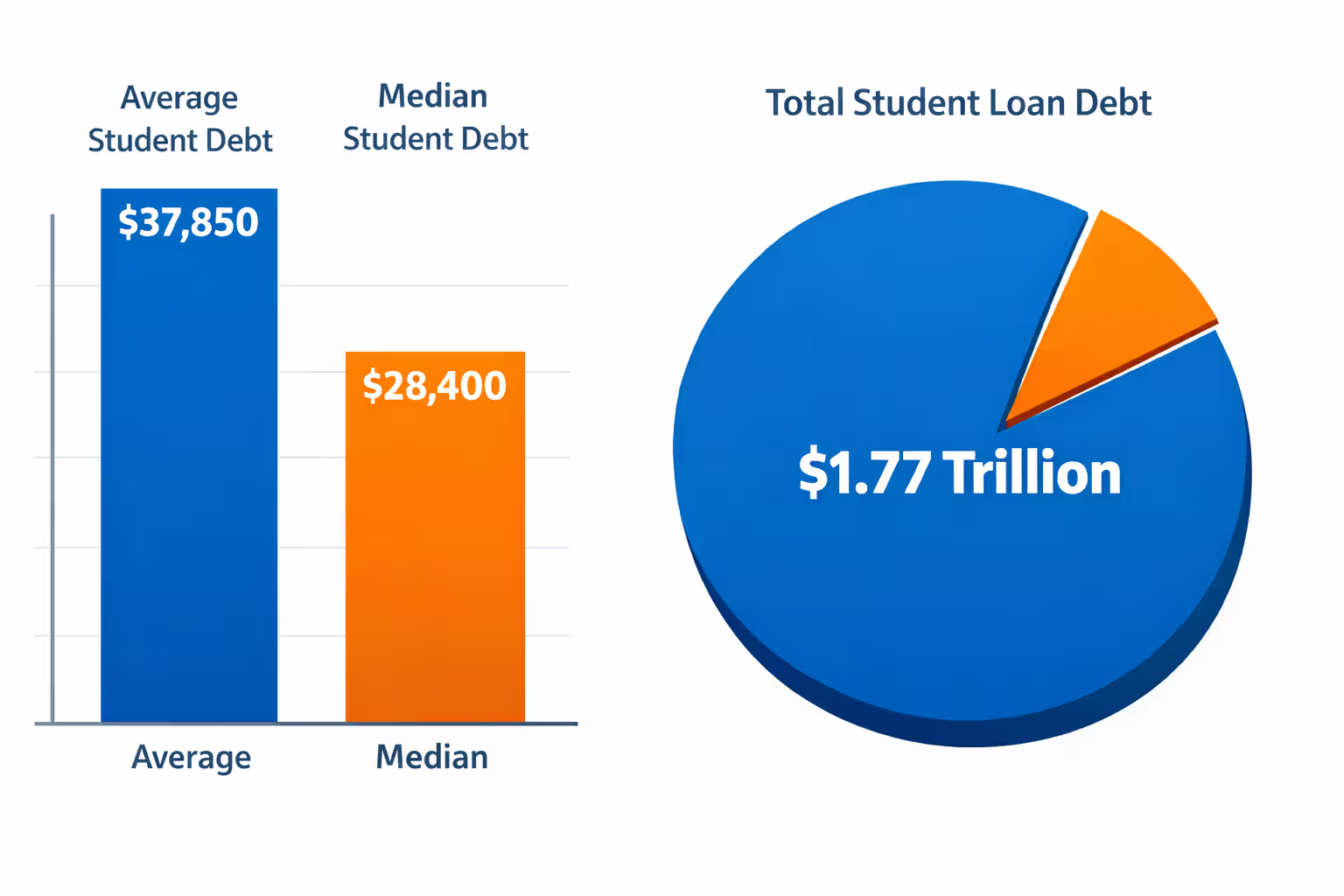

Right now, the typical borrower who finished their degree owes $37,850. That's the mean—add up everyone's debt and divide by the number of people.

But here's where it gets interesting. The median sits at $28,400. Half of all borrowers owe less than this; half owe more. Notice the $9,000+ gap? That happens because borrowers with $200,000+ in medical or law school debt pull the average way up, even though most people owe significantly less.

Americans collectively owe $1.77 trillion in education loans. About 43 million people carry this debt. The federal government holds roughly 92% of it—the rest comes from private lenders like banks.

