Young professional holding tax form with calculator and laptop in background

Are Student Loans Tax Deductible Guide

Every January, millions of borrowers open their mailboxes to find tax forms from their loan servicers. Most toss them aside, assuming student loan payments don't matter come tax time. Big mistake—though not for the reason you'd hope.

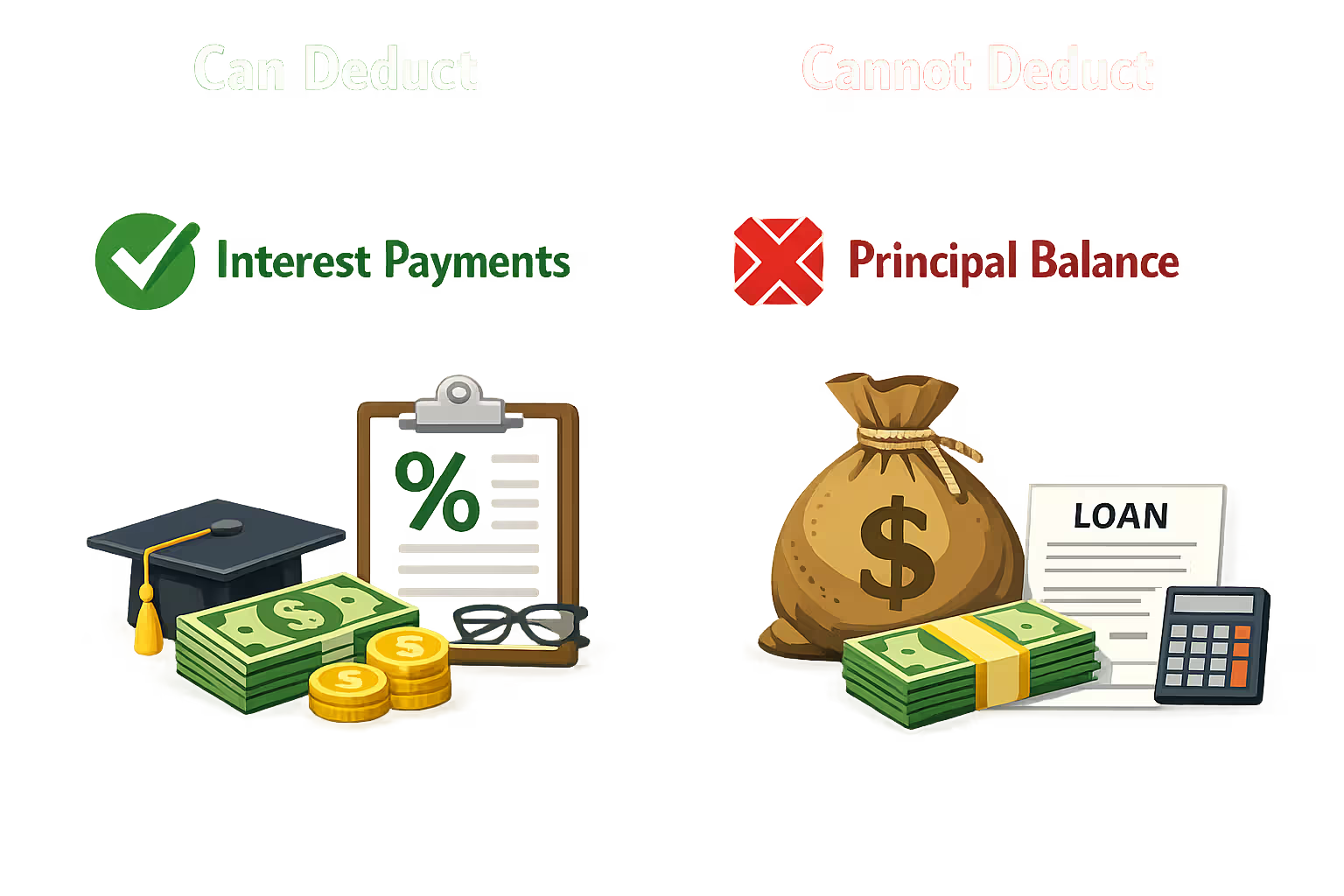

Your $800 monthly payment? Can't deduct it. The $10,000 you paid toward your balance last year? Same story—no tax break. But buried in those payments sits something the IRS does care about: the interest charges.

