Student reviewing college acceptance letter and tuition costs at desk

How Do Student Loans Work for College Students?

Picture this: acceptance letter in hand, tuition bill arriving next week, and your savings account showing $1,247. Welcome to the reality facing 43 million Americans who've turned to student loans. Most borrowers sign their first loan documents with only a foggy idea of what happens next—where the cash actually goes, why that balance keeps growing, or what that monthly bill will look like in four years.

Let's walk through the complete journey of a student loan, from clicking "submit" on your application to making that final payment years down the road.

What Are Student Loans and Who Qualifies

Think of student loans as money you're borrowing today against your future income, specifically earmarked for college costs—your tuition bill, textbooks, dorm room, meal plan, even your off-campus apartment and gas money.

Here's what sets them apart from other money: you have to pay them back, with added charges called interest. Nobody's giving you free money like with a Pell Grant or a scholarship from your local Rotary Club.

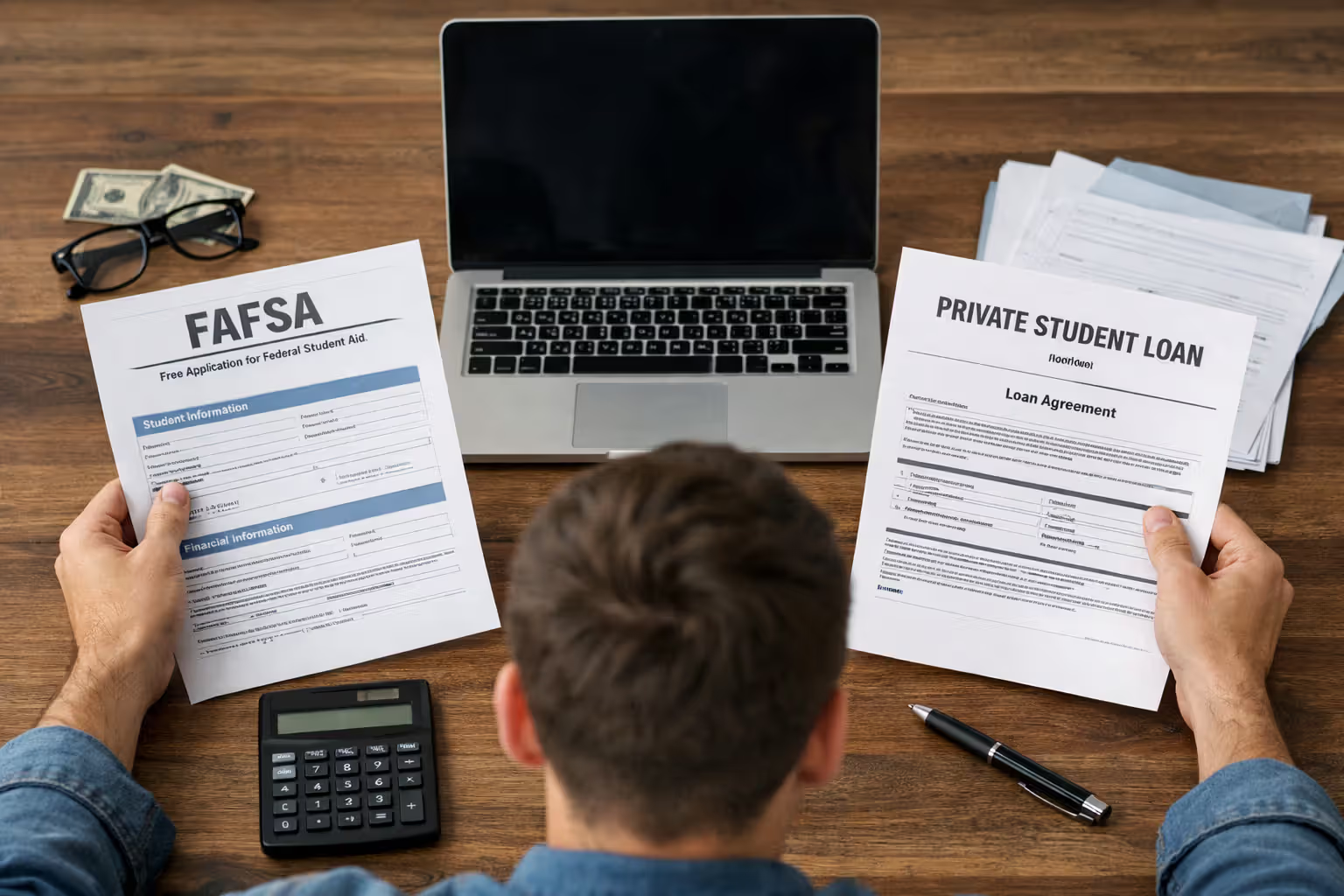

You'll encounter two distinct loan universes. Federal loans come from the U.S. Department of Education, backed by taxpayer dollars. Private loans come from Wells Fargo, Discover, Sallie Mae, your local credit union, or dozens of other financial companies. How does a student loan work differently between these two? Almost everything changes—the application, the interest rate, your repayment flexibility, even whether you need Mom or Dad to co-sign.

