Student Loans Resource & Financial Education

Source: sonicmusic.net

Welcome to our Student Loans resource center — a place dedicated to helping students, graduates, and families better understand the world of education financing. Here we discuss federal and private student loans, repayment strategies, interest rates, forgiveness programs, and practical ways to manage education debt with greater confidence.

You’ll find clear explanations of how student loans work, step-by-step guidance on applying for loans, comparisons of repayment plans, and helpful tools such as loan calculators and financial planning tips. We also explore topics like loan forgiveness programs, deferment and forbearance options, refinancing, and ways to reduce long-term borrowing costs.

Read more

Top Stories

Read more

Read more

Read more

Read more

Trending

Read more

Read more

Latest articles

Most read

Read more

Read more

In depth

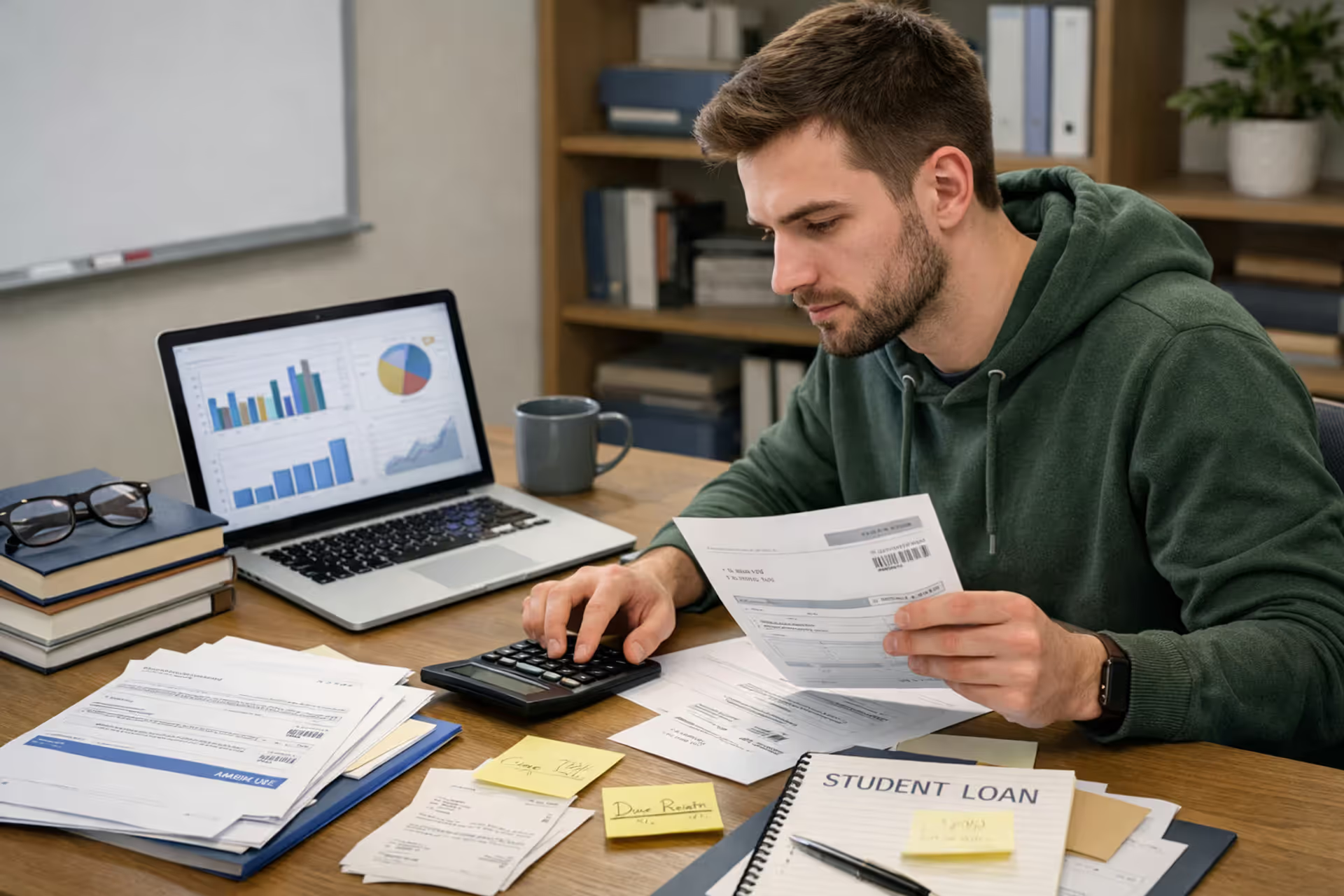

Grad school costs serious money. Whether you're pursuing an MBA, law degree, PhD, or medical training, you're looking at price tags that can exceed $100,000 for many programs. Recent data from the Education Data Initiative shows the typical grad student leaves school with over $76,000 in borrowed funds—and that figure climbs much higher for professional programs like medicine or dentistry.

Here's what catches people off guard: borrowing for graduate programs works completely differently than undergrad loans. You'll face higher limits, steeper rates, and rules that flip everything you learned about student loans the first time around. Those differences matter because they'll follow you for 10, 20, or even 25 years after you finish your degree.

Most people cobble together money from several sources. You might get a teaching assistantship covering half your tuition, borrow federal loans for the rest, and maybe tap into private lending if there's still a gap. How you structure this mix—and which loan programs you choose—creates either a manageable situation or a financial mess that follows you into your 40s.

This guide walks you through the real mechanics of financing grad school: which federal programs exist, what they actually cost right now, how to navigate the application maze, when private loans make sense, how repayment works in practice, and which mistakes cost borrowers the most money.

What Are Graduate Student Loans?

These are specialized financing tools built for anyone enro...

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer guidance on student loan topics, including federal and private student loans, interest rates, repayment plans, loan forgiveness programs, deferment, forbearance, consolidation, and related financial matters. The information presented should not be considered legal, financial, tax, or professional lending advice.

All information, articles, explanations, and program discussions published on this website are provided for general informational purposes. Student loan programs, repayment options, forgiveness eligibility, and financial assistance policies may change over time and may vary depending on government regulations, loan servicers, lenders, borrower eligibility, income level, school status, and individual loan terms. Details such as interest rates, repayment schedules, eligibility for forgiveness programs, and application requirements may differ between federal and private lenders and may change without notice.

While we strive to keep the information accurate and up to date, this website makes no guarantees regarding the completeness, reliability, or accuracy of the content. The website and its authors are not responsible for any errors, omissions, or actions taken based on the information provided here.

Use of this website does not create a financial advisor–client, legal, or professional relationship. Visitors are encouraged to review the official documentation provided by the U.S. Department of Education, student loan servicers, and private lenders, and to consult with a qualified financial advisor, loan specialist, or legal professional before making decisions regarding student loans, repayment strategies, or financial obligations.