That interest can slash your taxable income by up to $2,500 each year. Someone paying 22% in federal taxes who maxes out this deduction keeps an extra $550 that would've gone to Uncle Sam. Not life-changing money, but enough to cover several months of Netflix and groceries.

Before you get excited, know this: qualifying means threading through a maze of income caps, filing restrictions, and dependency rules that trip up even careful filers. Let's walk through who actually gets this break and how to claim it without errors.

What Student Loan Tax Deductions Actually Cover

Search for "are student loans a tax write off" and you'll find plenty of borrowers who think their full monthly payment counts toward a deduction. Time for bad news: the money repaying what you originally borrowed (called principal) does absolutely nothing for your tax return.

The IRS exclusively cares about interest—and only particular types. This means interest you're legally obligated to pay on loans financing education. Your loan, your spouse's loan, or loans for someone you claimed as a dependent when the money was borrowed.

Which education expenses qualify? More than you'd guess. Obviously tuition and mandatory fees count. Less obvious: your dorm room or off-campus apartment rent, the $400 biology textbook that made you wince, lab equipment, meal plans, even gas money getting to campus. The expenses just need to support at least half-time enrollment in a program leading to a degree or credential at a qualifying school. One catch exists—total costs can't balloon past the institution's published cost of attendance figure.

Tax deductions for student loans come with specific no-go zones. Borrowed $15,000 from your parents at 5% interest with a signed promissory note? Doesn't count, even with perfect documentation. Taking a loan from your employer's 401(k) plan for education? Also disqualified.

Both federal loans and private ones work, assuming they meet the rules. Refinanced your loans last year? That's fine too—provided every penny of the new loan paid off qualifying education debt. Took out an extra $5,000 during refinancing for credit card bills? You'll need to calculate what portion of your interest relates to the original student loans versus that cash-out amount.

Author: Danielle Pierce;

Source: sonicmusic.net

Who Qualifies for the Student Loan Interest Deduction

Student loans and taxes deduction rules stack multiple requirements together. Fail even one test and the whole thing collapses.

First test: you must legally owe the money. Making voluntary payments on someone else's loans—including your own child's—generates zero deduction for you. Your name needs to appear on the promissory note as a borrower or co-borrower.

Dependency status confuses thousands of filers annually. Maybe you graduated in May, got a job in June, and have been living independently since. But if your parents claim you as a dependent on their tax return for that year, you cannot claim this deduction. Period. Even if you made every single payment from your own checking account. Twist the knife: your parents can't claim it either in this scenario, despite claiming you.

Your filing status builds walls around eligibility. Married couples filing separately face an absolute ban—zero exceptions regardless of income, who has the loans, or who pays. Single filers, heads of household, qualifying surviving spouses, and married couples filing jointly all remain eligible, assuming they clear other hurdles.