The federal government offers three loan flavors. Subsidized Direct Loans target undergrads who can demonstrate financial need; here's the sweet part—Uncle Sam covers your interest charges while you're taking classes (provided you're enrolled at least half-time). Unsubsidized Direct Loans open up to both undergrads and grad students with zero financial need requirements, but your interest clock starts running the moment money hits your school's account. PLUS Loans fill the gap for graduate students and parents helping their dependent kids; these require passing a credit review and let you borrow much larger amounts.

Who gets approved for federal loans? You need citizenship or eligible immigration status, a Social Security number, acceptance into a degree or certificate program, and grades that meet your school's satisfactory academic progress standards. Men between 18 and 25 face one extra hurdle: Selective Service registration. The beautiful thing about Direct Subsidized and Unsubsidized Loans? No credit check. An 18-year-old with absolutely zero credit history qualifies just like everyone else.

Private lenders operate more like car loan companies. They pull your credit report, examine your income, calculate your existing debts against your earnings. How loans for students work in the private space means most undergrads hit a wall—you typically need someone with established credit and steady income to cosign, usually a parent or guardian putting their credit score on the line alongside yours.

The government caps how much you can borrow. In 2026, dependent undergrads max out at $5,500 to $7,500 annually depending on your year in school. Independent students and those whose parents got denied for PLUS Loans can access up to $12,500 per year. Private lenders often bridge the gap when federal limits don't cover your school's sticker price, but that convenience carries consequences.

Author: Danielle Pierce;

Source: sonicmusic.net

The Student Loan Application Process Step-by-Step

The student loan borrowing process forks into two completely different roads based on whether you're chasing federal or private money.

Completing the FAFSA

Every federal loan starts with the Free Application for Federal Student Aid. The online form opens each October 1st for the following school year. Timing matters more than most students realize—certain aid gets distributed first-come, first-served until the money runs dry.

Gather your documentation first: Social Security card, driver's license number, federal tax returns from two years prior (applying for 2026–27 aid means pulling your 2024 tax data), your W-2s, documentation of any untaxed income streams, and current balances on your savings and investment accounts. Dependent students need their parents to provide the same financial snapshot.

The application crunches these numbers to generate your Expected Family Contribution—now rebranded as the Student Aid Index. Your college's financial aid office receives this number and builds your personalized aid package showing grants, federal work-study eligibility, and loan offers.

Here's where students make their first major mistake: accepting every dollar offered. Your aid letter might offer $12,500 in loans, but after subtracting your $6,000 Pell Grant, $2,000 state grant, and the $3,000 your parents can contribute, you only need $8,000. Accept less than the maximum and you'll thank yourself later.

First-time federal borrowers must complete entrance counseling (roughly 30 minutes of educational content explaining your obligations) and electronically sign a Master Promissory Note. This MPN legally binds you to repay the loan and stays active for up to ten years of additional borrowing at the same institution.

Author: Danielle Pierce;

Source: sonicmusic.net

Applying for Private Student Loans

Each private lender runs their own application portal, but the student loan process explained for private borrowing follows a predictable pattern.

Start with comparison shopping. Interest rates might span from 4.99% to 13.99% depending on your credit profile. Origination fees vary—some lenders charge nothing, others take 5% off the top. Repayment terms stretch from 5 to 20 years. Cosigner release policies differ wildly (can you get Mom off the hook after two years of payments, or never?).

Applications request your personal details, your school's information, how much you need, and financial documentation. You'll designate your cosigner during this stage. The lender runs credit checks on both of you, scrutinizing credit scores, income sources, current debt obligations, and employment stability.

Approvals can ping back in 60 seconds or take a full week. Once approved, you receive a disclosure statement spelling out your interest rate, any fees, your repayment terms, and the total amount you'll repay over the loan's life. Federal law mandates a three-day cooling-off period before money moves, giving you time to change your mind.