And those who started college but never finished? They typically owe around $14,500. Smaller number, sure, but they're stuck with debt and no degree to boost their earning power. That's often the worst situation to be in.

Average Student Loan Debt by Borrower Type

Author: Marcus Bennett;

Source: sonicmusic.net

Who borrowed the money matters as much as how much they borrowed. Different loan programs serve different groups, with separate rules and limits.

Undergraduate Borrowers

Students who finished a four-year degree and borrowed to pay for it graduate owing about $29,700 on average. That includes both federal and private loans.

Go to a public university? Expect closer to $27,200. Attended a private nonprofit school? You're looking at roughly $33,600.

Why the difference? Federal rules limit how much dependent undergraduates can borrow each year—$5,500 as a freshman, $6,500 as a sophomore, $7,500 for junior and senior years. These caps keep most undergrads from racking up six-figure federal debt, though private loans can push totals higher if families take that route.

Independent students—those over 24, married, or with kids of their own—can borrow an extra $4,000 to $5,000 annually in unsubsidized federal loans. That's why their balances typically run a bit higher.

Graduate and Professional Degree Holders

Graduate school is where debt really explodes. Earn a master's degree? You're carrying about $71,300 on average if you borrowed for both undergrad and grad school. Get a PhD? That jumps to $102,000, though it varies wildly by field.

Professional degrees create the steepest mountains of debt. Medical school graduates who borrowed average $202,000. Law school adds roughly $145,000 on top of whatever undergrad debt you brought along. Dental school? Try $292,000 by the time you're done.

Why so high? Graduate students can borrow up to their school's full cost of attendance (minus any scholarships or aid) through Grad PLUS loans. No cap. That open spigot explains these eye-watering balances.

Parent Borrowers

About 3.7 million parents took out federal Parent PLUS loans to help pay for their children's education. They owe an average of $28,900 per child. Many borrowed for multiple kids, which means their household total climbs much higher.

Parent PLUS loans carry worse terms than regular student loans—8.05% interest versus 5.50% for undergraduates. Parents also get fewer flexible repayment options. They do face a credit check, though it's fairly lenient compared to private loans.

How Student Loan Debt Varies by Degree and School Type

Your school choice and the degree you pursued completely reshape your debt picture.

| Degree Level | Typical Debt at Completion | Entry-Level Salary | Debt-to-Income Ratio |

| Associate | $16,200 | $42,000 | 0.39:1 |

| Bachelor's | $29,700 | $58,500 | 0.51:1 |

| Master's | $71,300 | $77,000 | 0.93:1 |

| Doctoral | $102,000 | $95,000 | 1.07:1 |

| Medical | $202,000 | $68,000 (residency pay) | 2.97:1 |

| Law | $145,000 | $82,000 | 1.77:1 |

Community college students getting two-year associate degrees finish with the smallest debt loads—around $16,200 on average. Many attend part-time while working, which cuts down borrowing needs for living expenses.

Four-year bachelor's programs show huge variation by school type. Public universities send graduates out with $27,200 in debt typically. Private nonprofit colleges push that to $33,600. For-profit institutions—despite enrolling fewer students overall—produce bachelor's recipients owing $43,500 on average.

State flagship universities usually fall somewhere in the middle of the public range. Regional public universities often cost less. Specialized private colleges can stick you with $40,000+ in debt even for an undergraduate degree.

Graduate credentials show the craziest variation. A master's in education might add $35,000. An MBA from a top-tier program? That can tack on $120,000 or more. Clinical psychology doctoral programs often span six or seven years and generate debt exceeding $150,000, despite pretty modest starting salaries in many therapy settings.

Author: Marcus Bennett;

Source: sonicmusic.net

Average Monthly Payment and Repayment Timeline

The standard federal repayment plan spreads your balance over 10 years. Quick math: every $1,000 you borrowed costs roughly $12 per month at today's interest rates (around 5.5%).

So the average bachelor's degree holder owing $29,700? They'll pay about $356 monthly. Over that decade, they'll hand over approximately $42,700 total—meaning $13,000 goes purely to interest.

Graduate borrowers face much steeper bills. Someone with $71,300 in debt pays roughly $854 each month on the standard plan. That's $102,500 over 10 years. Medical school graduates sitting on $202,000? They'd owe $2,424 monthly—completely impossible for residents earning $68,000 annually.