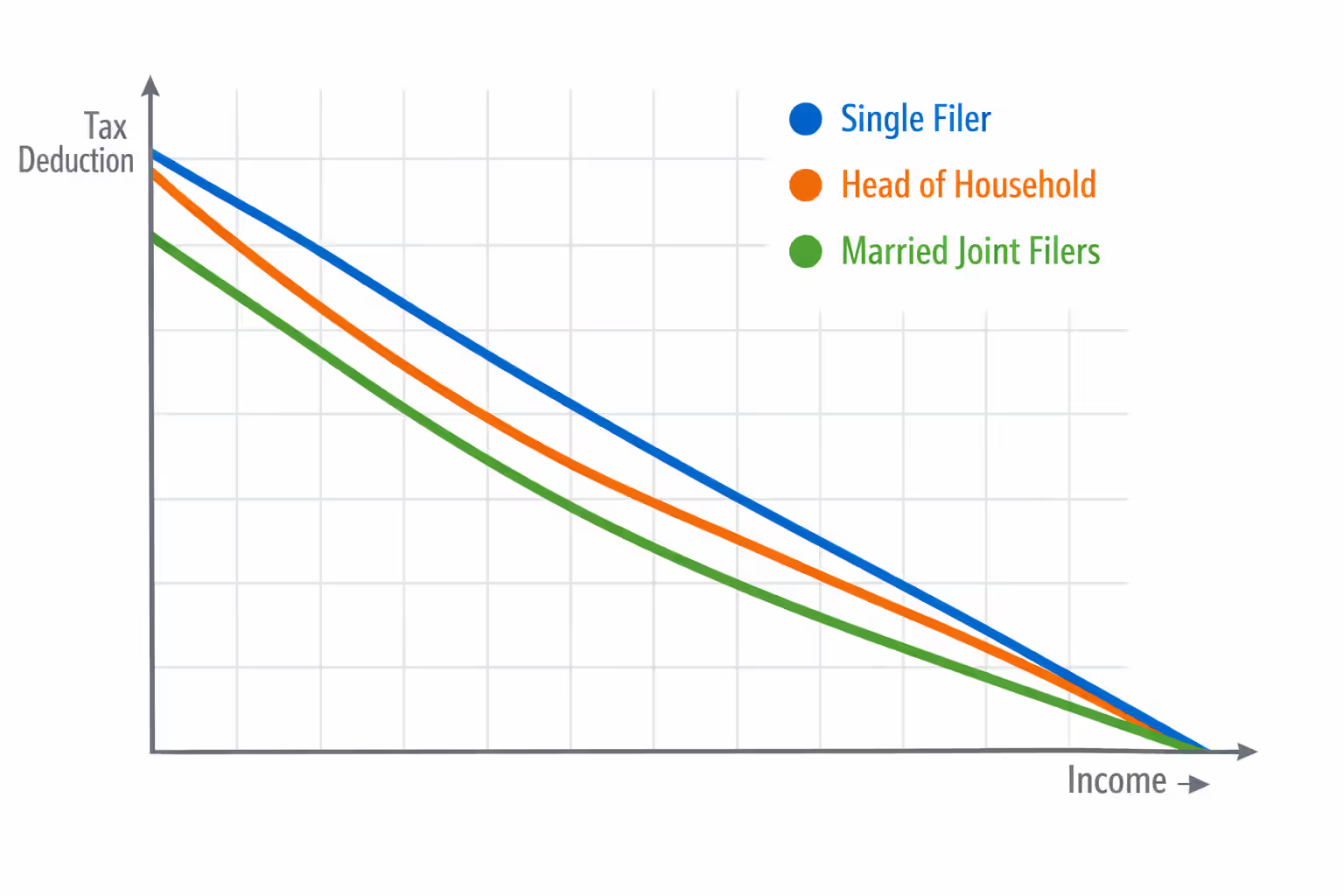

Income creates the steepest barrier because the deduction doesn't simply disappear at a threshold—it slowly fades. This gradual elimination surprises borrowers who landed a promotion mid-year or switched to a higher-paying job.

Income Phase-Out Ranges for 2026

The IRS adjusts these numbers periodically based on inflation. Current limits for 2026 tax returns:

| Filing Status | MAGI Where Phase-Out Starts | MAGI Where Deduction Disappears | Maximum Possible Deduction |

| Single | $80,000 | $95,000 | $2,500 |

| Head of Household | $80,000 | $95,000 | $2,500 |

| Married Filing Jointly | $165,000 | $195,000 | $2,500 |

| Qualifying Surviving Spouse | $165,000 | $195,000 | $2,500 |

| Married Filing Separately | Not allowed | Not allowed | $0 |

Income below the starting threshold means you can claim the full deduction (up to $2,500 or whatever you actually paid, whichever is less). Fall somewhere in the middle range and your deduction shrinks proportionally. Cross the upper boundary and the deduction evaporates completely.

Take someone filing single with modified adjusted gross income hitting $87,500. They've landed exactly halfway through the phase-out zone, cutting their maximum deduction to roughly $1,250—half the usual $2,500 cap.

Author: Danielle Pierce;

Source: sonicmusic.net

Disqualifying Filing Statuses

Married filing separately stands completely alone as the one typical filing status that automatically disqualifies you. Income becomes irrelevant. You could earn $20,000 and pay $2,800 in interest—still get nothing.