The lender sends a certification request to your school's financial aid office to verify you're actually enrolled and confirm the school's total cost of attendance. This safeguard prevents you from borrowing $50,000 when your school only charges $30,000. After certification clears, the lender schedules disbursement to sync with your school's academic calendar.

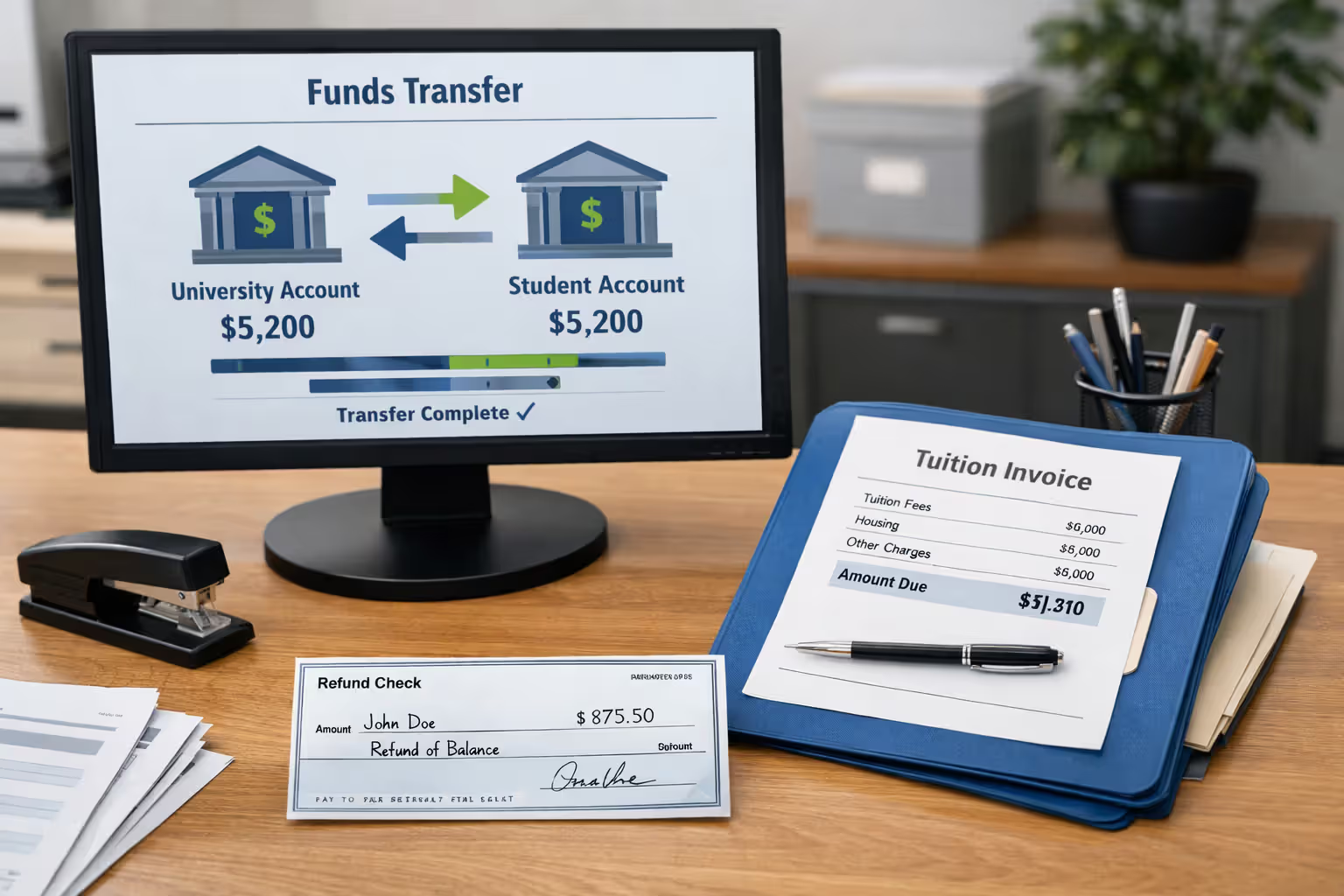

How Student Loan Money Is Disbursed to Your School

Disbursement describes the actual money transfer, and the mechanics surprise first-time borrowers.

Federal loans split into at least two payments, typically one installment per semester or quarter. Borrowed $5,500 for the full academic year? Expect $2,750 dropping in August and another $2,750 in January. Private lenders usually follow this same split-disbursement model, though some release funds in a single payment for shorter certificate programs.