That's where income-driven repayment enters the picture. These plans recalculate your payment based on what you actually earn, typically taking 10% of your discretionary income (the amount you make above 150% of the poverty line). A single borrower earning $58,500 would pay around $315 monthly under these plans, no matter how much total debt they're carrying.

The catch? These plans stretch repayment to 20 or 25 years. Whatever remains after that gets forgiven, though you might owe taxes on the forgiven amount. Borrowers on income-driven plans with average debt often end up paying the full term because their monthly payments don't cover accumulating interest in the early years.

Refinancing through private lenders can slash your interest rate if you've got strong credit and income. Some borrowers cut years off their repayment and save thousands in interest this way. But refinancing federal loans into private ones means kissing goodbye to income-driven plans, forbearance options, and any shot at forgiveness programs.

Author: Marcus Bennett;

Source: sonicmusic.net

Why the Average Amount of Student Loan Debt Keeps Rising

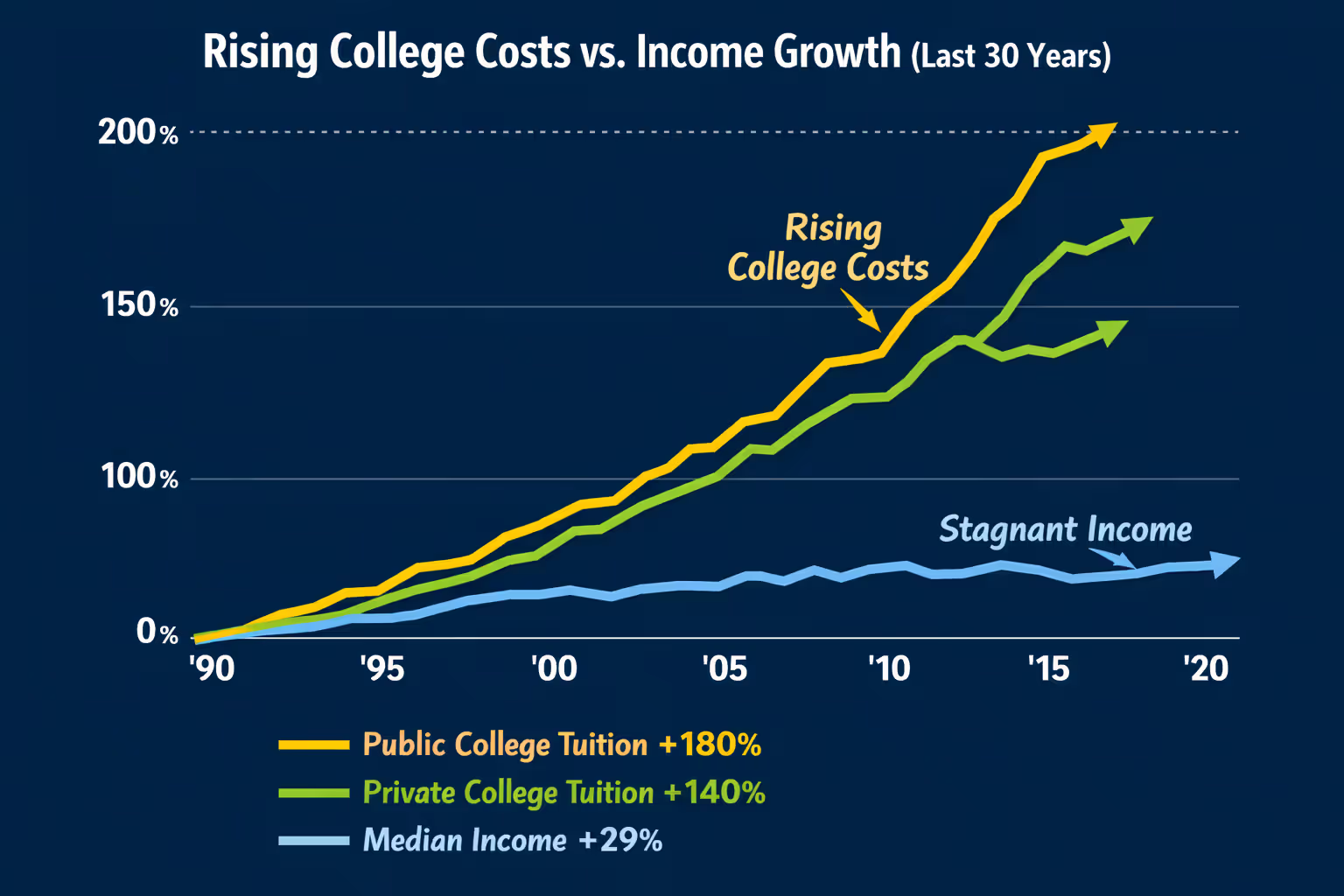

Tuition at public four-year schools has jumped 180% over the past 30 years after accounting for inflation. Private nonprofit tuition climbed 140% in the same stretch. Meanwhile, wages? They've grown just 29% in real terms.