Couples sometimes file separately when one spouse carries heavy itemized deductions or when filing separately shields one partner from the other's tax problems. Just understand this choice immediately eliminates the student loan interest deduction for both of you, zero wiggle room. The math works out favorably only when other significant factors heavily favor separate returns.

How Much You Can Deduct from Student Loan Interest

The ceiling sits at $2,500 per tax return—not per loan, not per person. Married couples filing jointly hit this same $2,500 maximum even when both spouses carried their own loans and paid interest on separate debt all year.

Can you write off amounts exceeding that cap? No. Pay $3,700 in interest and you still max out at a $2,500 deduction. Conversely, pay only $950 in interest and that's your deduction—$950.

This deduction reduces your adjusted gross income rather than cutting your tax bill directly. Your actual tax savings hinges on your bracket. Someone taxed at 24% claiming the full $2,500 saves approximately $600 in federal taxes ($2,500 × 0.24). Lower brackets generate smaller savings, but money is money.

You can only deduct interest you actually paid during the tax year. Borrowers on income-driven repayment plans sometimes see their monthly payments fail to cover all accumulating interest. Deduct only what actually left your account—not what piled onto your balance.

Loan origination fees need attention. These upfront charges technically qualify as prepaid interest, making them deductible—but you spread them across the loan's entire life. A 1% origination fee deducted from your $30,000 disbursement means you'd deduct roughly $30 annually on a 10-year repayment timeline.

Capitalized interest—unpaid interest your servicer tacks onto your principal—becomes deductible later, specifically the year you finally pay it down.

Made extra payments beyond the minimum? As long as those dollars went toward interest (not exclusively principal), they count toward your deduction. Most servicers automatically route extra payments toward principal first, so you might need to specify you want those additional dollars applied to interest if maximizing your deduction matters to you.

How to Claim the Student Loan Interest Deduction

Can you deduct student loans on taxes without itemizing deductions? Absolutely—making this benefit unusually accessible. You don't sacrifice your standard deduction to claim this. Tax professionals label this an "above-the-line" adjustment, meaning it shrinks your adjusted gross income before you even choose between itemizing or taking the standard deduction.