Here's what doesn't happen: no one hands you a check or deposits money into your personal checking account (not initially, anyway). Lenders wire funds directly to your institution's bursar or student accounts office. The school applies this money to your outstanding balance—tuition first, then mandatory fees, then campus housing and meal plans if you live on campus.

When loan money exceeds your direct school charges, you get the leftover amount as a refund. This usually processes one to two weeks into the semester, after the add/drop deadline passes and your enrollment gets confirmed. Schools issue refunds through direct deposit (if you've set it up) or mail paper checks.

That refund check legally covers education-related expenses: your off-campus rent payment, textbooks from Amazon, your laptop that died sophomore year, gas for commuting, groceries. Technically, loan terms permit all these uses. Realistically, students sometimes blow refunds on weekend trips or restaurant meals, then wonder why they're $40,000 in debt four years later with a $25,000-per-year job offer.

First-time federal borrowers face a mandatory 30-day waiting period before their initial disbursement. If you're a first-year student taking out your first federal loan ever, your school cannot release loan funds until 30 days after your program start date. This creates a potential cash flow gap requiring temporary out-of-pocket payment or emergency payment plan arrangements with your bursar's office.

Author: Danielle Pierce;

Source: sonicmusic.net

Understanding Interest Rates and How They Accumulate

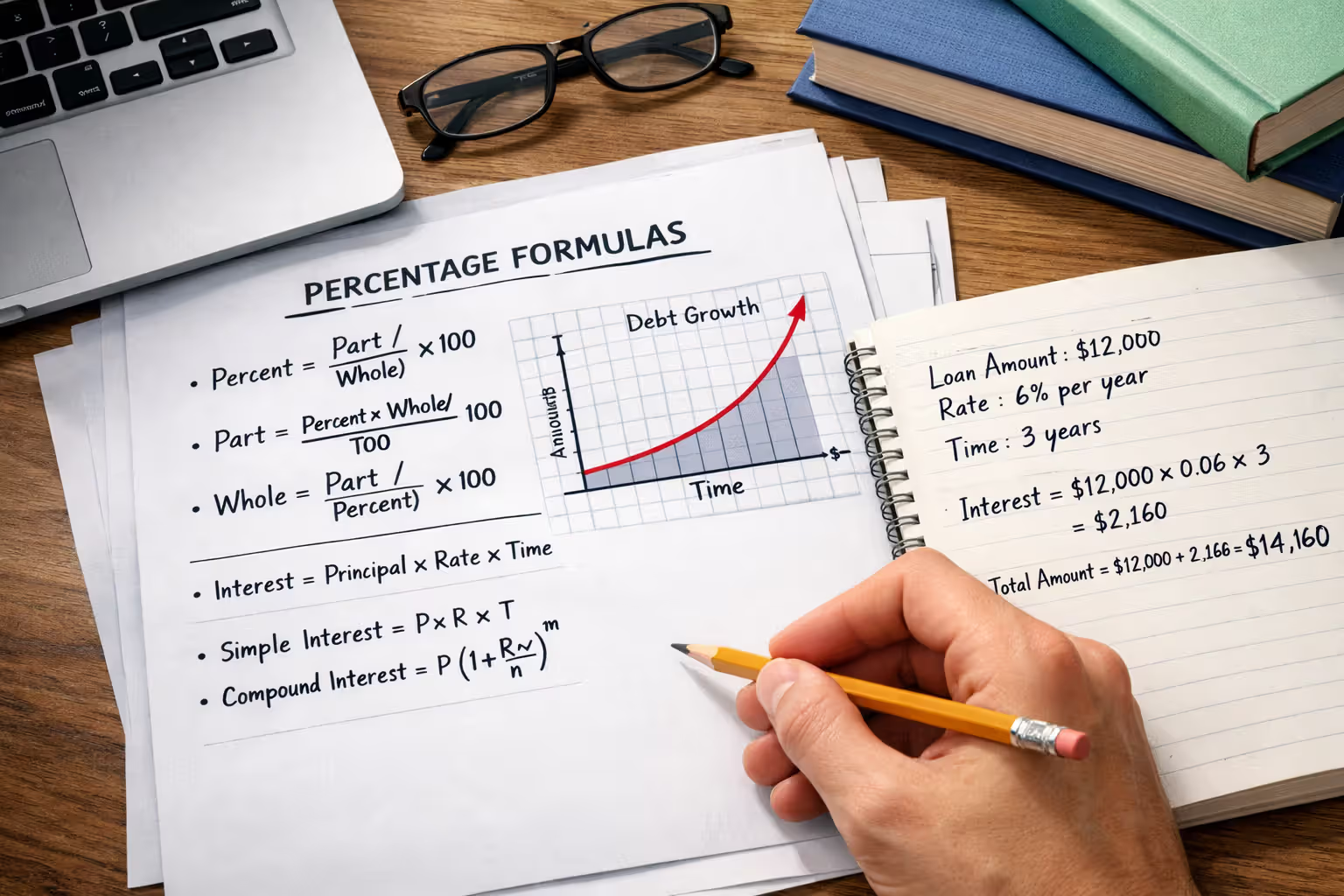

Interest represents the price tag on borrowed money, calculated as a percentage of your outstanding balance. How student loans work explained through an interest lens requires understanding several moving parts.

Federal student loan rates stay fixed—Congress sets them annually using a formula tied to the 10-year Treasury note auction in May plus statutory add-on percentages. For loans disbursed between July 1, 2025, and June 30, 2026, rates landed at 5.50% for undergraduate Direct Subsidized and Unsubsidized Loans, 7.05% for graduate Unsubsidized Loans, and 8.05% for PLUS Loans. Lock in your rate at disbursement and it never changes, regardless of whether the Federal Reserve raises or lowers rates during your repayment.

Private loan rates come in two varieties. Fixed rates cement in place for your entire repayment period. Variable rates bounce up and down monthly or quarterly based on an index (usually SOFR—the Secured Overnight Financing Rate) plus a margin reflecting your creditworthiness. That variable rate might start at an attractive 4.99% but could balloon to 12% or higher over a 15-year repayment if interest rates climb. This unpredictability complicates long-term budgeting.

Interest charges accrue daily using this calculation: (outstanding principal × interest rate) ÷ 365 = daily interest. Take a $10,000 loan at 5.50%—you rack up roughly $1.51 in charges each day.