State governments slashed higher education funding after the 2008 recession. They never really restored it. Today, states provide 13% less money per student than in 2008, forcing public universities to make up the difference through tuition hikes.

The student population has shifted too. Graduate enrollment has grown faster than undergraduate enrollment, and grad students borrow way more. Back in 1995, graduate students accounted for 11% of student loan dollars. Now? Nearly half—48%.

Living expenses while in school add thousands to borrowing needs. Room and board at four-year institutions averages $12,700 per year. Students living off-campus in expensive cities often borrow additional thousands for rent, transportation, and groceries.

Federal loan limits haven't budged. The annual cap for dependent first-year undergrads has stayed frozen at $5,500 since 2008. When federal loans don't cover the bills, students turn to pricier private loans or push their parents toward PLUS loans.

Credential inflation in the job market pushes more students toward graduate degrees. Jobs that once required a bachelor's now prefer or require a master's. Career-minded students feel forced to add extra years of education—and debt.

The average debt figures mask significant disparities in who borrows and how much. Low-income students borrow at higher rates and for larger amounts relative to their family resources, while wealthy students often graduate debt-free. This means student debt both reflects and reinforces existing economic inequality

— Dr. Rachel Fishman

How Much Student Loan Debt Is Too Much?

Financial advisors usually recommend keeping total student debt below your expected first-year salary. Planning to earn $55,000 out of school? Try to limit borrowing to that amount or less.

The debt-to-income ratio gives you a clearer picture. Monthly student loan payments shouldn't eat up more than 10-15% of your gross monthly income. At 15%, someone earning $55,000 annually ($4,583 monthly) should pay no more than $687 toward student loans.

Using that $12 per month per $1,000 borrowed rule, this means total debt shouldn't exceed about $57,250 for someone making $55,000. Cross that threshold and you'll likely need an income-driven repayment plan just to keep your head above water.