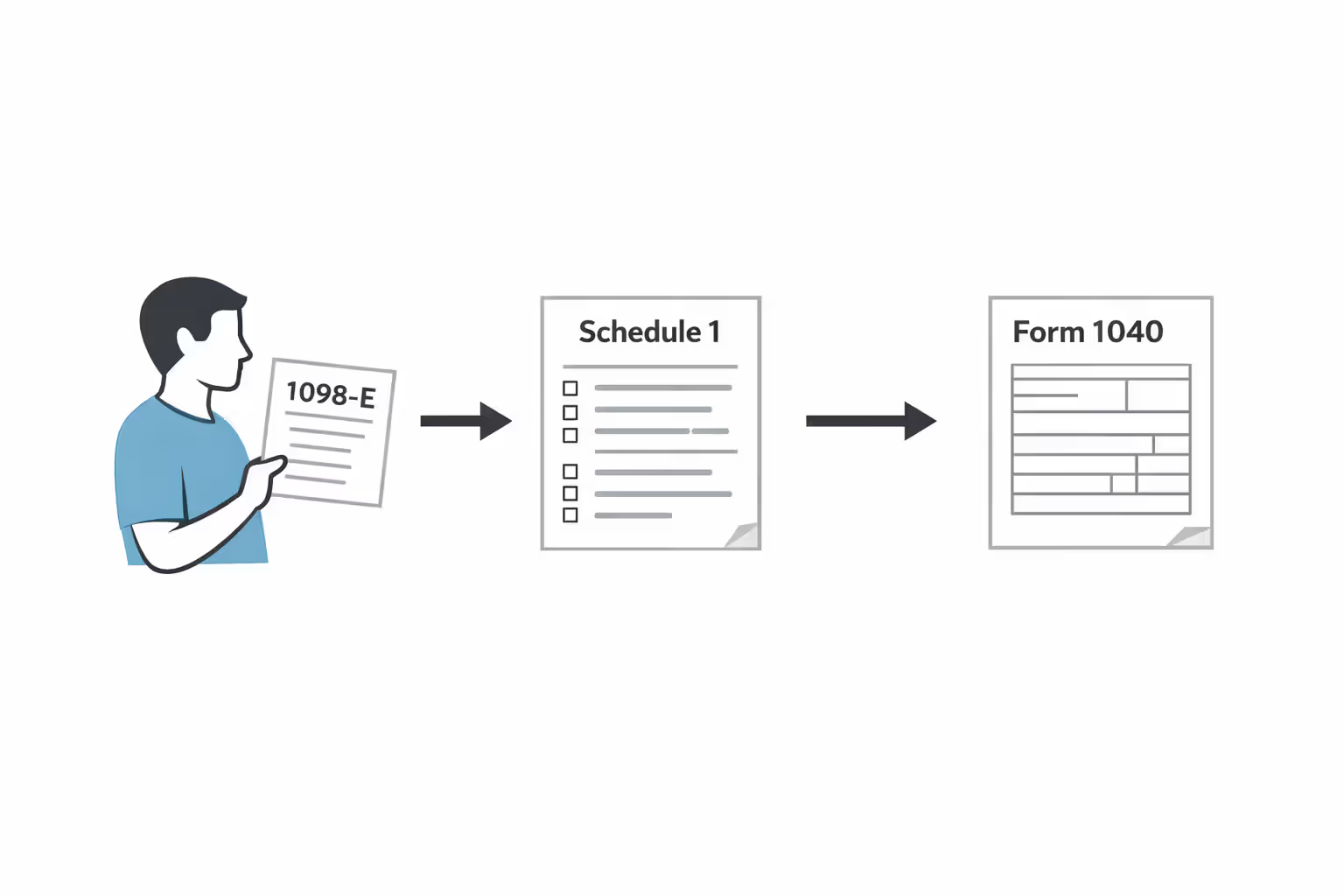

Your loan servicer mails or emails Form 1098-E by early February, assuming you paid at least $600 in interest during the prior year. Box 1 displays your total interest. Box 2 shows whether any interest came from loans originated before September 2004, which affects certain edge-case borrower scenarios.

Report the deduction on Schedule 1 (Additional Income and Adjustments to Income), which attaches to Form 1040. Line 20 of Schedule 1 is where you enter the amount—it flows through to reduce your adjusted gross income on your main 1040 form.

Here's the step-by-step: grab the figure from Box 1 of your 1098-E, apply any reduction based on income phase-outs, enter the final number on Schedule 1. Tax software handles calculations automatically once you input your 1098-E details and income figures.

Juggling loans with three different servicers? You'll receive separate 1098-E forms from each. Add up all the interest totals—though remember, your combined deduction still caps at $2,500.

Plenty of servicers now provide 1098-E forms exclusively online instead of mailing paper copies. Haven't spotted yours by mid-February? Log into your servicer's website to download it directly.

Author: Danielle Pierce;

Source: sonicmusic.net

Common Mistakes That Disqualify Your Deduction

The most frequent blunder? Trying to deduct principal payments. When your annual statement shows $7,200 in payments, it's tempting to assume that whole amount helps your tax situation. Your servicer's year-end breakdown separates principal from interest—exclusively the interest line matters for your deduction.

Income increases disqualify countless borrowers who haven't verified whether recent raises pushed them past the limits. That promotion you received in August might bump your modified adjusted gross income into the phase-out zone or beyond, shrinking or eliminating your deduction entirely. Always confirm current year limits before claiming anything.

The dependency trap snags many recent graduates. You file your own return while your parents still claim you as a dependent—especially common for students who graduated mid-year or turned 24 late in the tax year. In this situation, neither you nor your parents can claim the student loan interest deduction, even when you're making every payment yourself or your parents co-signed the loan.

Family loans create another pitfall. Your parents loaned you money for college, drafted a formal promissory note, and charged market-rate interest. That interest still fails to qualify for the deduction. The lender must be a legitimate institution—banks, credit unions, federal government, or educational institutions themselves.

Employer-paid student loan interest requires careful handling. Some companies pay up to $5,250 annually toward employee student loans (a provision extended through 2025). While that benefit is fantastic, you cannot claim a tax deduction for interest your employer paid directly. The IRS forbids double-dipping.

