Graduate student reviewing tuition bills and loan documents at a desk

Graduate Student Loans Guide

Content

Content

Grad school costs serious money. Whether you're pursuing an MBA, law degree, PhD, or medical training, you're looking at price tags that can exceed $100,000 for many programs. Recent data from the Education Data Initiative shows the typical grad student leaves school with over $76,000 in borrowed funds—and that figure climbs much higher for professional programs like medicine or dentistry.

Here's what catches people off guard: borrowing for graduate programs works completely differently than undergrad loans. You'll face higher limits, steeper rates, and rules that flip everything you learned about student loans the first time around. Those differences matter because they'll follow you for 10, 20, or even 25 years after you finish your degree.

Most people cobble together money from several sources. You might get a teaching assistantship covering half your tuition, borrow federal loans for the rest, and maybe tap into private lending if there's still a gap. How you structure this mix—and which loan programs you choose—creates either a manageable situation or a financial mess that follows you into your 40s.

This guide walks you through the real mechanics of financing grad school: which federal programs exist, what they actually cost right now, how to navigate the application maze, when private loans make sense, how repayment works in practice, and which mistakes cost borrowers the most money.

What Are Graduate Student Loans?

These are specialized financing tools built for anyone enrolled at least half-time in post-bachelor's programs—masters, doctorates, professional degrees, all of it. Three big differences separate them from undergraduate borrowing: you can borrow way more money, the government won't pay your interest during school, and some programs check your credit.

For federal loan purposes, you're a graduate student once you've finished your bachelor's. MBA candidates qualify. So do law students, medical students in didactic training, PhD candidates in year six of their dissertation, master's students in education, social work, engineering—basically any post-bachelor's program. Professional programs like dentistry, pharmacy, and veterinary medicine count too. Students in these intensive programs often borrow $200,000 or more because the cost of attendance is astronomical and the programs prohibit substantial outside work.

The subsidized loan cutoff hits hardest. Undergrads can access Direct Subsidized Loans where Uncle Sam covers their interest while they're in school. Congress axed that benefit for grad students back in 2012 through the Budget Control Act. Every dollar you borrow for grad school starts accumulating interest the day it hits your account. Writing your thesis? Interest accruing. Doing clinical rotations? Interest accruing. Six-month grace period after graduation? Still accruing.