Direct Subsidized Loans deliver a powerful benefit: the federal government covers your accruing interest while you're enrolled at least half-time, throughout your six-month grace period, and during approved deferment periods. This subsidy saves borrowers thousands of dollars over the loan's lifespan.

Every other loan type—Unsubsidized, PLUS, and all private loans—starts accruing interest the moment funds disburse. Ignore those charges while you're in school and they capitalize when you enter repayment. Capitalization means unpaid interest gets added to your principal balance, and you start paying interest on interest. Your $10,000 loan with $2,000 in accumulated interest transforms into a $12,000 loan at capitalization, substantially increasing your total repayment burden.

You can make interest-only payments during school to stop capitalization. Even modest monthly payments—$50 or $100—dramatically reduce your total amount owed after graduation.

Author: Danielle Pierce;

Source: sonicmusic.net

When and How Student Loan Repayment Begins

The how do student loans work guide wouldn't tell the complete story without explaining when bills actually arrive in your mailbox (or inbox).

Federal loans include a six-month grace period starting the day after you graduate, officially withdraw, or drop below half-time enrollment. Your first payment comes due six months and 21 days from your grace period start date. Graduate in May 2026? Your first payment would hit late December 2026.

Interest keeps accruing during grace periods on unsubsidized and PLUS loans (but not subsidized loans). Use these six months strategically: select your repayment plan, enable autopay for the interest rate discount, and build a small emergency fund.

Private loan grace periods vary dramatically by lender. Some match the federal six-month grace. Others provide only three months. A few require immediate repayment the day after graduation. Your promissory note specifies your particular grace terms.

Federal borrowers choose from multiple repayment structures. The Standard Repayment Plan spreads equal monthly payments across 10 years. Graduated Repayment launches with lower payments that increase every two years, still wrapping up in 10 years. Extended Repayment stretches the timeline to 25 years for borrowers carrying more than $30,000 in Direct Loans, shrinking monthly payments but dramatically inflating total interest paid.

Income-driven repayment plans—including SAVE, IBR, PAYE, and ICR—calculate monthly payments based on your discretionary income (the amount you earn above 225% of federal poverty guidelines) and household size, typically capturing 5% to 10% of that discretionary income. Make qualifying payments for 20 or 25 years and the government forgives whatever balance remains, though you might owe income tax on the forgiven amount.

Private lenders typically offer rigid repayment terms: 5, 10, 15, or 20 years. Shorter terms mean fatter monthly payments but far less total interest paid. Some lenders permit one or two term changes during your loan's life.