Modified adjusted gross income calculations confuse some filers. MAGI starts with your AGI, then adds back specific items: foreign earned income exclusion, foreign housing deductions, and certain territorial income exclusions. Most taxpayers lack these adjustments—their AGI and MAGI match exactly. But when you work abroad or have unusual income sources, calculate carefully.

Student Loan Tax Deduction vs. Other Education Tax Benefits

Understanding are student loans tax deductible explained requires seeing how this deduction fits alongside other education tax breaks. The tax code offers multiple benefits, and grasping how they interact helps you maximize savings.

The American Opportunity Tax Credit hands you up to $2,500 per eligible student, though exclusively during the first four undergraduate years. Unlike deductions, credits slash your tax bill dollar-for-dollar, making them substantially more powerful. Even better: $1,000 of the AOTC is refundable—the IRS sends you money even when you owe no tax.

The Lifetime Learning Credit offers up to $2,000 per tax return for qualifying education expenses. No restriction on years of education—graduate programs, professional degrees, and even job skill courses all count. It provides less benefit than the AOTC but reaches more people in more situations.

Good news: you can claim the student loan interest deduction in the same year you claim either education credit, provided you independently qualify for each. They target different expenses—credits apply to tuition and fees you paid during the current year, while the deduction applies to interest on loans possibly taken years earlier. They don't interfere with each other.

However, you must pick between the AOTC and LLC for any individual student in any given year. You can't layer both for the same person.

Income restrictions vary across these benefits. The AOTC phases out starting at $90,000 for single filers and $180,000 for joint filers in 2026—higher than the student loan interest deduction limits. The LLC mirrors those AOTC phase-out ranges.

Picture this scenario: A married couple filing jointly earns $170,000 MAGI. Their daughter attends college, generating tuition bills. They also carry their own older student loans from graduate school. They can claim the AOTC for their daughter's current tuition (potentially receiving $2,500 in credits) plus deduct up to $2,500 in interest they paid on their own decades-old loans. That's potentially $5,000 in combined tax benefits.

Many taxpayers leave money on the table by not claiming all the education tax benefits available to them. The student loan interest deduction is particularly overlooked because it doesn't require itemizing. I've seen clients save $400 to $600 annually just by claiming this one deduction they didn't know existed. When combined strategically with education credits, families can significantly reduce their tax burden during the expensive college years and beyond

— Jennifer Martinez

Frequently Asked Questions About Student Loan Tax Deductions

The student loan interest deduction delivers tangible tax relief for millions of borrowers navigating repayment. While you can't write off principal payments, the interest deduction—maxing out at $2,500 annually—remains accessible even when taking the standard deduction, making it easier to claim than many tax breaks.

Qualification hinges on several factors aligning simultaneously: legal obligation to pay the interest, not being claimed as anyone's dependent, filing with an eligible status (anything except married filing separately), and keeping modified adjusted gross income within allowable ranges. For 2026, single filers begin losing the deduction at $80,000 and lose it completely at $95,000, while joint filers phase out between $165,000 and $195,000.

Claiming the benefit is straightforward—use Form 1098-E from your servicer and report the amount on Schedule 1 attached to your 1040. This deduction stacks with education credits like the American Opportunity Tax Credit or Lifetime Learning Credit, potentially delivering thousands in combined tax benefits when multiple education-related expenses align in one year.

Avoiding common pitfalls protects your deduction: don't claim principal payments, verify you're not being claimed as a dependent elsewhere, check that your income hasn't exceeded limits, and ensure your loans came from legitimate lenders rather than family members. Maintain accurate payment records, particularly when you paid under $600 in interest and won't receive Form 1098-E automatically.

Student loan debt strains household budgets across the country. Understanding and leveraging available tax benefits provides modest but meaningful relief. Review your eligibility annually, since changing circumstances—salary increases, marriage, refinancing, or reaching the age where parents can no longer claim you as a dependent—all affect qualification. Every legitimate deduction and credit you claim reduces your tax liability, freeing up cash you can redirect toward eliminating your loans faster.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.