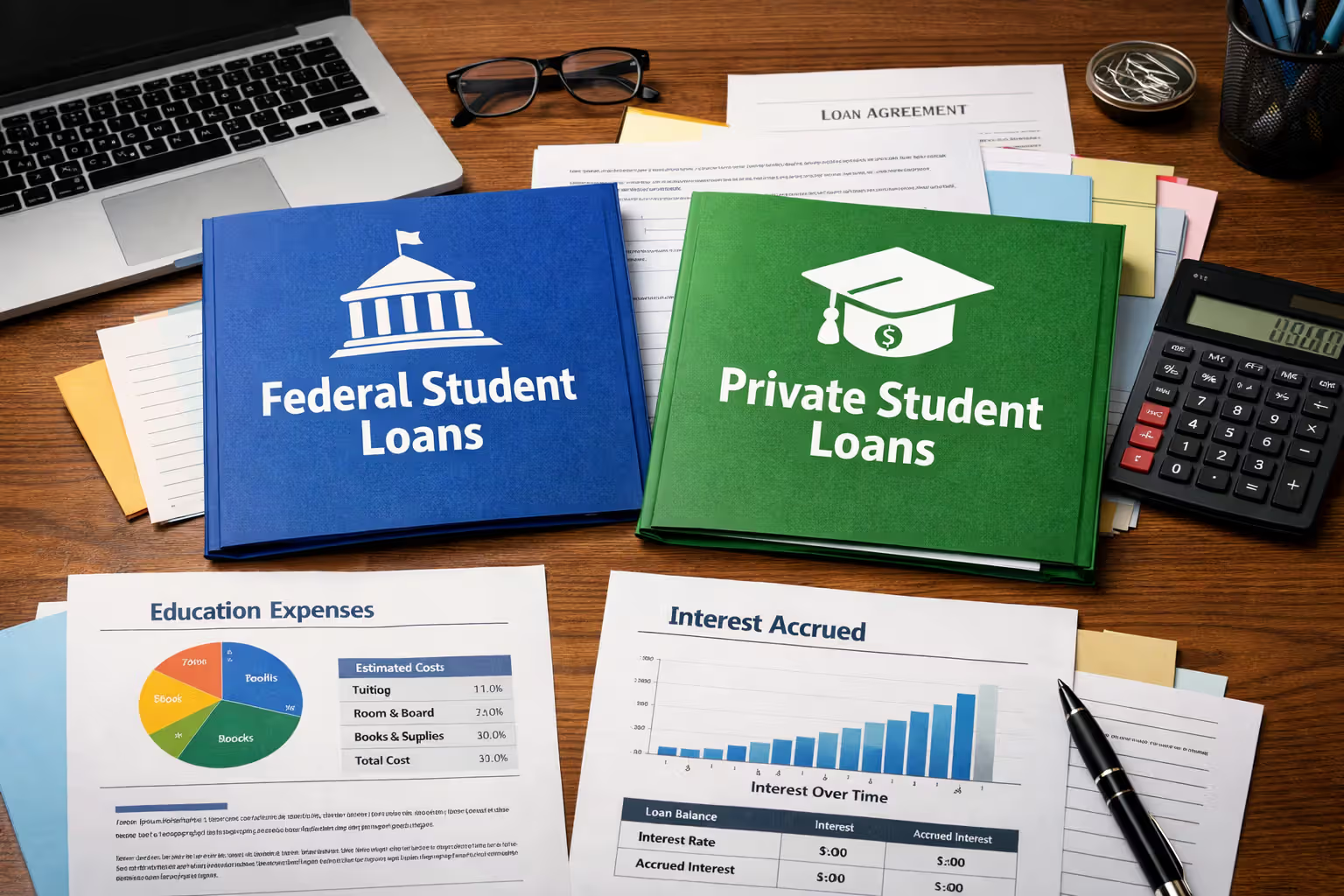

The Department of Education runs two federal programs for graduate students: Direct Unsubsidized Loans and Grad PLUS Loans. Banks and credit unions also offer private graduate loan products, but those skip federal protections like income-based payments and Public Service Loan Forgiveness eligibility. Smart money says max out federal options before touching private loans—though exceptions exist if you've got stellar credit and can lock in rates well below federal numbers.

Here's the typical cycle: you borrow each year, money goes straight to your school's bursar office to cover tuition and fees first, then housing and meal plans if applicable, and finally they refund whatever's left for your rent and living costs. Interest starts its climb immediately. You won't owe payments until six months after you drop below half-time enrollment, but that interest? Already growing.

Author: Marcus Bennett;

Source: sonicmusic.net

Types of Federal Graduate Student Loans

Two federal programs form the backbone of most graduate financing strategies. Both offer fixed rates, flexible payment plans, and borrower protections private lenders won't match. Understanding how Direct Unsubsidized and Grad PLUS loans work determines how much you'll actually pay over the lifetime of your debt.

Direct Unsubsidized Loans

Think of Direct Unsubsidized as your first-tier borrowing option. The program lets graduate students take up to $20,500 annually, with lifetime borrowing capped at $138,500 (that includes any undergrad federal loans still on your books).

No credit check happens with Direct Unsubsidized—a huge advantage if you're fresh from undergrad with limited credit history or recovering from past financial problems. You need to file a FAFSA and maintain half-time enrollment in an eligible program. Your school's financial aid office crunches the numbers on your cost of attendance, subtracts scholarships or grants you received, and determines your maximum borrowing eligibility.

The defining characteristic: interest charges begin at disbursement and never stop until you've paid everything back. Borrow $20,500 at the start of a two-year master's program and ignore it? You'll add roughly $2,800 in accumulated interest by graduation day (using current rates). That interest then capitalizes—gets added to your principal—making your balance $23,300 instead of $20,500 when you start repayment.

Smart borrowers make interest-only payments during school. Even $100 monthly prevents capitalization. You're covering the cost of borrowing in real-time rather than letting it snowball. Other students choose to defer everything until after graduation, accepting a larger starting balance in exchange for more cash flow while in school—especially if money's tight and you're working with a survival budget.

Grad PLUS Loans

Grad PLUS fills the canyon between Direct Unsubsidized limits and your actual costs. These loans have no annual caps beyond your school's certified expenses. Medical student facing $60,000 yearly costs? You can borrow up to that full amount by combining Direct Unsubsidized ($20,500) with Grad PLUS ($39,500).

Unlike Direct Unsubsidized, Grad PLUS requires passing a credit check. The Department of Education looks for what they call "adverse credit history"—debt in default, bankruptcy within five years, foreclosure, repossession, tax liens, wage garnishment, or federal student debt write-offs within the past five years. Delinquencies of 90+ days on debts exceeding $2,085 also trigger denial.