Enrolling in autopay usually earns a 0.25% interest rate reduction with both federal servicers and private lenders. Over the life of a $50,000 loan, this quarter-point discount can save you $800 or more.

Federal vs. Private Student Loans Comparison

| Feature | Federal Student Loans | Private Student Loans |

| Application Process | Single FAFSA application unlocks all federal aid; Direct Subsidized/Unsubsidized require no credit review | Separate applications for each lender; credit evaluation required for all |

| Interest Rates | Congress sets fixed rates annually; every borrower within a loan type gets identical rates | Fixed or variable options; rates determined by creditworthiness; typically range 4% to 14%+ |

| Repayment Options | Eight different plans including four income-driven options; terms from 10 to 25 years | Usually limited to 5, 10, 15, or 20-year terms; minimal flexibility |

| Eligibility | U.S. citizenship or eligible immigration status, enrollment at least half-time; most require no credit check | Credit evaluation mandatory; undergraduate borrowers typically need creditworthy cosigners |

| Borrowing Limits | Annual caps of $5,500–$12,500 for undergraduates depending on year and dependency status; lifetime maximums apply | Up to certified cost of attendance minus other financial aid; varies significantly by lender |

| Cosigner Requirements | Never required for Direct Subsidized/Unsubsidized Loans; PLUS Loans don't use cosigner model | Almost universally required for undergrads; some lenders offer release after 24–48 on-time payments |

| Forgiveness Programs | Public Service Loan Forgiveness, Teacher Loan Forgiveness, IDR balance forgiveness after 20–25 years | Rarely available; most lenders only offer death or total disability discharge |

| Fees | Origination fees deducted from disbursement: 1.057% for Direct Subsidized/Unsubsidized; 4.228% for PLUS (2025–26 rates) | Varies dramatically; many charge zero fees; some deduct up to 5% upfront |

Common Student Loan Mistakes to Avoid

Borrowers repeatedly trip over the same obstacles, costing themselves thousands in unnecessary interest and years of financial stress.

Over-borrowing sits at the top of the mistake list. Your school offers $12,500 in loans but you only need $8,000 after grants, scholarships, and family contributions? Decline the excess $4,500. That refund check feels like winning a small lottery until repayment begins. Borrow for actual need, not perceived wants.

Ignoring loan types creates expensive problems. Students sometimes accept Unsubsidized loans before maxing out their Subsidized loan eligibility, voluntarily giving up the interest subsidy. Others grab private loans before exhausting federal options, sacrificing access to income-driven repayment plans and Public Service Loan Forgiveness.

Missing grace period details triggers shock when that first bill arrives. Calendar your grace period end date and configure your repayment plan at least 30 days before your first payment is due.

Skipping private lender comparison shopping can cost you full percentage points on your rate. A 7% rate versus a 5% rate on a $40,000 loan over 10 years translates to roughly $5,000 more in interest charges. Invest two hours comparing at least three lenders.

Neglecting to update your contact information with your loan servicer means missing critical notices about repayment plans, forbearance eligibility, or forgiveness opportunities. Log into your servicer portal at least once per semester to verify your address, email, and phone number remain current.

Ignoring your loans while enrolled represents a missed opportunity. Making even $25 monthly payments throughout a four-year undergraduate program can save $2,000 or more in capitalized interest.

Students frequently fixate exclusively on covering this semester's tuition bill.But financially successful students understand their loan's complete lifecycle before signing anything—how interest accumulates, when repayment starts, what their actual monthly payment will be after graduation. That knowledge fundamentally changes borrowing behavior

— Jennifer Martinez

Frequently Asked Questions Aut Student Loans

Student loans function as a time machine for your money—converting your expected future earnings into immediate purchasing power for educational expenses. The process flows through predictable stages: submit applications, meet eligibility requirements, accept specific loan offers, watch funds route through your school's accounting office, and eventually repay principal plus interest over years or decades.

These mechanics matter enormously because small decisions compound dramatically over time. Choosing Subsidized over Unsubsidized when eligible saves real money. Making interest payments during enrollment prevents capitalization. Selecting the appropriate repayment plan keeps monthly obligations within reach. Comparing private lenders can shave full percentage points off your rate.

Treat student loans as a powerful tool, not an inevitable trap. Borrow intentionally for genuine need, thoroughly understand your obligations, and plan your repayment strategy from day one. The degree you're financing should boost your earning potential enough to justify the debt burden—calculate the numbers before signing any promissory notes. Student loans work when you strategically work the system rather than stumbling through it blindly.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.