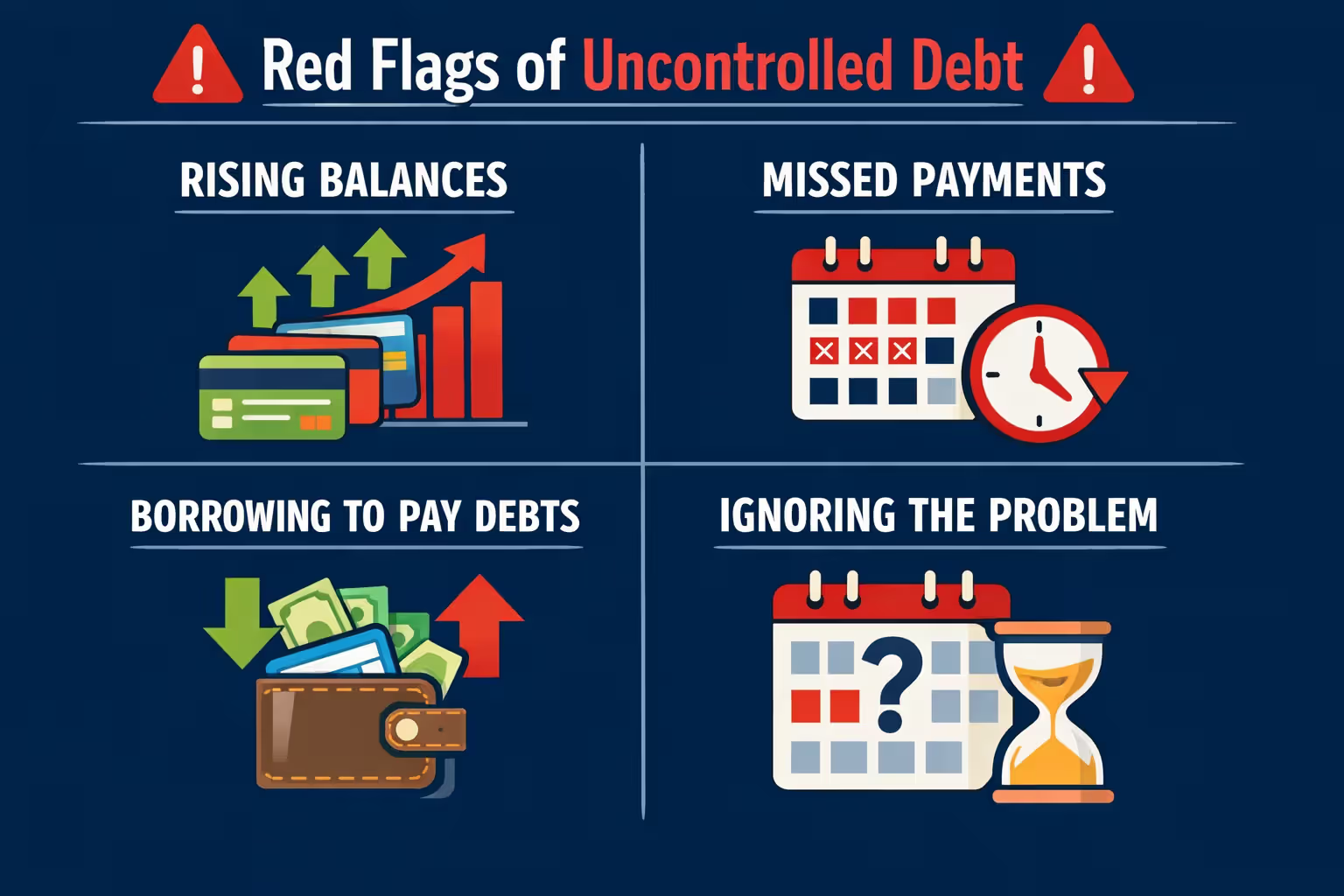

Red flags that debt has become unmanageable:

You can't cover minimum payments without repeatedly entering forbearance or deferment. These exist for temporary rough patches, not chronic budget shortfalls.

Your balance grows despite making payments. Income-driven plans sometimes set monthly payments below the interest that's accruing, causing negative amortization. While this might work short-term, watching your balance climb year after year messes with your head.

You're postponing major life decisions like buying a home, starting a family, or switching careers purely because of student loan payments. Some delay makes sense, but indefinitely shelving important goals means debt is running your life.

You're defaulting on other bills to make student loan payments. Choosing student loans over rent, utilities, or medical care signals an unsustainable situation demanding immediate adjustment to a different repayment plan.

Some careers justify higher debt loads. Physicians eventually earn enough to handle $200,000+ in debt, though residency years require careful planning. Engineers, computer scientists, and others in high-paying fields can similarly manage above-average debt.

On the flip side, degrees in modest-earning fields—social work, education, counseling—make even average debt burdensome. A social worker earning $48,000 with $65,000 in loans faces a brutal financial path without forgiveness programs.

Public Service Loan Forgiveness offers relief for government and nonprofit employees, wiping out remaining federal balances after 120 qualifying payments. Teachers at low-income schools can access separate forgiveness after five years. These programs make higher debt loads workable for people committed to lower-paying public service careers.

Author: Marcus Bennett;

Source: sonicmusic.net

Frequently Asked Questions About Student Loan Debt Averages

Comparing your debt to national averages provides helpful context, but it shouldn't control your emotions or strategy. Someone with $25,000 in debt but limited earning potential faces tougher challenges than someone with $80,000 and a high-paying career.

Focus on your debt-to-income ratio and monthly payment burden rather than the raw dollar figure. If payments fit comfortably within 10-15% of gross income, you're in manageable territory whether you're above or below average.

Struggling with payments? Income-driven repayment plans offer immediate relief by capping payments at an affordable percentage of income. These work particularly well for borrowers in public service careers who can eventually pursue forgiveness.

Borrowers with solid income and credit should explore refinancing to cut interest rates, potentially saving thousands over the loan's life. This strategy works best if you're confident you won't need federal protections like income-driven plans or forbearance down the road.

The average student loan debt reflects decades of policy choices, economic shifts, and changing educational expectations. Your individual debt tells a different story—shaped by your choices, circumstances, and goals. Understanding where you stand relative to others provides perspective, but building a repayment strategy that works for your specific situation matters infinitely more than any national benchmark.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.