Get denied? Two paths forward: find an endorser (basically a co-signer) without adverse credit who'll vouch for you, or document extenuating circumstances explaining your credit problems. Many students who can't clear the Grad PLUS credit check pivot to private loans instead—though that usually means sacrificing federal benefits.

Grad PLUS costs more than Direct Unsubsidized on both fronts. Interest rates sit at 8.05% versus 7.05%, and origination fees run higher too. That rate premium reflects the credit risk and unlimited borrowing potential. Students pursuing expensive professional credentials find Grad PLUS loans necessary despite the elevated cost.

Both programs qualify for identical repayment plans and forgiveness programs, which keeps them superior to private loans for anyone considering public service careers or expecting variable income situations.

Students walk into my office thinking all education debt works the same way.Then they're shocked when I explain graduate loans charge interest immediately, or when they see how much $50,000 becomes after interest piles up during two years of school. The worst situations I see? Students who borrowed the maximum available without running the numbers on what they'd actually owe monthly

— Maria Chen

Graduate Student Loan Interest Rates and Fees

Congress sets these rates annually using a formula tied to 10-year Treasury notes. Rates stay fixed for each loan's entire life, so borrowing in different academic years means different rates locked in permanently.

Current 2025–2026 academic year rates:

| Loan Program | Fixed Interest Rate | Maximum Annual Amount | Lifetime Maximum | Credit Check? | Origination Fee |

| Direct Unsubsidized | 7.05% | $20,500 | $138,500 (includes any undergrad federal loans) | Not required | 1.057% |

| Grad PLUS | 8.05% | Your school's certified cost of attendance minus other aid | No cap | Required (adverse credit disqualifies) | 4.228% |

These numbers represent a significant jump from 2020–2022, when Direct Unsubsidized rates dropped below 5%. Today's rate environment means someone borrowing $80,000 across two years will shell out approximately $44,000 in interest charges over standard 10-year repayment.

Origination fees get deducted upfront from each disbursement. Your school certifies a $10,000 Grad PLUS loan? You'll actually receive $9,577 after the 4.228% fee vanishes, but you owe the full $10,000 plus accumulating interest. This surprises students who don't factor fees into their borrowing calculations.

Interest accumulates daily using simple interest: outstanding principal × interest rate ÷ 365. A $20,000 Direct Unsubsidized Loan at 7.05% grows by $3.86 every single day. Over a two-year program plus six-month grace period (912 days total), that loan adds $3,520 in interest before your first payment arrives. Skip those payments and that interest capitalizes—your new principal becomes $23,520, with future interest calculated on that inflated amount.

Author: Marcus Bennett;

Source: sonicmusic.net

Fixed rates provide certainty. Unlike variable-rate private loans, you'll never face rate increases regardless of Federal Reserve policy or economic conditions. You can budget confidently and plan long-term. The tradeoff? You won't benefit if market rates plummet either.

How to Apply for Graduate Student Loans

Accessing federal graduate loans involves several steps, ideally starting six to eight months before classes begin. The FAFSA forms the center of everything, along with your school's aid office and mandatory loan counseling.

Begin with the FAFSA at studentaid.gov. Applications open October 1st for the following academic year. Graduate students automatically qualify as independent filers, eliminating parental financial information requirements regardless of your age or living situation. You'll need your FSA ID (create one on StudentAid.gov), Social Security number, driver's license, and tax information from two years back (the 2026–2027 FAFSA requires 2024 tax data).

Completing the FAFSA establishes eligibility but doesn't guarantee borrowing. Your school's financial aid office receives your FAFSA results and assembles a financial aid package showing costs and available options. Many schools automatically include Direct Unsubsidized Loans in initial offers; Grad PLUS typically requires a separate application.

For Grad PLUS, visit studentaid.gov and submit the Grad PLUS Loan Request. Credit checks usually process instantly. Approved applicants complete Grad PLUS counseling (required for first-time Grad PLUS borrowers) and sign a Master Promissory Note. That note remains valid up to 10 years, so you'll typically sign once during your entire program unless you transfer institutions.

Your school's aid office then certifies your loan amount—confirming half-time enrollment and ensuring the loan doesn't exceed cost of attendance. Certification takes two to four weeks during peak periods (July through September), so submit applications early if you need money for first-semester bills.

Federal loans disburse straight to your school in multiple installments annually, usually at each semester or quarter's start. Schools apply funds to tuition first, then fees, campus housing, meal plans, and other institutional charges. Remaining amounts get refunded to you, typically within 14 days of disbursement.

First-time borrowers must complete entrance counseling at studentaid.gov before receiving funds. This mandatory step ensures you understand obligations, repayment choices, and default consequences. The counseling takes 20–30 minutes and covers your entire graduate program.

Documentation needed: government-issued ID, enrollment verification (your school handles this), and for Grad PLUS with adverse credit, potentially documentation supporting extenuating circumstances claims. Save copies of all Master Promissory Notes and disclosure statements—these documents lock in your exact interest rates and fee schedules.

Author: Marcus Bennett;

Source: sonicmusic.net

Private Student Loans for Graduate Students

Private lenders—banks, credit unions, online financial companies—offer graduate loans that can supplement or replace federal options. The catch? You'll trade federal protections for potentially lower rates, assuming your credit qualifies.

Consider private graduate loans when: you've maxed out Direct Unsubsidized and Grad PLUS but still face funding gaps; your credit score exceeds 720 and you can beat federal Grad PLUS rates; you're certain Public Service Loan Forgiveness isn't in your future; or you're confident about post-graduation income and want to minimize interest costs through lower rates.

Your credit profile drives everything in private lending. Lenders examine credit scores, income (including assistantships or part-time work), debt-to-income ratios, and employment records. Graduate students typically have thin credit files, complicating approval. Some lenders design products specifically for grad students that factor in expected post-graduation earnings, particularly for law, medicine, and MBA candidates at top-tier schools.

Variable versus fixed rates demands careful analysis. Variable-rate private loans often start 1–2 percentage points below fixed rates but fluctuate based on benchmark indices like SOFR (Secured Overnight Financing Rate). A 5.5% variable rate looks attractive versus 8.05% Grad PLUS, but if rates climb to 9% or 10% during repayment, you'll pay more overall. Fixed-rate private loans cost more upfront but provide predictability.

Private loans skip federal income-driven repayment entirely. Lose your job or face income drops? Federal loans let you cap payments at 10% of discretionary income. Private lenders might offer forbearance, but with fewer options and shorter timeframes. Private loans also can't qualify for Public Service Loan Forgiveness—a major consideration for anyone planning government, nonprofit, or qualifying public service careers.

Some students strategically deploy private loans for the final semester after exhausting federal limits, minimizing higher-risk private debt. Others with excellent credit and high-earning career trajectories refinance federal loans into private ones post-graduation, accepting loss of federal protections in exchange for interest savings.

Before choosing private lending, calculate actual cost differences. A 6% private loan versus 8.05% Grad PLUS on $30,000 saves roughly $3,600 in interest over 10 years—meaningful, but potentially not worth sacrificing income-driven repayment if your career path remains uncertain.

Repayment Options for Graduate Student Loans

Federal graduate loans offer multiple repayment structures designed for different financial realities and career trajectories. Your plan choice determines whether monthly payments feel manageable or crushing.

Standard Repayment spreads loans over 10 years with identical monthly payments. Costs the least in total interest but demands the highest monthly amount. Someone with $80,000 at 7.5% average interest pays approximately $948 monthly under standard repayment, eliminating debt in 10 years while paying about $33,760 in total interest.

Graduated Repayment begins with lower payments that increase every two years across a 10-year term. Works well for borrowers expecting significant income growth—think medical residents transitioning to attending salaries. You'll pay more total interest than standard repayment because early payments cover less principal.

Extended Repayment stretches payments across 25 years for borrowers exceeding $30,000 in Direct Loans. Monthly payments drop dramatically—that $80,000 balance falls to roughly $587 monthly—but total interest nearly doubles to approximately $96,000.

Income-Driven Repayment (IDR) plans cap monthly payments at a discretionary income percentage and forgive remaining balances after 20–25 years of qualifying payments. Four IDR plans exist: Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (now called SAVE), and Income-Contingent Repayment (ICR). The SAVE plan, fully operational since 2024, provides the most generous terms for most borrowers: 10% of discretionary income for graduate loans, with discretionary income calculated as earnings exceeding 225% of federal poverty guidelines.

Someone earning $65,000 annually (single filer, no dependents) pays around $300 monthly under SAVE—far below the $948 standard payment. The reality check: you'll pay for 25 years, and unpaid interest can accumulate (though SAVE includes interest subsidy provisions preventing runaway balance growth in many situations). After 25 years of payments, remaining balances get forgiven, though that forgiveness might create taxable income.

Public Service Loan Forgiveness (PSLF) erases remaining federal balances after 120 qualifying payments (10 years) while working full-time for qualifying employers—any government organization or 501(c)(3) nonprofit. Graduate students planning social work, public health, government, education, or nonprofit careers should pursue PSLF by enrolling in IDR immediately upon entering repayment. PSLF forgiveness comes tax-free, making it substantially more valuable than standard IDR forgiveness.

Deferment and forbearance temporarily suspend payments during financial hardship, unemployment, or additional schooling. Interest keeps accumulating on all graduate loans during these periods (unlike subsidized undergrad loans). Use sparingly—every forbearance month increases ultimate repayment costs.

Most graduate students benefit from starting with IDR enrollment, even expecting high incomes. You can always increase payments voluntarily or switch to standard repayment later, but beginning with lower required payments provides flexibility during career transitions.

Author: Marcus Bennett;

Source: sonicmusic.net

Common Mistakes When Borrowing for Graduate School

Graduate students make predictable errors that multiply costs exponentially. Sidestepping these traps can save tens of thousands of dollars and shave years off repayment timelines.

Over-borrowing tops the list. Federal loans permit borrowing up to full cost of attendance, including generous living expense allowances. Someone attending school in a low-cost area might borrow $25,000 annually for living expenses when $18,000 covers actual needs. That extra $7,000 yearly over a two-year program, with accumulated interest, costs roughly $11,000 across a 10-year repayment term. Borrow only genuine needs, accounting for part-time income, savings, or partner contributions.

Ignoring interest accumulation during school creates graduation day sticker shock. Your $60,000 borrowed becomes $68,000 after two years of accrued interest without payments. Many students miss that interest capitalizes—gets added to principal—upon entering repayment, inflating every future payment. Making interest-only payments during school, even $50–100 monthly, prevents capitalization and saves thousands long-term. Others defer all payments until graduation, accepting larger principal balances for better cash flow during enrollment.

Skipping federal options before exploring private lending eliminates access to income-driven repayment and loan forgiveness. Some students see private loan marketing promising rates below federal options and jump to private lending without maximizing Direct Unsubsidized and Grad PLUS first. Federal loans should anchor your borrowing strategy; add private loans only if federal proves insufficient.

Neglecting to compare programs' return on investment creates unsustainable debt loads. A $120,000 master's in a field with $55,000 median starting salaries creates nearly impossible repayment scenarios under standard plans. Research typical earnings for your target career, calculate debt-to-income ratios (target total student debt below 1.5× expected first-year salary), and consider lower-cost programs or part-time enrollment while working.

Rushing through loan counseling and disclosure review means missing critical obligation details. Many students click through entrance counseling without absorbing content, then feel blindsided by repayment requirements. Read loan disclosures carefully—they specify exact interest rates, fees, and first payment timing.

Borrowing for non-essentials—new laptops when current ones function, expensive apartments, frequent travel—treats student loans like free money. Every borrowed dollar costs $1.40–1.80 over 10-year repayment once interest compounds. Question whether each expense truly supports degree completion.

Losing contact with loan servicers after graduation triggers missed payment deadlines and potential default. Update contact details, establish autopay (reducing interest rates by 0.25%), and respond promptly to servicer communications. Default destroys credit, triggers wage garnishment, and eliminates future federal aid eligibility.

Frequently Asked Questions About Graduate Student Loans

Graduate student loans represent a substantial multi-decade financial commitment demanding careful planning and informed choices. The combination of elevated borrowing limits, immediate interest accumulation, and zero subsidized options means graduate debt piles up faster and costs more than undergraduate borrowing.

Begin with federal Direct Unsubsidized Loans, offering the lowest rates without credit checks. Layer in Grad PLUS Loans only after exhausting Direct Unsubsidized options, and explore private loans exclusively if you've got strong credit and can lock in meaningfully lower rates—while accepting you'll forfeit federal repayment flexibility.

Calculate expected debt-to-income ratios before committing to any program. Financial advisors generally recommend maintaining total student debt below 1.5× expected first-year salary. A career starting at $70,000 can reasonably support $105,000 in student debt; borrowing $150,000 for identical career prospects creates financial pressure under any repayment structure.

Make interest payments during enrollment whenever financially feasible. Even modest monthly contributions prevent capitalization and preserve thousands over loan lifetimes. Can't afford interest payments? At minimum, understand how much interest will accumulate and capitalize to avoid graduation day shock at your balance.

Select repayment plans strategically. Income-driven repayment provides flexibility and enables loan forgiveness access, particularly Public Service Loan Forgiveness for qualifying careers. Standard repayment minimizes total interest but demands higher monthly payments that may not align with early-career budgets.

Graduate education can revolutionize your career and earning trajectory, but only when you manage financing intelligently. Borrow intentionally, comprehend your terms completely, and maintain active communication with loan servicers throughout repayment. Your graduate degree should amplify your financial future—not saddle it with decades of overwhelming debt.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.